Generic Drugs Market

Generic Drugs Market size, share, & Trends Analysis Report By Drug Type (Simple Generics, Super Generics),By Brand (Pure Generic Drugs, Branded Generic Drugs) , By Route of Administration (Oral, Injection, Cutaneous, Others) By Therapeutic Application (Central Nervous System (CNS), Cardiovascular, Infectious Diseases, Musculoskeletal Diseases, Respiratory, Oncology, Others), By Distribution Channels( Retail Pharmacy, Hospital, Pharmacy, Online and Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025-2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIPHR1011

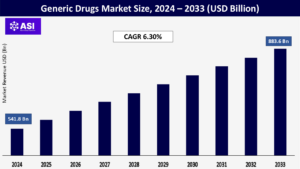

CAGR: 6.30%

Last Updated : July 17, 2025

The value of global generic drugs market was around USD 541.8 billion in 2024 and is expected to reach USD 883.6 billion by achieving a CAGR 6.30% during the forecast period (2025-2033)

Generic drugs are very important in bringing down the cost of healthcare while providing easy access to necessary medications. These pharmaceuticals are therapeutically similar to their branded counterparts and are commonly employed in the management of long-term diseases like diabetes, cancer, and cardiovascular disease. Drivers of the market include the patent expiries of blockbuster products, increasing pressure for cheaper medication, official policies encouraging the use of generics, and the rising rate of long-term diseases globally.

Due to the high cost of branded pharmaceuticals, healthcare costs have skyrocketed globally, making it more and more difficult for middle- and low-income groups to obtain necessary treatments. A long-term answer to this problem is provided by generic medications, which are therapeutically identical to their branded equivalents but are marketed for much less money. In an effort to ease financial burden, governments, insurance companies, and patients are aggressively moving toward generics. The U.S. FDA claims that generic drugs can save up to 85% of the cost of name-brand ones, saving the American healthcare system around USD 300 billion annually.

In the majority of countries, doctors and pharmacists are encouraged, if not mandated, to utilize generic medications as first-line treatments. For instance, the National Health Service (NHS) in the United Kingdom encourages generic prescribing in order to maintain the affordability of public healthcare. In India, Jan Aushadhi Kendras provide essential generics at discounted costs as part of initiatives like the Pradhan Mantri Bhartiya Janaushadhi Pariyojana. Generic medications are thereby improving prescription compliance and worldwide public health outcomes in addition to making therapy more inexpensive.

The “patent cliff,” or the expiration of patents on popular branded medications, is one of the factors propelling the generic medicine industry. Other businesses are permitted to produce bioequivalent versions of a medication, or generics, at a much reduced cost once the patent protection for that medication expires. Consequently, consumers and healthcare systems can gain from increased competition, faster market entry, and reduced prices. Patents on many of the most widely used drugs, such as diabetic treatments, anticoagulants, and cancer drugs, will expire between 2023 and 2030.

As an example, beginning in 2023, AbbVie’s top-selling immunology medication Humira (adalimumab) lost exclusivity in several regions, paving the way for generic and biosimilar substitutes to flood the market. When the initial biosimilar formulation came on the market in the US early in 2023, it instantly registered in terms of prescription and pricing patterns. Generic drugmakers are increasing production to take advantage of the more lucrative drugs that are moving off patent. Pharmaceutical companies thus have intense competition and a thriving international marketplace that will soon offer patients less expensive alternatives.

Though they are cheaper, generic drugs tend to create suspicion about their safety, quality, and efficacy in many countries, especially those developing, because of differences in regional regulations and production practices. Although regulatory bodies such as the U.S. FDA, the European Medicines Agency (EMA), and India’s CDSCO enforce strict regulation, not all production units globally are of equal standard. Quality failures, like contamination or strengths of dosing that do not match the prescription, have resulted in recalls and undermined trust on the part of the public.

For example, in 2018 and 2019, generic copies of the drug Valsartan for treating high blood pressure were recalled in Europe and the U.S. because the drugs contained cancer-causing impurities (NDMA and NDEA). These incidents not only damage customer confidence but also encourage stricter regulations, longer approval processes, and increased compliance costs for businesses. Furthermore, complex regulatory constraints are often too much for smaller generic medicine companies to handle, leading to delayed market introductions. As a result, even if generics significantly lower healthcare costs, persistent quality and regulatory concerns nonetheless limit the market’s expansion.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Type |

Simple Generics Super Generics |

| By Brand |

Pure Generic Drugs Branded Generic Drugs |

| By Route of Administration |

Oral Injection Cutaneous Others |

| By Therapeutic Application |

Central Nervous System (CNS) Cardiovascular Infectious Diseases Musculoskeletal Diseases Respiratory Oncology XOthers |

| By Distribution Channel |

Retail Pharmacy Hospital Pharmacy Online Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Of the drug types, plain generics maintain the largest market share. These are identical bioequivalent copies of off-patent brand medicines with exactly the same therapeutic effects at reduced prices. Their simplicity of manufacture and regulatory approval lends themselves to broad usage, particularly in price-sensitive markets. Super generics, while a smaller market, are emerging. These include generics with altered formulations, delivery systems, or therapeutic profiles. They are attractive to both regulators and patients for providing enhanced outcomes. For example, modified-release analgesics and re-formulated diabetes drugs are widening therapeutic choices with increased benefits.

From the brand category, branded generics dominate the market in developing countries such as India and Brazil. These medications are marketed under a brand name and offered at the same way as branded products but at affordable prices, providing credibility and recognition to the consumer. Pure generics, often sold by their International Nonproprietary Name (INN), are more common in highly regulated economies like the U.S. and UK where generic prescribing is promoted in order to save money. Branded generics contributed a considerable market share in 2024 with pharmaceutical firms spending a lot on branding even for generics.

Major segments are Oral, Injection, Cutaneous, and Others. Oral generics like tablets and capsules comprise the largest segment because of ease of manufacture, patient acceptability, and numerous therapeutic uses. Injectables are registering sharp growth, particularly in hospitals, spurred by growing demand for biosimilars and critical care medicines. For instance, generic oncology injectables are witnessing high demand owing to their cost-effectiveness. Cutaneous (dermal) and other routes such as ophthalmic or transdermal are niche yet emerging areas.

Segments are Central Nervous System (CNS), Cardiovascular, Infectious Diseases, Musculoskeletal Diseases, Respiratory, Oncology, and Others. Cardiovascular and CNS diseases dominate the market because these conditions are chronic in nature and have high worldwide prevalence. Hypertension, epilepsy, and depression generics are widely demanded. Oncology generics are increasing fast with patent expirations on cancer medications making cheaper chemotherapy and biologic options available. Infectious disease therapy, including generic antibiotics and antivirals, is also important, especially in lower-income countries. TheCOVID-19 pandemic sped this segment for a short while.

Key channels are Retail Pharmacy, Hospital Pharmacy, Online Pharmacy, and Others. Retail pharmacies control the distribution market, particularly in developing markets where over-the-counter availability is ubiquitous. Hospital pharmacies are needed for injectable and life-saving generics, mainly for institutional use. Online pharmacies are quickly becoming popular, aided by the healthcare digitalization and home delivery convenience. For instance, in India and the U.S., online pharmacy platforms such as GoodRx and NetMeds have registered massive sales of generic medicines after 2020. Others are government-sponsored shops such as India’s Jan Aushadhi Kendras.

North America leads the world’s generic drugs market with around 37.5% of total market share in the year 2024, propelled mainly by the United States, which boasts one of the strongest generic pharmaceutical sectors in the world. The region enjoys well-established regulatory infrastructures, including the FDA’s Abbreviated New Drug Application (ANDA) process allowing for quick-track approval of generics. The financially prudent choice of healthcare providers and payers and patent expirations of Big Pharma blockbusters have provided a rich soil for generics. The region’s expected CAGR stands at 6.2% for 2025–2032, with biosimilars and specialty generics experiencing maximum growth.

Europe holds the second-largest share, with an expected CAGR of 6.7% between 2025 and 2032. Countries like Germany, the UK, and France are key contributors, backed by supportive pricing regulations, aging populations, and widespread adoption of generic prescribing. The European Medicines Agency (EMA) simplifies generics approval across the member states, further increasing accessibility. Measures to reduce healthcare spending have prompted national initiatives that encourage generic substitution within public healthcare systems.

Asia-Pacific is the fastest-growing region, fuelled by large populations, expanding healthcare infrastructure, and rising chronic disease prevalence. India, China, and Japan are at the heart of the momentum of the region. India is renowned as “the pharmacy of the world” and is a major producer and exporter of generic drugs, helped by low-cost production and a huge pool of skilled manpower. China is increasingly embracing generics via policy reforms and price controls. The region is expected to expand at a CAGR of 8.9% over 2025-2032.

Latin America represents an emerging market with strong growth potential, particularly in Brazil, Mexico, and Argentina. Growth driven by emergence of a middle-class population, surging government support for generic substitution, and investments in local manufacturing are the growth drivers. Initiatives to contain healthcare spending and make medicines more affordable are boosting market penetration.

Middle East & Africa (MEA) remains in an early growth phase, but market opportunities are enhancing with increasing demand for healthcare and an expanding pharmaceutical manufacturing base. South Africa, Saudi Arabia, and UAE are the most dynamic markets. Local production incentives and development of healthcare infrastructure by governments are also driving adoption. While pricing and regulatory issues continue to be a factor, the region will grow at a CAGR of 6.5% during 2032, thanks to need for cheap medicine and increased chronic disease incidence.

The generic drugs market was worth USD 541.8 billion as of 2024

The generic drugs market is projected to grow at a CAGR of 6.30% from 2025 to 2033.

The generic pure drugs has the largest market share

The Asia-pacific region is likely to experience the largest growth rate

Major players of generic drugs are Teva Pharmaceutical Industries Ltd, Sandoz (a division of Novartis), Sun Pharmaceutical Industries Ltd, Mylan N.V. (a subsidiary of Viatris), Cipla Ltd., Lupin Pharmaceuticals, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Generic Drugs Market, By Drug Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Generic Drugs Market, By Brand

5.3 Generic Drugs Market, By Route of Administration

5.4 Generic Drugs Market, By Therapeutic Application

5.5 Generic Drugs Market, By Distribution Channel

6.1 North America Generic Drugs Market, By Country

6.1.1 Generic Drugs Market, By Drug Type

6.1.2 Generic Drugs Market, By Brand

6.1.3 Generic Drugs Market, By Route of Administration

6.1.4 Generic Drugs Market, By Therapeutic Application

6.1.5 Generic Drugs Market, By Distribution Channel

6.2 U.S.

6.2.1 Generic Drugs Market, By Drug Type

6.2.2 Generic Drugs Market, By Brand

6.2.3 Generic Drugs Market, By Route of Administration

6.2.4 Generic Drugs Market, By Therapeutic Application

6.2.5 Generic Drugs Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping