Airport Security Market

Airport Security Market Size, Market Share & Trends Analysis Report By Type (Access Control, Cybersecurity, Perimeter Security, Screening, Surveillance), By Application (Commercial Airports, Cargo Airports, Military Airports), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1003

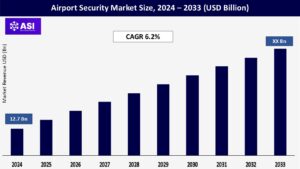

CAGR: 6.2%

Last Updated : May 12, 2026

The global Airport Security Market size was valued at approximately USD 12.7 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a steady CAGR of 6.2% during the forecast period (2026–2033).

Airport security systems are critical for ensuring the safety and security of passengers, staff, and infrastructure. The increasing threat of terrorism, rising air passenger traffic, and stringent government regulations are driving the demand for advanced security solutions. Key technologies include access control, cybersecurity, perimeter security, screening, and surveillance systems.

The global increase in air passenger traffic, coupled with the growing threat of terrorism and cyberattacks, is a major driver for the airport security market. According to the International Air Transport Association (IATA), global air passenger traffic is expected to grow at an annual rate of 3.5% over the next decade.

This growth necessitates enhanced security measures to ensure passenger safety and prevent unauthorized access to restricted areas. As more people choose air travel for both domestic and international trips, airports are experiencing higher passenger throughput, creating challenges in maintaining efficient yet thorough security checks.

This has led to the adoption of advanced technologies such as biometric identification, advanced imaging systems, and explosive detection tools to streamline processes while ensuring safety.

The evolving threat of terrorism remains a critical concern, with terrorist organizations continually targeting airports and aircraft. To counter these risks, airports are implementing stricter screening procedures and investing in cutting-edge security infrastructure.

Additionally, the rise in cyber threats has become a significant issue as airports and airlines increasingly rely on digital systems for operations such as passenger check-ins, baggage handling, and air traffic control. Cybersecurity measures are now an essential component of airport security strategies to protect against disruptions, data breaches, and potential threats to passenger safety.

Governments and international organizations like the International Civil Aviation Organization (ICAO) have also established stringent security standards, requiring airports to comply with regulations that often demand significant investments in technology and personnel training.

Innovations in biometrics, artificial intelligence (AI), and machine learning (ML) are transforming airport security. Advanced screening systems, such as full-body scanners and automated threat detection systems, are improving the efficiency and accuracy of security checks.

Additionally, the integration of cybersecurity solutions is becoming increasingly important to protect sensitive data and critical infrastructure from cyber threats.

The deployment of advanced security systems, such as biometric scanners and AI-based surveillance, requires significant capital investment, posing a major challenge for airports, especially smaller ones and those in developing regions. While these technologies are essential for enhancing security and streamlining passenger processing, their high upfront costs for installation and integration into existing infrastructure can be prohibitive.

Additionally, ongoing maintenance and periodic upgrades further strain budgets, as they demand specialized expertise and resources to ensure optimal functionality. For smaller airports with limited financial capacity, these expenses can create disparities in security capabilities, leaving some regions less equipped to handle modern threats.

Compounding these financial challenges are stringent regulatory and privacy concerns surrounding the use of advanced technologies, particularly biometric systems. Governments and international bodies have implemented strict data protection laws, such as the General Data Protection Regulation (GDPR) in Europe, requiring airports to comply with complex legal frameworks.

Compliance often necessitates additional investments in robust data protection measures, including encryption, secure storage solutions, and regular audits, which further increase operational costs.

Moreover, the potential for public backlash over privacy violations or data breaches adds another layer of complexity, forcing airports to balance enhanced security with the responsibility of safeguarding passenger information.

These challenges underscore the need for airports to strike a delicate balance between adopting advanced security technologies, managing costs, and ensuring regulatory compliance. While these systems are critical for addressing evolving threats and improving efficiency, their high implementation and maintenance costs, coupled with regulatory hurdles, can hinder market growth and limit accessibility for smaller or less financially equipped airports.

Addressing these issues will require innovative financing models, government support, and collaboration among stakeholders to ensure that all airports can meet modern security demands without compromising privacy or operational sustainability.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Access Control Cybersecurity Perimeter Security Screening Surveillance |

| By Application |

Commercial Airports Cargo Airports Military Airports |

| Key Players |

Honeywell International Inc. Siemens AG Thales Group Raytheon Technologies Corporation Smiths Group plc L3Harris Technologies, Inc. NEC Corporation Bosch Security Systems Unisys Corporation Rapiscan Systems |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The airport security market is segmented by type, with each category playing a vital role in ensuring comprehensive safety and operational efficiency. In 2024, access control systems dominated the market, accounting for over 31% of the global share.

These systems, which include biometric scanners, smart card readers, and facial recognition technologies, are essential for managing the movement of passengers and staff within secure areas, ensuring that only authorized individuals gain access. Their widespread adoption is driven by the need for enhanced security and streamlined operations in increasingly busy airport environments.

Cybersecurity is another critical segment, expected to witness the fastest growth during the forecast period. This growth is fueled by the aviation industry’s growing reliance on digital systems for operations such as passenger check-ins, baggage handling, and air traffic control.

As cyber threats become more sophisticated, the demand for robust cybersecurity measures, including encryption, intrusion detection systems, and secure data storage solutions, is rising rapidly. Protecting sensitive passenger data and ensuring the integrity of airport operations are top priorities, making cybersecurity a key area of investment.

The airport security market is also segmented by application, with commercial airports holding the largest market share in 2024. This dominance is driven by the high volume of passenger traffic at commercial airports, which necessitates robust and efficient security measures to ensure safety and compliance with international regulations.

The increasing number of travelers, coupled with the growing threat of terrorism and cyberattacks, has led to significant investments in advanced security technologies such as biometric access control, AI-based surveillance, and sophisticated screening systems. These measures are essential not only for protecting passengers but also for maintaining operational efficiency and minimizing delays.

On the other hand, military airports are expected to experience steady growth during the forecast period. This growth is fueled by increasing investments in defense infrastructure and the need for advanced security solutions to protect sensitive military assets, personnel, and operations.

Military airports require specialized security systems tailored to their unique needs, including perimeter security, access control for restricted areas, and cybersecurity measures to safeguard critical data and communication networks. As global defense spending rises and geopolitical tensions persist, the demand for cutting-edge security solutions in military airports is likely to grow, further driving this segment’s expansion.

North America dominated the airport security market, accounting for 35.2% of the global share. This leadership is driven by stringent security regulations, the presence of major airport security solution providers, and substantial investments in advanced screening and surveillance technologies.

The U.S., in particular, is a key market, with its focus on countering terrorism and cyber threats fueling the adoption of cutting-edge security systems.

Europe held a significant market share in 2024, supported by the region’s emphasis on enhancing airport security and complying with EU regulations. Countries such as the UK, Germany, and France are leading contributors, with their airports adopting advanced technologies like biometric access control and AI-based surveillance to ensure passenger safety and operational efficiency.

The region’s strong regulatory framework and focus on data privacy further drive the demand for compliant security solutions.

The Asia-Pacific region is projected to register the highest compound annual growth rate (CAGR) of 7.5% during the forecast period. This growth is fueled by rapid urbanization, increasing air passenger traffic, and government initiatives to modernize airport infrastructure.

Major markets such as China, India, and Japan are investing heavily in advanced security systems to accommodate their growing aviation sectors and address emerging security threats.

The global Airport Security market was valued at approximately USD 12.7 billion in 2024.

North America dominated the market, accounting for 35.2% of the global share in 2024, driven by stringent security regulations and significant investments in advanced technologies.

The access control segment holds the largest market share, accounting for over 31% in 2024. This includes technologies like biometric scanners, smart card readers, and facial recognition systems.

Key drivers include rising air passenger traffic, increasing threats of terrorism and cyberattacks, stringent government regulations, and advancements in security technologies such as AI and biometrics.

The Asia-Pacific region is projected to grow at the highest CAGR of 7.5% during the forecast period, driven by rapid urbanization, increasing air travel, and government initiatives to modernize airport infrastructure.

The major types include:

The main applications are:

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Airport Security Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Airport Security Market, By Application

6.1 North America Airport Security Market, By Country

6.1.1 Airport Security Market, By Type

6.1.2 Airport Security Market, By Application

6.2 U.S.

6.2.1 Airport Security Market, By Type

6.2.2 Airport Security Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping