Flight Simulator Market

Flight Simulator Market Size, Market Share & Trends Analysis Report By Platform (Commercial, Military, UAVs), By Solution (Products, Services), By Type (Full Flight Simulators, Flight Training Devices), By Region (North America, Europe, Asia-Pacific, Middle East and Africa, Latin America) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIADR1010

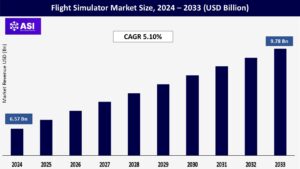

CAGR: 5.10%

Last Updated : May 18, 2026

The global Flight Simulator Market size was valued at approximately USD 6.57 billion in 2024 and is projected to reach USD 9.78 billion by 2033, growing at a steady CAGR of 5.10% during the forecast period (2026–2033).

Flight simulators are advanced technologies designed to recreate the experience of flying an aircraft in a safe and controlled environment. These systems play a crucial role in pilot training, research, and development. The growing demand for commercial pilots, increasing defense budgets, and technological advancements in simulation are key factors driving market growth.

The growing global air traffic has significantly increased the demand for new pilots. Airlines and aviation training centers are investing heavily in-flight simulators to provide cost-effective and efficient pilot training.

According to the International Air Transport Association (IATA), global air passenger traffic is expected to double by 2040, further fueling demand for simulators. Additionally, the increasing adoption of simulators for recurrent training and skill enhancement among experienced pilots is further propelling market growth.

Innovations in artificial intelligence (AI), virtual reality (VR), and enhanced graphics have improved the realism and effectiveness of flight simulators. Advanced motion systems and high-definition visuals are making simulation training more immersive, enhancing pilot skills and safety measures.

Moreover, the integration of cloud-based solutions for remote simulation training is providing cost-effective alternatives for pilot training institutions.

Operating real aircraft for pilot training is highly expensive, involving fuel, maintenance, and operational costs.

Flight simulators provide a more economical solution by allowing trainees to gain hands-on experience in a controlled and repeatable environment. Airlines and military organizations are increasingly adopting flight simulation technology to reduce training costs while maintaining high-quality learning experiences.

The development and deployment of full-flight simulators require significant capital investment. The cost of acquiring and maintaining these systems can be a barrier for smaller training centers and emerging markets.

Flight simulators must comply with stringent aviation regulations and certifications. Regulatory approvals from bodies such as the Federal Aviation Administration (FAA) and the European Union Aviation Safety Agency (EASA) add to operational complexity and costs.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Patform |

Commercial Military Unmanned Aerial Vehicles (UAVs) |

| By Solution |

Products

Services

|

| By Type |

Full Flight Simulators (FFS) Flight Training Devices (FTD) |

| Key Players |

DJI Parrot Drones AeroVironment, Inc. PrecisionHawk DroneDeploy Zipline Kespry Wing (Alphabet Inc.) FLIR Systems General Atomics |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The flight simulator market is categorized based on platform, solution, and type.

The commercial segment dominated the market in 2024, driven by rising air traffic and increased investments in pilot training programs by airlines. The military segment is also experiencing notable growth due to the increased focus on defense aviation training, particularly in countries with expanding defense budgets. Additionally, the UAV segment is gaining traction as drone applications increase in commercial and defense operations.

The products segment, which includes hardware and software components, held the largest market share in 2024. Advancements in high-fidelity motion platforms, augmented reality, and 3D visualization contribute to the segment’s growth. The services segment is expected to witness steady growth due to rising demand for outsourced training programs and maintenance services.

Full flight simulators (FFS) accounted for the largest market share in 2024, offering high-fidelity simulation experiences essential for comprehensive pilot training programs. Meanwhile, flight training devices (FTD) are gaining popularity as cost-effective alternatives that still provide critical training functionalities.

North America accounted for 36.0% of the global market share in 2024, driven by the presence of key players such as CAE Inc. and Boeing. The region continues to witness significant investments in aviation training, supported by strong airline and military aviation programs. The U.S. remains a key contributor, with the FAA pushing for enhanced training regulations that increase simulator adoption.

Europe held a 28.3% market share in 2024, with leading countries such as the UK, France, and Germany investing heavily in flight training infrastructure. The European aviation sector is also focusing on sustainability initiatives, which include increasing the use of simulators to minimize carbon emissions from real aircraft training.

The Asia-Pacific region is expected to grow at the highest CAGR of 6.2% during the forecast period. Rapid urbanization, growing air passenger traffic, and rising investments in airline fleet expansion in China and India are fueling market growth. Additionally, aviation training institutions in the region are adopting advanced simulation technologies to meet the increasing demand for qualified pilots.

The Middle East and Africa region is experiencing increased demand for flight simulators due to the rapid expansion of airline networks and aviation training centers. The UAE and Saudi Arabia are making significant investments in aviation training infrastructure to support their growing airline industries.

Latin America is seeing steady growth in the flight simulator market, led by Brazil and Mexico. Increased government initiatives to improve aviation safety and pilot training are contributing to market expansion.

The global flight simulator market was valued at approximately USD 6.57 billion in 2024.

The market is projected to grow at a CAGR of 5.10% from 2026 to 2033.

Increasing demand for pilot training, technological advancements, and cost-effective training solutions.

The commercial segment leads due to rising air traffic and pilot training demand.

North America leads with a 36.0% market share.

The Asia-Pacific region is expected to grow at the highest CAGR of 6.2% from 2026 to 2033.

Major players include CAE Inc., Boeing, L3Harris Technologies, Thales SA, and Saab AB.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Flight Simulator Market, By Platform

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Flight Simulator Market, By Solution

5.3 Flight Simulator Market, By Type

6.1 North America Flight Simulator Market, By Country

6.1.1 Flight Simulator Market, By Platform

6.1.2 Flight Simulator Market, By Solution

6.1.3 Flight Simulator Market, By Type

6.2 U.S.

6.2.1 Flight Simulator Market, By Platform

6.2.2 Flight Simulator Market, By Solution

6.2.3 Flight Simulator Market, By Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping