Telemedicine Market

Telemedicine Market Share and Trend Analysis, By Type (Products and Services), By Modality (Store-and-forward (Asynchronous), Real-time (Synchronous), and Others), By Application (Teleradiology, Telepathology, Teledermatology, Telecardiology, Telepsychiatry, and Others), By End-User (Healthcare Facilities, Homecare, and Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

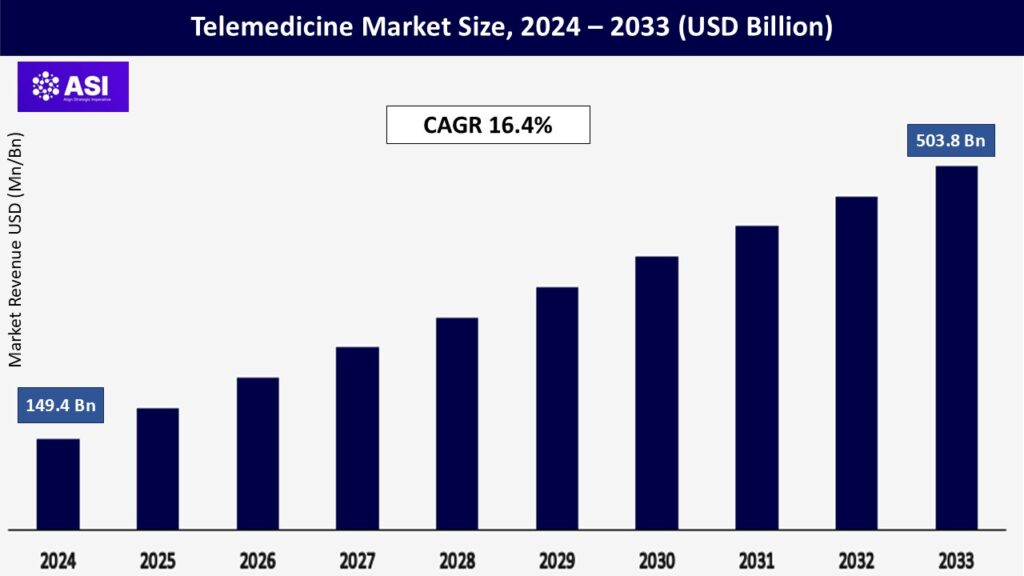

CAGR: 16.4%

Last Updated : May 5, 2026

The global telemedicine market size was valued at USD 149.4 billion in 2024 and is projected to reach USD 503.8 billion by 2032, expanding at a compound annual growth rate (CAGR) of 16.4% during the forecast period (2025 – 2033).

Telemedicine employs digital communication technologies to provide remote clinical services, thus increasing healthcare accessibility and efficiency. This expanding adoption is contributing to the overall telemedicine market size globally. The expansion is driven by a number of factors, such as the rising need for remote patient monitoring, improvements in telecommunication infrastructure, and the growing incidence of chronic diseases. Additionally, the incorporation of artificial intelligence and machine learning into telehealth platforms is enhancing diagnostic precision and allowing for more tailored care.

The COVID-19 pandemic also boosted the use of telemedicine, highlighting its significance in ensuring continuity of care and reducing infection risk. Government policies and positive reimbursement schemes have also supported market growth. Nonetheless, issues like data privacy, regulatory barriers, and the requirement of strong digital infrastructure in emerging regions can hinder growth. However, the telemedicine industry is on track for substantial growth, revolutionizing the delivery of healthcare and presenting new benefits for providers and patients alike. This transformation is redefining the global telemedicine industry.

The global prevalence of chronic diseases like diabetes, cardiovascular disease, and respiratory diseases has increased so much that more than 41% of adults globally have at least one chronic condition. Therefore, patients need to be monitored regularly and have regular follow-up visits, which puts a load on providers as well as healthcare systems. Additionally, aging populations in developed and developing countries are also fueling this demand further; for example, the use of telehealth among U.S. adults 65+ went up from 4.6% in 2019 to 21.1% in 2021, reflecting an unequivocal preference for remote care models that reduce travel and risk exposure.

Hence, telemedicine has come forth as an indispensable tool by facilitating ongoing chronic disease management via virtual consultations, remote monitoring of vital signs, and medication compliance support, cutting down hospital admissions by as much as 25% in some studies. Moreover, telemedicine platforms have broadened reach to rural and underserved regions; in India’s Ayushman Bharat program, teleconsultations increased by 500% between 2020 and 2023, which shows how distant healthcare connects spatial divides. Therefore, payers and patients are increasingly using telehealth solutions to enhance outcomes, reduce expenses, and provide more convenience. Advancement in R&D and Strategic Investments

Accelerated progress in broadband penetration and mobile coverage has set the stage for scalable telemedicine services. To date, in 2024, 83% of the world’s population had access to high-speed internet, and deployments of 5G reached 64 countries to support low-latency, high-definition video consultations. Furthermore, machine learning (ML) and artificial intelligence (AI) are now part of telehealth platforms; AI-based diagnostic software has demonstrated up to 90% accuracy in the interpretation of chest X-rays and dermatological photos, surpassing conventional techniques.

Additionally, predictive analytics use continuous streams of patient data to forecast health declines, reducing emergency department visits by 15% in pilot initiatives. In addition, conversational AI and chatbot integration simplifies triage processes, lowering clinician workload by 20% and increasing patient interaction through 24/7 symptom evaluation. As such, such technological innovations not only enhance diagnosis accuracy and individualized treatment regimens but also enable platform scalability and interoperability with electronic health records (EHRs). As a result, the union of intelligent software and high-speed connectivity is causing telemedicine to evolve beyond mere video visits into full-fledged virtual care systems. Such developments are reshaping the future of the telemedicine industry

Telemedicine providers usually face considerable challenges as a result of differing licensing requirements in different areas. For example, in America, doctors need to secure individual licenses to practice in every state, even if the consultations are virtual. The process is time-consuming and expensive and entails considerable fees and bureaucratic input. These intricacies make it difficult to provide telemedicine services smoothly across state borders.

Moreover, payment policies for telemedicine services are still mixed and frequently inadequate. Medicare, for instance, has traditionally capped telehealth reimbursement only to certain kinds of care and areas, mostly nonmetropolitan locations. This limits many patients’ access and provides fiscal disincentives for suppliers. Private payers also have different rates and policies of reimbursement, making their financial sustainability all the more complicated.

The exchange of confidential patient information on digital media entails serious privacy and security threats. There have been reported cases of data breaches, e.g., the leakage of more than 120,000 documents, including medical records and recordings of therapy sessions, from unsecured databases. Additionally, certain telehealth websites have been discovered to pass user information on to third parties via ad trackers and session recording software, which poses questions about the confidentiality of the patient. Medical professionals have to navigate a web of data protection laws, including HIPAA in the US.

Maintaining compliance with these laws and instituting strong cybersecurity practices are essential to upholding trust from patients in telemedicine services. Rapid growth of telehealth has outpaced the creation of authoritative privacy and security standards, creating gaps that might be targeted by criminals.

| Report Metric | Details |

|---|---|

| By Type |

Products Services |

| By Modality |

Store-and-Forward (Asynchronous) Real-Time (Synchronous) Others |

| By Application |

Teleradiology Telepathology Teledermatology Telecardiology Telepsychiatry Others |

| By End-User |

Healthcare Facilities Homecare Others |

| Key Players |

|

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The products segment includes the hardware and software essential tools that make it possible to deliver telemedicine services. Such tools include medical devices like digital stethoscopes, otoscopes, ECG monitors, and pulse oximeters, which allow for remote examination and diagnostics. Other tools in this segment are telemedicine carts, kiosks, wearable sensors, and mobile health (mHealth) devices, which provide ongoing patient monitoring. On the software side, video conferencing platforms, electronic health record (EHR) integration, remote imaging, scheduling, and data sharing make up the infrastructure of digital delivery of care. Such advancements are continuously expanding the telemedicine market size.

The adoption of these products is being spurred on by the requirement for scalable healthcare infrastructure, particularly in rural and underserved markets. In addition, the COVID-19 pandemic hastened the demand for home-based testing devices, which continue to perform a vital function in chronic illness management and post-surgical monitoring. With technological advancements in artificial intelligence and interoperability, the product segment will continue to be a significant driver of the telemedicine market.

The services segment includes services like teleconsultation, telemonitoring, telepsychiatry, teleradiology, and virtual education. The segment has witnessed exponential growth, with healthcare providers transforming their models from hospital-centric to patient-centric models. Services provide real-time and asynchronous communication, offload physical infrastructure, and boost clinical workflow efficiency. Increased insurer support and value-based care efforts are further fueling service adoption.

This modality permits medical information such as images, reports, or test results to be sent safely to a provider for later review. It is commonly applied in dermatology, radiology, and pathology, where immediate interaction is not required. Store-and-forward enhances access to specialists, particularly in remote locations, and increases efficiency in workflow by providing flexible scheduling and quicker diagnostic turnaround. Its use is expanding with the progress in imaging and secure cloud storage technology.

Real-time telemedicine consists of live video or audio communication between healthcare professionals and patients. It closely resembles face-to-face visits, allowing direct consultations, follow-up visits, and real-time evaluations. This method is widely applied in primary health care, mental health services, and the management of chronic diseases. With continued improvement in internet access and the ease of use of telehealth platforms, real-time consultations are increasingly becoming popular for their speed and ease of access.

This category consists of remote patient monitoring (RPM) and mobile health (mHealth) solutions. RPM equipment monitors vital signs such as heart rate, blood sugar level, and oxygen level, allowing chronic patients to receive around-the-clock care. mHealth applications help with patient education, medication adherence reminders, and lifestyle guidance. These solutions favor early intervention and are now more extensively incorporated into digital health programs globally.

Hospitals and clinics are significant consumers of telemedicine services, incorporating them into their healthcare delivery systems to improve patient care.

The homecare division is seeing a high-growth rate as patients prefer to receive medical treatment in the comfort of their homes, facilitated by distant monitoring technologies.

This segment involves schools, workplaces, and prisons that use telemedicine services to deliver healthcare access to certain groups.

North America is still the market leader in the global telemedicine market. In 2024, the region held a share of about 43.1% of the total global market share due to developed healthcare infrastructure, widespread digital health technology adoption, and favorable government policies. The U.S. telemedicine market alone was worth USD 32.3 billion in 2024 increasing at a CAGR of 18.25%. High incidence of chronic diseases, an ageing population, and rising demand for superior technology are the factors attributing to this growth.

Europe is also a leading region in terms of telemedicine market share, with the UK, Germany, and France taking top positions in adoption thanks to conducive government policy and rising health digitization. The region is further supported by high-developed healthcare systems and growing efforts towards minimizing health expenses via digital technologies. National health policy implementation and reimbursement for telemedicine have further driven adoption across the continent.

The Asia-Pacific region has the fastest-growing telemedicine market, with an estimated CAGR of 19.5% from 2024 to 2030. The growth is fueled by greater internet penetration, a high patient population, and growing demand for affordable healthcare services. These factors strongly support the telemedicine market growth in the region. Government programs in nations such as India and China to encourage telemedicine are also fueling this expansion.

Latin America telehealth market valued at USD xx billion in 2023 is and registering a CAGR of 24.1%. The high prevalence of chronic conditions, ageing population, and rise in adoption of digital healthcare solutions drive growth in the region. Brazil and Mexico are forerunners with high investment in telehealth infrastructure and accommodating regulations.

The telehealth market in the Middle East and Africa was valued at USD xx billion in 2024 and is expected to grow at a CAGR of 26.8% during the period 2025-2030. Improving internet connectivity, rising smartphone penetration, and initiatives by governments such as Saudi Arabia’s Vision 2030 are fueling the digitalization of healthcare in the region. The UAE led with the highest portion of 24.8% in 2024, led by initiatives to disseminate awareness and adopt telehealth platforms by patients and healthcare providers.

The global telemedicine market was valued at USD 123.1 billion in 2024.

The market is projected to grow at a CAGR of 16.4% from 2025 to 2033.

Major players include Teladoc Health Inc., American Well Corporation, MDLIVE Inc., Siemens Healthineers, GE Healthcare, Cerner Corporation, Cisco Systems Inc., Koninklijke Philips N.V., Medtronic, and Doctor on Demand Inc.

Services Segment hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Telemedicine Market By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Telemedicine Market , By Modality

5.3 Telemedicine Market , By Application

5.3 Telemedicine Market , By End User

6.1 North America Telemedicine Market, By Country

6.1.1 Telemedicine Market, By Type

6.1.2 Telemedicine Market, By Modality

6.1.3 Telemedicine Market, By Application

6.1.4 Telemedicine Market, By End User

6.2 U.S.

6.2.1 Telemedicine Market, By Type

6.2.2 Telemedicine Market, By Application

6.2.3 Telemedicine Market, By Modality

6.2.3 Telemedicine Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping