Airship Market

Airship Market Size, Market Share & Trends Analysis Report By Type (Rigid, Semi-Rigid, Non-Rigid), By Application (Commercial, Military, Research, Cargo Transport), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1004

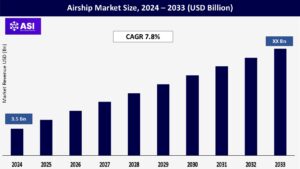

CAGR: 7.8%

Last Updated : May 13, 2026

The global Airship Market size was valued at approximately USD 3.5 billion in 2024 and is projected to reach USD XX billion by 2033, growing at a CAGR of 7.8% during the forecast period (2026–2033).

Airships are gaining traction in commercial and military applications due to their low operational costs, long endurance capabilities, and ability to operate in remote areas. Advancements in aerostat technology, increasing demand for aerial surveillance, and the resurgence of airships in logistics and cargo transportation are driving market growth.

Airships have proven to be a valuable asset in surveillance, intelligence gathering, and border security due to their ability to operate at high altitudes for extended periods. This makes them ideal for monitoring large areas with minimal ground-based infrastructure.

For example, the U.S. Department of Defense has deployed aerostats for persistent surveillance, particularly in areas such as the U.S.-Mexico border and in conflict zones like Afghanistan, where airships provide real-time intelligence and situational awareness.

Additionally, the U.S. Army has been testing tethered aerostat systems, capable of carrying advanced radar, communications equipment, and video cameras, for enhanced border and coastal surveillance.

The global market for surveillance and reconnaissance airships is expected to grow substantially, with defense budgets of various countries allocating increased funding for these systems to strengthen national security and monitor strategic areas.

The rising concern about carbon emissions has led the aviation and logistics sectors to look for greener alternatives for cargo transport, and airships are emerging as a promising solution. Hybrid airships, combining the lift of helium with propulsion systems, offer a potential reduction in carbon footprints compared to traditional aircraft and trucks.

Companies like Hybrid Air Vehicles and LTA Research are developing airships capable of carrying payloads of several tons over long distances while consuming far less fuel than conventional airplanes. A notable example is the development of the Airlander 10, the world’s largest hybrid airship, which is designed for long-haul cargo transport and is currently undergoing testing.

Furthermore, airships can access remote regions, including the Arctic and offshore areas, where traditional logistics infrastructure may be lacking. Humanitarian organizations are exploring airships for delivering aid to hard-to-reach areas, while businesses are beginning to use airships for Arctic logistics and offshore resupply missions.

With environmental concerns driving the move toward sustainable transport, the airship market is expected to see increasing interest from sectors such as logistics, humanitarian aid, and government supply chains.

Airships are susceptible to adverse weather conditions, limiting their operational efficiency. Strong winds and turbulence can pose challenges, making them less reliable than fixed-wing aircraft for certain applications. Additionally, their payload capacity remains lower than conventional cargo aircraft, restricting their use in high-volume logistics.

Despite lower operational costs, the initial investment required for airship development remains a key barrier. Research, materials, and regulatory certifications contribute to high capital costs, limiting the entry of new players in the market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Rigid Semi-Rigid Non-Rigid |

| By Application |

Commercial Military Research Cargo Transport |

| Key Players |

Hybrid Air Vehicles Ltd. Lockheed Martin Corporation RosAeroSystems LTA Research & Exploration Zeppelin Luftschifftechnik GmbH Worldwide Aeros Corp Airborne Industries Flying Whales Skyship Services Inc. Aero Drum Ltd. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The non-rigid airship segment accounted for the largest market share in 2024, driven by widespread adoption for advertising and surveillance applications. Rigid and semi-rigid airships are gaining popularity in cargo transport and military applications due to their improved payload capacity and structural integrity.

The military and defense segment dominated with a 38.5% share in 2024, driven by increased adoption for intelligence, surveillance, and reconnaissance (ISR) missions. The commercial segment is expected to witness the highest growth, supported by airships’ increasing role in advertising, tourism, and cargo transport.

North America accounted for 35.2% of the global airship market share in 2024, driven by strong defense spending and ongoing research initiatives in the U.S. The U.S. military is investing in high-altitude, long-endurance (HALE) airships for persistent surveillance, while commercial players are exploring applications in cargo transport and tourism. The Federal Aviation Administration (FAA) is also streamlining regulatory frameworks to support commercial airship operations.

Europe holds a 29.1% market share, with countries like Germany, France, and the UK at the forefront of airship innovation. The European Union is funding research into hybrid airships as part of its sustainability initiatives. Companies such as Flying Whales and Hybrid Air Vehicles are developing airship solutions for cargo transport and disaster relief operations.

The Asia-Pacific region is expected to witness the highest CAGR of 9.3% during the forecast period, driven by rising defense investments in China and India. China is actively developing stratospheric airships for military surveillance, while Japan is investing in airship technology for urban transportation and disaster response. The growing logistics sector in Southeast Asia also presents significant opportunities for airship-based cargo transport.

Middle East and Africa are emerging markets for airships, particularly in security and infrastructure monitoring applications. The UAE and Saudi Arabia are exploring airship-based solutions for border surveillance and oil field monitoring. Africa’s interest in airships is growing for humanitarian aid and medical supply transport in remote regions.

Latin America is witnessing increased adoption of airships in advertising, tourism, and agricultural monitoring. Brazil and Mexico are leading the regional market, leveraging airships for aerial surveillance and environmental monitoring.

The global Airship market was valued at approximately USD 3.5 billion in 2024.

The market is projected to grow at a CAGR of 7.8% from 2026 to 2033.

Major drivers include increasing demand for aerial surveillance, the rise of sustainable cargo transport, and technological advancements.

Non-rigid airships lead the market due to their widespread use in advertising, tourism, and surveillance applications.

The military sector holds the largest share, followed by commercial applications.

North America leads with a 35.2% market share, followed by Europe at 29.1%.

The Asia-Pacific region is expected to grow at the highest CAGR of 9.3% from 2026 to 2033.

Major players include Hybrid Air Vehicles, Lockheed Martin, RosAeroSystems, LTA Research, and Zeppelin Luftschifftechnik.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Airship Market, By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Airship Market, By Application

6.1 North America Airship Market, By Country

6.1.1 Airship Market, By Type

6.1.2 Airship Market, By Application

6.2 U.S.

6.2.1 Airship Market, By Type

6.2.2 Airship Market, By Application

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping