Epoxy Adhesive Market

Epoxy Adhesive Market Size, Market Share & Trends Analysis Report By Type (One-component, Two-component), By Application (Automotive, Construction, Aerospace, Electronics, Marine, Others), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

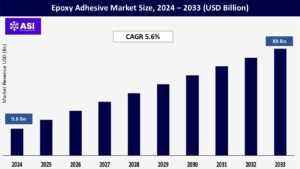

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASICMR1004

CAGR: 5.6%

Last Updated : February 3, 2026

The global epoxy adhesive market size was approximately USD 9.8 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a steady CAGR of 5.6% over the forecast period (2026–2033).

Epoxy adhesives are widely utilized in industries such as automotive, construction, aerospace, electronics, and marine due to their superior bonding strength, chemical resistance, and durability. The increasing demand for lightweight and high-performance materials across various applications is fueling market growth. Key growth drivers include advancements in adhesive formulations, rising demand for sustainable bonding solutions, and expanding applications in critical end-use industries, supporting the continued expansion of the epoxy adhesive market size.

The epoxy adhesive market is experiencing significant growth driven by increasing adoption in automotive and aerospace manufacturing. Epoxy adhesives are preferred in these sectors due to their ability to provide strong structural bonds, resist high temperatures, and reduce vehicle weight by replacing traditional mechanical fasteners.

According to the European Automobile Manufacturers Association (ACEA), global vehicle production is projected to rise by 4.5% annually, further driving epoxy adhesive consumption. Additionally, the International Air Transport Association (IATA) estimates that global passenger air traffic will grow at an annual rate of 3.6% over the next two decades, leading to increased aircraft manufacturing and maintenance activities, which require advanced adhesive solutions. The shift toward electric vehicles (EVs) and the need for lightweight materials in aircraft manufacturing are further propelling demand. These trends strongly supporting epoxy adhesive market growth.

Innovations in epoxy adhesive formulations are enhancing product performance, including improved flexibility, thermal resistance, and faster curing times. Manufacturers are developing advanced adhesives that meet stringent regulatory requirements, particularly in industries such as electronics and healthcare. Additionally, the development of bio-based and environmentally friendly epoxy adhesives is gaining traction.

For example, the U.S. Department of Energy (DOE) has invested over $100 million in research programs focused on advanced materials and adhesives for energy-efficient applications. Similarly, the European Union’s Horizon Europe program, with a budget exceeding €95 billion, supports innovation in sustainable and high-performance materials, including epoxy adhesives. Such innovations are expected to accelerate epoxy adhesive market growth over the forecast period.

The cost of epoxy adhesives is influenced by fluctuations in raw material prices, including epichlorohydrin and bisphenol-A. Price volatility and supply chain disruptions can impact market stability, making it challenging for manufacturers to maintain competitive pricing.

Stringent environmental regulations regarding volatile organic compound (VOC) emissions and hazardous chemicals pose challenges for the epoxy adhesive market. Manufacturers are focusing on developing low-VOC and solvent-free adhesives to comply with evolving regulatory standards. These requirements are reshaping product development strategies within the epoxy adhesive industry.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

|

| By Application |

|

| Key Players |

Henkel AG & Co. KGaA 3M Company H.B. Fuller Company Sika AG Huntsman Corporation Dow Inc. Arkema Group Ashland Global Holdings Inc. Lord Corporation Permabond Engineering Adhesives |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Two-component epoxy adhesives dominated the epoxy adhesive market share in 2024, holding a share of over 56%. These adhesives provide superior bonding strength, durability, and resistance to environmental factors, making them ideal for structural applications in construction, automotive, and aerospace industries. One-component epoxy adhesives are gaining popularity due to their ease of use and faster curing times, particularly in electronics and consumer goods applications.

The automotive sector accounted for the largest market share in 2024, driven by the growing use of epoxy adhesives in vehicle assembly and structural bonding. The construction industry is also a significant contributor, leveraging epoxy adhesives for infrastructure projects, flooring, and composite bonding. The electronics segment is projected to witness the fastest growth, driven by increasing demand for high-performance adhesives in semiconductor packaging and circuit board assembly.

North America accounted for 29.3% of the global epoxy adhesive market share in 2024, driven by strong demand from the aerospace, automotive, and electronics industries. The U.S. leads in epoxy adhesive innovation, with companies investing in research and development to enhance product performance and sustainability.

Europe held xx% of the market share in 2024, supported by stringent environmental regulations and the region’s focus on sustainable adhesive solutions. Germany, France, and the UK are key contributors, particularly in the automotive and construction sectors.

Asia-Pacific is projected to register the highest CAGR of 6.8% during the forecast period, driven by rapid industrialization, infrastructure development, and growth in manufacturing sectors. China, Japan, and India are major markets, with China leading due to its expanding automotive and electronics industries. These factors are expected to significantly increase the epoxy adhesive market size across the Asia-Pacific region.

The Middle East and Africa are emerging markets, with increasing infrastructure projects and construction activities driving epoxy adhesive demand. Countries such as Saudi Arabia and the UAE are investing in smart cities and large-scale industrial projects, supporting market expansion. Such developments are contributing to the gradual rise in the epoxy adhesive market size in emerging economies.

Latin America is witnessing steady growth, with Brazil and Mexico leading the market due to their expanding automotive and aerospace industries.

The global epoxy adhesive market was valued at approximately USD 9.8 billion in 2024 and is projected to grow at a compound annual growth rate (CAGR) of 5.6% during the forecast period (2026–2033), reaching USD XX billion by 2033.

Two-component epoxy adhesives dominated the market in 2024, holding a share of over 56%. They are preferred for their superior bonding strength, durability, and resistance to environmental factors, making them ideal for structural applications.

North America held the largest market share in 2024, accounting for 29.3% of the global market. The region’s growth is driven by strong demand from the aerospace, automotive, and electronics industries, along with significant investments in research and development.

The key verticals in the market are Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Huntsman Corporation, Dow Inc., Arkema Group, Ashland Global Holdings Inc., Lord Corporation, and Permabond Engineering Adhesives.