Vaccine Adjuvants Market

Vaccine Adjuvants Market Share & Trends Analysis Report, By type (Particulate Adjuvants, Aluminum-Based Adjuvants, Toll- Like Receptor Agonists) By Application (Human Vaccines, Infectious Disease, Influenza, Hepatitis, HPV, COVID-19 Others) By End User (Pharmaceutical Companies, Biotechnology Companies, Academic & Research Institutes, Contract Research Organizations (CROs) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

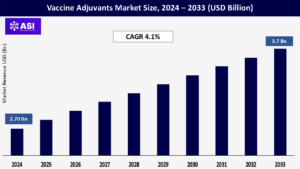

CAGR: 4.1%

Last Updated : July 17, 2025

Global Vaccine Adjuvants Market was around USD 2.70 billion in 2024 and is expected to reach USD 3.7 billion by 2033 at a CAGR of 4.1% during the forecast period (2025–2033).

Vaccine adjuvants are chemical substances that are added to vaccines to enhance the body’s immune response to an antigen, enhancing vaccine efficacy and duration of protection. The adjuvants activate the immune system to build a more effective defense against pathogens, with the duration of such defense being longer. Vaccine adjuvants are common in prophylactic and therapeutic vaccines, particularly where the antigen alone does not result in sufficient immunity. Growing dissemination of infectious diseases, ongoing development of cancer immunotherapies, and need for more potent and longer-lasting vaccines are key drivers for the market for vaccine adjuvants. Growth in biotechnology and adjuvant formulation is also fueling innovation and expanding their application in next-generation vaccines.

Development in vaccine delivery and formulation technology is also propelling the vaccine adjuvants market. Next-generation adjuvants are being developed with nanotechnology, synthetic biology, and lipid nanoparticle (LNP) delivery systems to achieve maximum immunostimulation with low reactogenicity. These new adjuvants not only enhance the immunogenicity of response but also facilitate antigen dose sparing, which is critical during pandemics and mass vaccination drives. For example, GlaxoSmithKline’s AS04 and Novavax’s Matrix-M adjuvants have become extremely potent to immunize humoral and cellular immune responses in licensed vaccines.

These success stories are encouraging greater interaction between biotech firms, research institutions, and pharma giants to further drive innovation in adjuvant technology. In the post-COVID era, big players such as Pfizer, Moderna, Sanofi, and Bharat Biotech have doubled their stakes on collaborative vaccine R&D, with most of them working on adjuvants as key components of next-generation platforms.

Further, higher investments in research in immunology and vaccinology are also driving the market growth. With further focus being placed on such diseases as RSV, dengue, chikungunya, Zika, and even cancer, the demand for adjuvanted vaccines continues to increase steadily.

Government initiatives targeting pandemic preparedness and bioterrorism defense are also robustifying the vaccine adjuvants market. Post-COVID-19 pandemic, all governments have redesigned their vaccines stockpiling strategies and invested in local manufacturing capacities for vaccines. Such organizations as the U.S. Biomedical Advanced Research and Development Authority (BARDA) and the European Medicines Agency (EMA) have heavily invested in adjuvanted vaccine development and stockpiling, including influenza, anthrax, and other priority pathogens.

The regulatory landscape has also been enhanced, with accelerated approval pathways and emergency use authorizations (EUAs) for vaccines and vaccine components, including adjuvants. Various adjuvants that were not previously licensed in the U.S. have been approved by the FDA for use in COVID-19 and other experimental vaccines, for instance.

This has made new adjuvant technologies more commercially appealing and promoted wider clinical adoption. Secondly, multilateral organizations and non-profits such as the Coalition for Epidemic Preparedness Innovations (CEPI) are spending significant amounts of money and scientific capital on adjuvant-based vaccine R&D, specifically for pandemic potential pathogens. These collective efforts can be expected to make adjuvants a integral component of the global immunization landscape.

While vaccine adjuvants are critical for immune stimulation and vaccine efficacy boost, issues of safety and tolerability are a restraining factor in the growth of the vaccine adjuvants market. Some adjuvants have been associated with local and systemic adverse reactions from injection site mild reactions to more severe immunological reactions, making them less easily used on a large scale, particularly in sensitive populations such as children, elderly, or autoimmune disease patients.

Perhaps the most extensively used adjuvant—aluminum salts (“alum”)—has been implicated in local inflammation, granuloma, and, in rare cases, long-term muscle pain and weakness, a condition commonly referred to as macrophagic myofasciitis (MMF). Although in some cases, a causal connection may not have been definitely established, chronic controversy and public concern surrounding aluminum-containing vaccines have created anxiety among segments of the population. This has led to vaccine hesitancy, particularly in countries with ongoing anti-vaccine activism.

The majority of side effects reported in association with vaccines are mild and transient, according to the U.S. Centers for Disease Control and Prevention (CDC), but adding adjuvants can increase the rate and intensity of side effects compared to non-adjuvant formulations. These reactions most typically include swelling, redness, pain at the site of injection, fever, and weakness—symptoms that, though generally self-limiting, might reduce vaccine acceptance in certain groups.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Particulate Adjuvants Aluminum-Based Adjuvants Toll- Like Receptor Agonists |

| By Application |

Human Vaccines Infectious Disease Influenza Hepatitis HPV COVID-19 Others |

| By End User |

Pharmaceutical Companies Biotechnology Companies Academic & Research Institutes Contract Research Organizations (CROs) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Aluminum-Based Adjuvants led the market in 2024 with a share greater than 42.5% in the vaccine adjuvants market. This is followed by decades of proven safety, cost-effectiveness, and regulatory clearance in pediatric and adult vaccines. Aluminum salts like aluminum phosphate and aluminum hydroxide are extensively used in diphtheria-tetanus-pertussis (DTP) and hepatitis, as well as HPV vaccines. Their extensive use in national immunization programs, especially among developing and middle-income nations, ensures long-term demand.

Particulate Adjuvants will witness the fastest growth over the forecast period due to their improved ability to mimic pathogens and provide better antigen presentation. This subcategory includes liposomes, virosomes, and virus-like particles (VLPs), which have shown excellent performance in vaccines based on subunits and mRNA. The fact that they can be used in conjunction with future vaccine platforms like mRNA (such as Moderna and Pfizer’s COVID-19 vaccines) places them at the forefront of adoption in future vaccine products.

Toll-Like Receptor (TLR) Agonists are gaining popularity, particularly in therapeutic vaccine design and late-stage immunotherapy development. TLR-based adjuvants such as CpG 1018 and MPL are increasingly being utilized to improve innate immunity and boost T-cell responses. Applications in hepatitis B, cancer, and RSV vaccines justify their expanding market share. However, tight regulatory focus and high development costs could limit their large-scale application in the short term.

Infectious Disease Vaccines accounted for the largest market share in 2024, with over xx% revenues. The high incidence of infectious diseases such as tuberculosis, hepatitis, malaria, and COVID-19 has driven the demand for effective, long-term vaccines in the world. Adjuvants play a critical role in eliciting immune response against highly mutable or poorly immunogenic pathogens, ensuring the dominance of this segment. Influenza and COVID-19 Vaccines are the primary growth drivers, especially in the post-pandemic era where seasonal booster doses and pandemic preparedness have become the world’s foremost health priority.

Adoption of advanced adjuvants like MF59 (used in Fluad) and Matrix-M (used in Novavax’s COVID-19 vaccine) has established a new benchmark of adjuvant innovation in combating respiratory viruses. Development of universal influenza vaccines is expected to propel long-term demand for high-performance adjuvant systems. Hepatitis and HPV Vaccines are expected to stay on track for continued growth, fueled by robust global immunization initiatives and increasing awareness of sexually transmitted diseases and liver ailments. Adjuvanted vaccines such as HEPLISAV-B (with CpG 1018) and Cervarix (with AS04) show how new adjuvants are improving vaccine performance and reducing the number of doses needed. Therapeutic Vaccine Applications for cancer, autoimmune disorders, and chronic viral diseases are emerging as high-growth opportunities. Although still in clinical development, adjuvant incorporation into therapeutic vaccine products—particularly those that evoke T-cell immunity—represent a shift toward more focused immunological strategies. These segments will gain market share as pipeline products move ahead in regulatory approvals.

Pharmaceutical Firms dominated the vaccine adjuvants market in 2024 with approximately xx%. Major vaccine players rely on adjuvant systems to enhance immunogenicity and improve the shelf-life of their vaccines. Major pharma companies such as GlaxoSmithKline, Sanofi, Pfizer, and Merck either have in-house facilities or strategic partnerships focused on adjuvant R&D. Their heavy investment in big-ticket clinical trials, production facilities, and regulatory submissions keeps them in the vanguard of the market. Biotech Companies will experience the most rapid growth, as their innovation leadership in next-generation adjuvants and novel delivery systems drives the market. Mid-tier biotechs and startups are increasingly entering into partnerships and licensing deals with majors to develop proprietary adjuvants, specifically for personalized vaccines, cancer immunotherapy, and emerging infectious diseases.

The largest driver of the vaccine adjuvants market in 2024 was North America and accounted for approximately 41.3% of the total global market. This is attributed to a developed infrastructure for vaccine research, strong government support, and the presence of leading pharmaceutical and biotech companies. The United States leads the way, driven by initiatives such as Project NextGen and the Biomedical Advanced Research and Development Authority (BARDA), which are steadfastly committed to investments in next-generation vaccine platforms, such as adjuvant technologies. The accelerated authorization and introduction of adjuvanted COVID-19 vaccines such as Novavax’s NVX-CoV2373 even attest to the region’s capability for innovation. In addition, elevated levels of infectious illnesses in aged communities and a growing focus on pandemic preparedness warrant ongoing demand for adjuvanted vaccines.

Europe remains a significant market for vaccine adjuvants, thanks to intensive pharmaceutical R&D and high-quality public health infrastructures. In 2024, the region held a global market share of approximately xx%. These include some of the top vaccine-developing countries and immunization programs: Germany, France, the United Kingdom, and the Netherlands. The European Medicines Agency (EMA) has approved several adjuvanted vaccines, including those based on the use of AS03 and MF59 adjuvants, more in influenza and hepatitis vaccines. The investment in Horizon Europe and the European Health Emergency Preparedness and Response Authority (HERA) by the EU continues to support novel adjuvant development. The region’s aging population and addressing antimicrobial resistance and vaccine-preventable diseases are among the factors that drive increased usage of adjuvanted formulations.

The Asia-Pacific is expected to record the highest growth in market for vaccine adjuvants, at a forecasted CAGR of 8.1% between the years 2024-2030. Extensively developing healthcare infrastructure, improving public health awareness, and increased government financing of immunization drive these factors. These nations include China, India, Japan, and South Korea. In the post-COVID-19 era, China’s assertive vaccine development approach has witnessed the use of adjuvanted formulations for indigenous vaccines as well as for export vaccines. India, as a prominent manufacturing hub for vaccines by organizations like the Serum Institute of India and Bharat Biotech, is looking to invest in next-generation adjuvants for domestic consumption and exports. Japan’s regulatory support for late-cycle biologics and geriatric populations also propel regional demand. Collaboration between international vaccine alliances (e.g., Gavi, CEPI) and Asian firms is also propelling use of new adjuvant technologies across the region.

Latin America and MEA are emerging markets for vaccine adjuvants, together occupying a smaller but growing share of the global market. In Latin America, Brazil and Mexico have dominance in regional production and use of vaccines. Public expenditure on immunization campaigns and increased application of WHO-approved vaccines fuel steady but moderate demand for adjuvanted vaccines. Economic inequalities and supply chain constraints, however, affect the pace of market growth.

In the Middle East & Africa, countries such as South Africa, Saudi Arabia, and the UAE are developing their role in adjuvant vaccine production and adjuvanted vaccine importation for diseases such as hepatitis, HPV, and COVID-19. The establishment of the African Medicines Agency by the African Union and increased financing by global health partners are set to enhance access to vaccines and production, and possibly extend the utilization of adjuvants.

The vaccine adjuvants market was valued at USD 3.70 billion in 2024.

The vaccine adjuvants market is projected to grow at a CAGR of 4.1% from 2025 to 2033.

The Aluminum- based Adjuvants hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Vaccine Adjuvants Market By Carrier Oil Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Vaccine Adjuvants Market, By Application

5.3 Vaccine Adjuvants Market, By Distribution Channel

6.1 Vaccine Adjuvants Market, By Country

6.1.1 Vaccine Adjuvants Market, By Type

6.1.2 Vaccine Adjuvants Market, By Application

6.1.3 Vaccine Adjuvants Market, By End User

6.2 U.S

6.2.1 Vaccine Adjuvants Market, By Type

6.2.2 Vaccine Adjuvants Market, By Application

6.2.3 Vaccine Adjuvants Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping