Green Power Market

Green Power Market Size, Market Share & Trends Analysis Report, By Source (Solar Energy, Wind Energy, Hydropower, Geothermal, Biomass), By Application (Residential, Commercial, Industrial, Utility), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2032

Report Code : ASIEPR1005

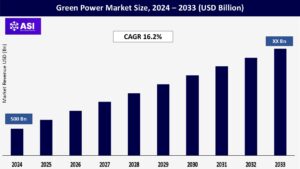

CAGR: 16.2%

Last Updated : July 13, 2026

The global Green Power Market size was valued at approximately USD 500 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a robust CAGR of 16.2% during the forecast period (2026–2033).

Green power sources such as solar, wind, hydropower, geothermal, and biomass are becoming pivotal in the global transition to renewable energy. Driven by mounting climate concerns, favorable government policies, and technological advancements, green power adoption is scaling new heights.

Key growth drivers include rapid industrialization, increasing awareness about sustainable energy solutions, and ongoing innovations that enhance energy generation and efficiency.

Rising investment in renewable energy projects is a significant driver of market growth. According to BloombergNEF, global investment in clean energy reached $1.1 trillion in 2023, marking a 31% increase from 2022.

Governments, private organizations, and financial institutions are channeling funds into solar farms, wind parks, and other green power projects. Additionally, green bonds, valued at $620 billion in 2023, are providing critical financing for sustainable energy initiatives.

The European Union’s Green Deal, which aims to make Europe climate-neutral by 2050, has allocated over €1 trillion for renewable energy projects. Similarly, the U.S. Inflation Reduction Act provides $369 billion for clean energy initiatives, targeting a 40% reduction in emissions by 2030.

In the Asia-Pacific, China leads the global renewable energy capacity, with a goal of 1,200 GW of solar and wind power by 2030, while India’s National Solar Mission targets 280 GW of solar capacity by 2030.

According to the International Renewable Energy Agency (IRENA), the global weighted-average Levelized Cost of Energy (LCOE) for solar and wind projects declined by 85% and 56%, respectively, from 2010 to 2023. This cost reduction is driving higher adoption across residential, commercial, and industrial sectors.

Additionally, innovations in solar photovoltaic (PV) technology, offshore wind farms, and energy storage systems are making green power more efficient and cost-competitive. For instance, bifacial solar panels, capable of capturing sunlight on both sides, have increased energy yields by up to 20%.

Offshore wind turbines, such as General Electric’s Haliade-X with a capacity of 14 MW, are significantly boosting wind energy potential. Additionally, advancements in energy storage, such as lithium-ion and flow batteries, are addressing intermittency issues, enabling a stable green power supply.

The green power market faces hurdles in grid infrastructure development and modernization. The intermittent nature of solar and wind energy necessitates robust grid systems with storage capabilities to ensure reliability.

Countries with outdated or insufficient grid networks, such as those in Africa and parts of Southeast Asia, struggle to fully utilize renewable energy potential. Additionally, high capital investments in grid modernization and energy storage solutions deter smaller players from entering the market.

The large-scale deployment of green energy infrastructure requires significant land resources, often leading to conflicts with agricultural, residential, or conservation interests. For instance, expanding wind farms in densely populated regions of Europe or the U.S. has faced resistance from local communities.

Furthermore, over-reliance on specific resources, such as rare earth elements for solar panels and wind turbines, exposes the market to supply chain vulnerabilities.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Source |

Solar Energy Wind Energy Hydropower Geothermal Biomass

|

| By Applications |

Residential Commercial Industrial Utility |

| Key Players |

Tesla, Inc. Siemens Gamesa Renewable Energy Vestas Wind Systems A/S Canadian Solar Inc. Orsted A/S NextEra Energy, Inc. Enel Green Power S.p.A Iberdrola S.A. Brookfield Renewable Partners L.P. First Solar, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

By source, solar energy dominated the market in 2024 with a share of over 39.7%, driven by the widespread adoption of rooftop solar systems and utility-scale projects. Wind energy, particularly offshore wind, is projected to grow at the fastest rate, supported by advancements in turbine technology and favorable coastal installations.

Hydropower remains a cornerstone of green power, especially in regions with abundant water resources, contributing 30.5% to the global market share. Biomass and geothermal energy offer niche applications but are increasingly gaining traction for industrial and localized use.

By application, the utility sector led the market with a 42.4% share in 2024, driven by large-scale renewable energy installations for grid supply. Industrial applications are gaining momentum as manufacturers aim to achieve sustainability targets. Residential and commercial sectors are witnessing steady growth, fueled by decentralized energy solutions such as rooftop solar and community wind projects.

North America accounted for 28.7% of the global market share in 2024, driven by federal incentives such as tax credits for solar and wind projects. The U.S. leads in wind power installations, while Canada is a pioneer in hydropower development. In the U.S., renewable energy has seen significant developments recently.

The U.S. Energy Information Administration (EIA) projects that new solar installations will drive the majority of the country’s electricity generation growth over the next two years.

In 2025, utilities and independent power producers are expected to add 26 gigawatts (GW) of solar capacity, followed by an additional 22 GW in 2026. This follows a record addition of 37 GW of solar power capacity in 2024, nearly doubling the additions from 2023.

Policy shifts have also impacted the renewable energy landscape. President Donald Trump has halted $300 billion in clean energy loans, affecting projects in manufacturing and renewable energy sectors across the country. These loans, part of the Inflation Reduction Act and the Bipartisan Infrastructure Law, were intended to support initiatives in wind, solar, and electric vehicles.

Despite a broader pivot back to pro-oil and gas policies, the Trump administration has shown favorable attention toward geothermal energy.

Geothermal power provides steady electricity generation and utilizes technology similar to that of the oil and gas industries. Bipartisan support in Congress underscores the potential of this climate-friendly energy source, with projections of up to 90 GW of capacity by 2050.

Europe accounted for 32.3% of the global green power market share in 2024, establishing itself as a leader in renewable energy adoption. This leadership is driven by ambitious renewable energy policies, substantial investments, and collaborative efforts among member states under the European Union’s Green Deal.

Germany, the UK, and Denmark stand out as frontrunners in Europe’s renewable energy landscape. Germany, with its Energiewende (Energy Transition) policy, has focused on phasing out coal and nuclear power in favor of solar, wind, and biomass.

As of 2024, Germany had installed over 67 GW of solar power capacity and 62 GW of wind capacity, including both onshore and offshore installations. Furthermore, Germany’s green hydrogen projects aim to produce 5 GW of electrolysis capacity by 2030, solidifying its position as a leader in hydrogen energy.

The UK is aggressively advancing its renewable energy portfolio, particularly in offshore wind. The country’s Crown Estate Round 4 auction allocated seabed leases for an additional 8 GW of offshore wind capacity in 2024, aligning with the government’s commitment to achieving 50 GW of offshore wind power by 2030.

Furthermore, projects like Dogger Bank Wind Farm, which will become the world’s largest offshore wind farm, exemplify the UK’s commitment to leveraging its vast maritime resources for sustainable power generation.

Denmark, known for its long-standing leadership in wind energy, continues to innovate with projects such as artificial energy islands.

The Danish government has embarked on a plan to construct energy islands in the North Sea and Baltic Sea, which are expected to support 5 GW of wind energy capacity, catering to the energy needs of millions while bolstering Europe’s green energy grid integration.

The European Union’s Green Deal is a cornerstone of the region’s renewable energy advancement, with a budget of €1 trillion over the next decade focused on achieving net zero emissions by 2050.

Central to this vision are massive offshore wind projects in the North Sea, where collaboration among countries like Germany, the Netherlands, Belgium, and Denmark aims to deploy 300 GW of offshore wind capacity by 2050.

In Southern Europe, countries like Spain, Italy, and Greece are capitalizing on their abundant solar resources. Spain installed nearly 4 GW of new solar capacity in 2024, supported by government initiatives such as subsidies and green energy auctions.

The Asia-Pacific region is projected to record the highest compound annual growth rate (CAGR) of 15.1% during the forecast period of 2026 to 2033, making it a pivotal player in the global green power market.

This rapid growth can be attributed to accelerating industrialization, increasing energy demand, and strong governmental support for renewable energy initiatives in key countries like China, India, Japan, and South Korea.

China, the world’s largest emitter of carbon dioxide, is aggressively pursuing clean energy goals as part of its commitment to achieving carbon neutrality by 2060.

In 2024 alone, China added approximately 120 GW of new solar and wind power capacity, accounting for over 55% of global capacity additions. The country is also making strides in offshore wind power, with significant projects in Guangdong and Jiangsu provinces. In parallel, China’s 14th Five-Year Plan emphasizes green hydrogen, aiming for 50% cost reduction in hydrogen production by 2030.

India is another significant contributor to Asia-Pacific’s green power momentum, driven by the government’s ambitious renewable energy targets. The country is on track to achieve 500 GW of renewable energy capacity by 2030, with solar power playing a central role.

Flagship programs like the National Solar Mission and the Green Energy Corridor are enhancing the infrastructure needed for renewable energy integration into the grid.

Additionally, India aims to become a global hub for green hydrogen production, leveraging its vast renewable energy resources to manufacture cost-competitive hydrogen for both domestic use and export.

Japan and South Korea are increasingly focusing on green hydrogen projects as a sustainable energy solution. Japan, under its Basic Hydrogen Strategy, aims to create a fully hydrogen-powered society by 2050, with investment exceeding USD 19 billion into research and infrastructure by 2030.

South Korea, on the other hand, plans to achieve net zero emissions by 2050 through its Green New Deal initiative, which includes a target of producing 6.2 million hydrogen fuel cell vehicles and constructing 1,200 hydrogen refueling stations by 2040.

In Southeast Asia, nations such as Indonesia, Vietnam, and the Philippines are emerging as new hubs for renewable energy deployment, driven by rising energy demands and increasing foreign direct investment in renewable projects. Vietnam alone installed 9 GW of solar capacity in 2024, driven by incentives such as feed-in tariffs and foreign partnerships.

Middle East and Africa are emerging markets, focusing on solar power to address energy access issues. Projects like Saudi Arabia’s NEOM and South Africa’s Renewable Energy Independent Power Producer Procurement (REIPPP) program are examples of large-scale investments.

Latin America is making significant strides in wind and solar energy, with Brazil and Chile leading the way. Regional policies such as Brazil’s PROINFA program and Chile’s commitment to carbon neutrality by 2050 support market expansion.

The green power market was valued at approximately USD 500 billion in 2024. It is projected to reach USD XX billion by 2033, growing at a robust CAGR of 16.2% during the forecast period (2026–2033).