Autoimmune Therapeutics Market

Autoimmune Therapeutics Market Share & Trends Analysis Report By Drug Class (Anti-inflammatory Drugs, Nonsteroidal Anti-Inflammatory Drugs, Antihyperglycemics, Interferons, Biologics, Immunosuppressants, Immunomodulators¸ Others), By Disease Type (Rheumatoid Arthritis, Type 1 Diabetes, Multiple Sclerosis, Inflammatory Bowel Disease, Systemic Lupus Erythematosus, Psoriasis), By Distribution Channel (Hospitals, Specialty Clinics, Drug Stores, Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

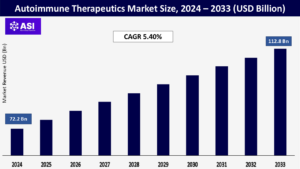

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIPHR1011

CAGR: 5.40%

Last Updated : August 7, 2025

The global Autoimmune Therapeutics Market was valued at approximately USD 72.2 billion in 2024 and is projected to reach USD 112.8 billion by 2033, growing at a CAGR of 5.40% during the forecast period (2025–2033).

The autoimmune disease therapeutics market is experiencing significant growth, primarily due to the rising prevalence of autoimmune disorders worldwide. Various factors, including genetic predisposition, environmental influences, and shifts in lifestyle, have contributed to the increasing incidence of these conditions. As cases continue to rise, the demand for more advanced and targeted treatments has surged, driving innovation in therapeutics. Additionally, the aging population, which is more vulnerable to autoimmune diseases, further contributes to the growing need for effective treatment solutions. Another key driver of market expansion is the rapid progress in biotechnology and pharmaceutical research. The introduction of biologics and immunotherapies has transformed the approach to managing autoimmune disorders, offering new treatment avenues for patients who previously had limited options.

Biologics have shown remarkable efficacy in conditions that were resistant to traditional therapies. Furthermore, pharmaceutical companies are heavily investing in research and development to enhance treatment effectiveness, ensuring continuous market growth. Greater awareness and improved diagnosis of autoimmune diseases also play a vital role in shaping the market landscape. Public health initiatives and educational programs have enabled better understanding of these conditions, leading to earlier detection and intervention. Timely diagnosis can significantly enhance patient outcomes, improving overall quality of life. Consequently, there is an increasing demand for therapies that address different stages of autoimmune diseases.

The rising awareness of health, especially the importance of early detection, is a key factor propelling the autoimmune disease diagnostics market. As people gain a deeper understanding of the risks and symptoms associated with autoimmune conditions, more individuals seek diagnostic testing. Detecting diseases at an early stage enhances treatment effectiveness, reducing the likelihood of severe complications. With healthcare systems increasingly emphasizing preventive care and timely intervention, the need for advanced diagnostic solutions for autoimmune diseases continues to grow.

The increasing prevalence of autoimmune diseases, such as rheumatoid arthritis, lupus, and Type 1 diabetes, is a key factor fueling the expansion of the autoimmune disease diagnostics market. As these conditions become more widespread, the demand for precise and early detection methods continues to rise. Enhanced awareness and advancements in diagnostic technology have encouraged individuals to prioritize early screening, driving market growth and the adoption of innovative healthcare solutions.

Technological advancements have led to the development of highly precise and automated diagnostic tests, enhancing the accuracy of autoimmune disease detection. Innovations such as advanced blood tests with increased sensitivity and specificity enable more effective biomarker identification, allowing for earlier and more accurate diagnoses. This, in turn, facilitates well-informed treatment planning. The integration of artificial intelligence and machine learning into diagnostic tools has significantly improved detection speed and accuracy, further accelerating market growth in autoimmune disease diagnostics.

One of the key obstacles in the autoimmune disease diagnostics market is the high cost associated with advanced testing methods. Technologies such as genetic screening and specialized blood tests often come with significant expenses, making them less accessible in lower-income regions. This financial barrier can lead to delays in diagnosis and treatment, particularly for patients with limited insurance coverage or restricted access to healthcare facilities offering these tests. As a result, market expansion is slowed due to affordability challenges and disparities in healthcare accessibility.

A significant challenge in the autoimmune disease diagnostics market is the lack of standardized testing methods across different regions. Autoimmune conditions are complex and often share symptoms with other diseases, making their diagnosis more challenging. Without universally accepted diagnostic criteria, inconsistencies in test results can arise, leading to delays in accurate diagnosis. Additionally, variations in diagnostic procedures among healthcare providers further complicate detection and treatment, making it difficult to ensure uniform and effective disease management.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Class |

Anti-inflammatory Drugs Nonsteroidal Anti-Inflammatory Drugs Antihyperglycemics, Interferons Biologics Immunosuppressants Immunomodulators Others |

| By Disease Type |

Rheumatoid Arthritis Type 1 Diabetes Multiple Sclerosis Inflammatory Bowel Disease Systemic Lupus Erythematosus Psoriasis |

| By Distribution Channel |

Hospitals Specialty Clinics Drug Stores Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Autoimmune Therapeutics Market is segmented by drug class and by disease application and by distribution channel. Each segment plays a crucial role in improving diagnostic therapeutic technologies, and growing awareness of the need for early detection and treatment.

The market for pharmaceuticals is categorized based on drug class, including anti-inflammatory drugs, antihyperglycemics, NSAIDs, interferons, and others. Among these, anti-inflammatory drugs have historically been the highest revenue-generating segment and are anticipated to maintain dominance in the coming years. This trend is driven by increasing demand for these medications, the introduction of new anti-inflammatory drugs, and supportive reimbursement policies in certain regions.

Additionally, the expected release of pipeline drugs such as tocilizumab, certolizumab, secukinumab, etanercept, and golimumab is likely to further boost market expansion.Anti-inflammatory medications play a key role in managing various inflammatory conditions, including inflammatory bowel disease, osteoarthritis, rheumatoid arthritis, fibromyalgia, systemic lupus erythematosus, gout, juvenile idiopathic arthritis, infectious arthritis, psoriatic arthritis, ankylosing spondylitis, reactive arthritis, scleroderma, and polymyalgia rheumatica.

The rising prevalence of these disorders continues to drive market growth.Currently, widely used anti-inflammatory treatments include Adalimumab, Etanercept, Infliximab, Abatacept, Certolizumab, Golimumab, Ustekinumab, Tocilizumab, and Secukinumab. Their availability and favorable reimbursement policies in select regions contribute to their sustained market growth.

The market for autoimmune disease diagnostics is segmented based on disease type, covering both systemic and localized conditions. Localized autoimmune diseases—such as inflammatory bowel disease, type 1 diabetes, and thyroid disorders—hold the largest market share due to their higher prevalence and the precision of diagnostic methods.Companies are actively developing advanced treatments to address these diseases.

Notably, AstraZeneca and Quell Therapeutics announced a collaboration in June 2023 to create engineered T-regulator (Treg) cell therapies aimed at providing curative solutions for type 1 diabetes and inflammatory bowel disease. Their approach leverages innovative cell engineering techniques, contributing to positive growth projections in the autoimmune disease diagnostics market

The report examines revenue trends in the pharmaceutical and healthcare industry across global, regional, and national markets, identifying key growth opportunities in various applications. It explores how advancements in pharmaceuticals, therapy solutions, and healthcare monitoring are shaping the industry’s landscape. Key aspects covered include market size, revenue contributions, and the role of technological innovations like AI-powered diagnostics. Regulatory developments and industry value chain insights—including major players and operational processes—are also highlighted.

The North American autoimmune disease therapeutics market is projected to hold 40.5% of the global revenue in 2025, amounting to a significant portion of the market. Future trends indicate continued expansion, with the market forecasted to reach approximately $107.2 billion by 2033 at a compound annual growth rate (CAGR) of 5.18%. Among North American countries in 2025, the United States is expected to dominate with 80.66% of the market share, while Canada and Mexico account for 12.19% and 7.15%, respectively.

The European autoimmune disease therapeutics market is projected to account for 18.40% of the global revenue in 2025. Among European countries, Germany is anticipated to hold the largest share at 24.20%, followed by the United Kingdom, France, Spain and other nations including Italy, Sweden, Switzerland, and Denmark, which contribute to the overall market distribution.

The Asia-Pacific autoimmune disease therapeutics market is projected to represent xx % of the global industry in 2025. Looking ahead, the market is expected to reach approximately $75.1 billion by 2033, with a compound annual growth rate (CAGR) of 6.46%. Among Asia-Pacific nations, China is projected to hold the largest, followed by Japan, India and other key markets, including South Korea, Australia, and Singapore, contributing to overall industry expansion.

The Middle Eastern autoimmune disease therapeutics market is expected to hold 3.44% of the global industry in 2025, contributing to the estimated xx billion global revenue. This sector has seen consistent growth with a compound annual growth rate (CAGR) of 5.85%. Among Middle Eastern nations, Saudi Arabia is forecasted to have the largest market share followed by Turkey, Egypt, the UAE, and Qatar with the rest of the region contributing 14.33% to the industry’s overall expansion.

The autoimmune therapeutics market was valued at USD 72.2 billion in 2024.

The autoimmune therapeutics market is projected to grow at a CAGR of 5.40% from 2025 to 2033.

The Anti-Inflammatory hold the largest market share of autoimmune therapeutics.

The North-America region is expected to witness the highest growth rate.

Major players include Abbott Laboratories (U.S.), Active Biotech (Sweden), Eli Lilly (U.S.), Bristol-Myers Squibb (U.S.), AstraZeneca plc (U.K.), Pfizer (Japan), Biogen Idec (U.S.),

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Autoimmune Therapeutics Market By Drug Class

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Autoimmune Therapeutics Market By Disease Type

5.3 Autoimmune Therapeutics Market By Distribution Channel

6.1 U.K.

6.2 Germany

6.3 France

6.4 Spain

6.5 Italy

6.6 Russia

6.7 Nordic

6.8 Benelux

6.9 The Rest of Europe

7.1 China

7.2 South Korea

7.3 Japan

7.4 India

7.5 Australia

7.6 Taiwan

7.7 South East Asia

7.8 The Rest of Asia-Pacific

8.1 UAE

8.2 Turkey

8.3 Saudi Arabia

8.4 South Africa

8.5 Egypt

8.6 Nigeria

8.7 Rest of MEA

9.1 Brazil

9.2 Mexico

9.3 Argentina

9.4 Chile

9.5 Colombia

9.6 Rest of Latin America

10.1 Global Market Share (%) By Players

10.2 Market Ranking By Revenue for Players

10.3 Competitive Dashboard

10.4 Product Mapping