Air Ambulance Market

Air Ambulance Market Share and Trend Analysis, By Technology (Rotary-Wing, Fixed-Wing), By Application (Inter-facility Transfer, Rescue Helicopter Service, Organ Transport Logistics, Infectious Disease Cases, Neonatal & Paediatric Transport), By End Users (Hospital-based, Independent Service, Government & Military) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 9.8%

Last Updated : May 7, 2026

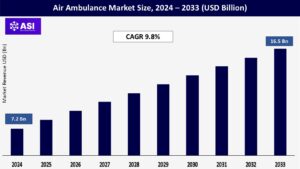

The global air ambulance market size was valued at USD 7.2 billion in 2024 and is projected to reach USD 16.5 billion by 2033, expanding at a compound annual growth rate CAGR of 9.8% during the forecast period (2025 – 2033).

Air ambulance services offer critical, immediate airborne medical transport for seriously ill or injured patients when ground ambulances are not practical because of distance or the unavailability of terrain. These critical operations employ two principal platforms: rotary-wing aircraft (helicopters) for rapid scene response and short transfers, reaching remote or heavily congested locations, including fixed-wing aircraft for effective long-distance travel, such as international repatriation. Experienced, highly specialized medical crews onboard provide advanced, continuous care in flight, essentially flying intensive care units. Their function is irreplaceable in all high-stakes situations: urgent transport for injured victims, between-facility transfer to specialist centres (such as stroke or heart centres), care of complex neonatal/paediatric crises, orchestrating timely organ transplant arrangements, and conducting disaster response evacuations.

Central to the imperative is the “golden hour” paradigm – optimized survival and recovery rates through drastically compressed time to definitive care for time-critical conditions. Ongoing technological advances improve capabilities, such as safer, more effective aircraft, sophisticated onboard medical gear reproducing hospital-level capabilities, and enhanced real-time communication systems connecting airborne crews with ground-based physicians. Increased demand is driven by demographic trends such as aging populations that need sophisticated care, chronically high rates of trauma and high-acuity cases, and healthcare systems tending to centralize specialized treatment, which demands effective and efficient patient-transfer networks. These elements anchor air ambulances as essential parts of emergency medical infrastructure in the contemporary world. The growing reliance on rapid medical transport solutions is positively influencing global air ambulance market size.

Deep demographic aging, especially severe in North America, Europe, and Japan, is a core driver of air ambulance demand. Older populations bear a disproportionate share of complicated, life-threatening chronic illnesses, cardiovascular emergencies such as heart attack, disabling strokes, acute respiratory failure needing sophisticated ventilation, and fragility fractures commonly necessitating advanced orthopaedic surgery. Perhaps most importantly, definitive treatment of these high-acuity illnesses is often localized to remote tertiary hospitals or specialized facilities (comprehensive stroke units, cardiac cath labs, level 1 trauma centers), far beyond the ability of proximal community facilities. Air ambulances are the sole reliable option for quick, safe inter-facility transport over large distances, having a direct effect on survival rates and functional recovery by significantly lessening the time-to-intervention, particularly in the critical “golden hour” time frame.

This need is growing stronger: Japan’s population over 65 now stands at over 30% of the population, driving unrelenting service use. In parallel, CDC reporting verifies steady elevations in age-adjusted coronary artery disease and cerebrovascular event rates among the US elderly, directly associated with increased air medical activations for emergent transfers. The intersection of increasing longevity, increasing chronic disease burden, and the strategic concentration of high-cost specialty services leads to a sustained, structural demand for expedited, airborne critical care transport, inexorably driving market expansion. Urbanization patterns also add to this, focusing specialist facilities far from rural older adults.

The incessant global burden of major trauma, with rising natural disasters, places a massive strain on air ambulance services. Road traffic crashes (RTCs), a major global cause of death and disabling injury (WHO ~1.19 million deaths per year), disproportionately affect developing countries with rapid motorization but without proportionate road safety infrastructure or development of trauma systems. Helicopter Emergency Medical Services (HEMS) are critical to the on-scene removal of critically injured patients, those with traumatic brain injury, unstable spinal cord injuries, severe internal bleeding, or multiple polytrauma, and their rapid transport straight to definitive trauma care, greatly enhancing survival probabilities where ground transportation time is precluded. At the same time, global warming adds to noticeable rises in the magnitude, intensity, and territorial extent of natural disasters (hurricanes, large floods, earthquakes, forest fires), overloading local healthcare facilities and making huge tracts of land inaccessible by road.

Air ambulances become central to disaster medical response, conducting urgent extractions of the critically wounded from remote areas, quickly transporting skilled medical personnel and equipment to clogged field hospitals, and effecting inter-facility transports when local hospitals are destroyed or saturated. This two-pronged imperative, the ongoing pressure from high-level serious trauma events necessitating quick scene response and the surge capacity demand for increasingly common large-scale disaster medical operations, represents a central, non-discretionary driver for expansion and investment in air ambulance services and fleets worldwide. Military-medical partnerships during disasters only increase this demand.

Air ambulance operations have extremely high operational costs that generate substantial market headwinds. They are a result of buying and maintaining advanced aircraft, procuring specialized equipment used in in-flight critical care, and hiring well-trained flight crews with special aviation and medical certifications. Aviation fuel, extensive insurance protection, and being prepared to spring into action at a moment’s notice contribute significantly to recurring expenses. The total cost per patient transport is significant. Although payment by insurance companies, including governmental programs, falls far short of the actual costs incurred by providers in terms of reimbursement in a consistent way, especially for government payers, the shortfall produces an unstained financial burden on the providers.

In an attempt to cover the gap, providers tend to charge patients personally for the unpaid amount, causing severe individual financial hardship, high rates of patient discontent, and high levels of uncollectible debt for the firms. The experience of dealing with complicated insurance claims, recurring controversies over coverage, and collecting patient payments creates substantial administrative burden and financial uncertainty. This inherent incompatibility between high-cost operations and low reimbursement is a primary constraint on the larger marketplace. It discourages new services investment and expansion of infrastructure, which may restrict availability in economically underprivileged areas and for those with insufficient insurance coverage, ultimately confining patient access to this vital care modality. Addressing these financial barriers remains a critical challenge for the air ambulance industry.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Rotary-Wing (Helicopters) Fixed-Wing (Aircraft)

|

| By Application |

Inter-facility Transfer Rescue Helicopter Service Organ Transport Logistics Infectious Disease Cases Neonatal & Pediatric Transport

|

| By End User |

Hospital-based Services Independent Service Providers Government & Military Services

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Rotary-wing aircraft, and also mainly helicopters, provide the frontline response for emergency sites and shorter patient transport. Their vertical takeoff and landing capability is invaluable, making it possible to access isolated areas, congested urban areas, hilly country, and crash sites that conventional ambulances cannot reach. Fixed-wing aircraft, covering all types of airplanes from turboprops to jets, meet the paramount requirement for efficiently and comfortably covering long distances. They are the workhorse for long-distance transfers, such as overseas repatriation flights and scheduled inter-facility transfers where rapidity is of essence but helicopter constraints such as operational range, payload capacity, or inclement weather conditions render them unfeasible.

Demand is strong in both types. While helicopters retain their critical position for instant emergency response and urban HEMS (Helicopter Emergency Medical Service), fixed-wing transport is seeing significant expansion, especially for complicated, long-distance patient logistics involving extended airborne intensive care over long flight times, as an expression of the globalization of specialized medical needs and accelerating medical tourism travel between continents. This increasing demand for long-distance medical transport is contributing to air ambulance market size expansion.

Patient transfer from one healthcare facility to another represents the most common use case for air ambulances. This dominance is a direct result of health care systems placing advanced, high-tech treatments – including major trauma, acute stroke treatment, complicated cardiac surgery, and serious burn management – within specialized tertiary centers, requiring urgent transfer from resource-poor community hospitals. Rescue from accident scenes or inaccessible points continues to be the most basic and essential use, with the immediate extraction and transport being vital for survival in major trauma, where a few minutes of delay can be pivotal. Organ movement for transplant is a specialized, high-growth niche market segment with increasing transplant activity volume worldwide and the sheer requirement to deliver very stringent organ preservation windows across frequently wide geographic distances.

Pediatric and neonatal transfers require highly specialized, miniaturized technology and crews well-trained to deal with the special physiological concerns and intensive care needs of infants and children in flight. Patients with severe, highly infectious diseases are transported in special aircraft configurations with heavy-duty airborne isolation pods and negative pressure capability, a strong requirement highlighted vividly by recent worldwide pandemic incidents that necessitated stringent biocontainment during patient transport.

Independent firms running specialized air ambulance fleets are a typical and important business model, which is often awarded single-service contracts by hospitals, municipal/state government departments, and large private insurance carriers to serve specific areas or population segments. Hospital-based programs are a strategically expanding market, led by large healthcare centers that attempt to vertically integrate key transport services under their operational umbrella. This enables large hospital systems to extend their geographic service area or catchment zone effectively, ensure seamless, coordinated movement of patients within their own integrated care systems, improve overall service coordination for critically ill patients who need continuity of care, and harvest related revenue streams.

Government and military-owned air medical services provide unique public service and national security requirements, addressing mostly large-scale public health crises, global disaster medical response and mass casualty evacuation, offering subsidized or free basic services to geographically remote, frontier, or poor rural communities with no private coverage, and performing specialized combat medical evacuations (MEDEVAC) and personnel recovery operations for active duty military forces deployed in the continental United States or abroad. Every model deals with particular market needs and funding streams.

North America, and in particular the United States, holds the biggest worldwide air ambulance market share. The reason for this is very high per capita health spending, widespread networks of subspecialty hospitals requiring constant inter-facility patient transport, high volumes of traumatic injuries, and an established (if contentious) reimbursement system. There exists a big, dynamic private air ambulance provider base with hospital-based programs. Advanced ground and air medical infrastructure facilitate high utilization levels. The demand environment is also influenced by huge geographical distances, remote areas, and a high prevalence of conditions requiring quick specialist treatment, all backed by comparatively advanced emergency response systems.

Europe is a mature air ambulance market, with a high level of government regulation and inclusion within national or regional public health systems. Services are usually funded or fully subsidized by the public sector and guaranteed extensive coverage albeit within controlled operational parameters. Demand drivers are mainly through fast-growing aging populations that demand sophisticated care transfers and unhindered cross-border patient flows engendered by cross-border healthcare arrangements and harmonized protocols. Helicopter Emergency Medical Services (HEMS) are an important and visible component, well integrated into trauma systems in both urban and rural environments. Such integration is helping Europe sustain a strong air ambulance market share.

The Asia Pacific region has the highest world growth rate. This boom is fuelled by huge investments fast-tracking healthcare infrastructure, burgeoning medical tourism with international patients in need of repatriation, increasing disposable incomes allowing access, rising health insurance penetration, and population densities as high as they are in major countries. Some regions also experience high-frequency natural disasters, generating intense demand for airborne medical evacuation and logistics. Regions such as China, India, and Australia are leading growth drivers, each with its own dynamics – ranging from building comprehensive trauma networks through to catering to massive remote interiors or enabling international patient flows – fuelling strong fleet growth and service development. These developments are expected to strengthen air ambulance market size across emerging economies.

The LAMEA region offers a highly differentiated and emerging market. Wealthy Gulf Cooperation Council (GCC) countries propel segments with high expenditures on healthcare, sophisticated medical tourism centers, and servicing distant oil/gas operations’ demand. Latin America, particularly Brazil and Mexico, holds promise through urbanization, economic development, and developing trauma system improvements. Africa is beset with acute challenges: services are only partially based in large urban centers, mining areas, or are dependent upon humanitarian relief, with acute funding and infrastructure limitations restricting wider access. Throughout LAMEA, huge rural and low-income bases are still largely underserved, with apparent needs, making the growth environment a challenging one.

The global air ambulance market was valued at USD 7.2 billion in 2024.

The air ambulance market is projected to grow at a CAGR of 9.8% from 2025 to 2033.

The Inter-facility hold the largest air ambulance market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Airbus Helicopters, Leonardo S.p.A., Bell Textron Inc., Textron Aviation Inc., Pilatus Aircraft Ltd., Lockheed Martin Corporation.

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Air Ambulance Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Air Ambulance Market, By Application

5.3 Air Ambulance Market, By End User

6.1 Air Ambulance Market, By Country

6.1.1 Air Ambulance Market, By Technology

6.1.2 Air Ambulance Market, By Application

6.1.3 Air Ambulance Market, By End User

6.2 U.S

6.2.1 Air Ambulance Market, By Technology

6.2.2 Air Ambulance Market, By Application

6.2.3 Air Ambulance Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping