Bronchoscopes Market

Bronchoscopes Market Share and Trend Analysis, By Technology (Flexible Bronchoscopes, Rigid Bronchoscopes, Hybrid/Advanced Bronchoscopes), By Application (Diagnostics, Therapeutics, Surgical Procedures), By End Users (Hospitals, Ambulatory Surgical Centers (ASCs), Diagnostic Centers, Specialty Clinics) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

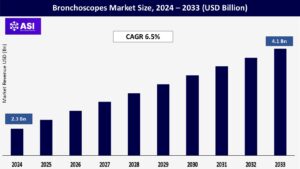

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.5%

Last Updated : May 9, 2026

The global Bronchoscopes Market size was valued at USD 2.3 billion in 2024 and is projected to reach USD 4.1 billion by 2033, expanding at a compound annual growth rate CAGR of 6.5% during the forecast period (2025 – 2033).

Bronchoscopes are advanced medical devices, basically thin tubes with lighting and optics, allowing physicians to look deep into a patient’s airways and lungs.”. Doctors thread these scopes up the nose or mouth and down the trachea to see clearly. Their primary task is diagnosing what’s amiss when a patient has difficulty breathing, recurring coughs, or lung spots on a scan. They do this by taking small samples of tissue (biopsies) or washes of lung fluid to analyze in a lab. Outside of diagnosis, these devices are becoming ever more important for therapies.

Trained professionals employ bronchoscopes to extract mistakenly inhaled materials, insert stents to keep narrowed airways open, end annoying bleeding, or even deliver focused heat or cold treatment to annihilate small tumors obstructing airways. The industry is all about supplying these vital instruments, from classic fiber-optic scopes to sophisticated video equipment and newer single-use technology, to hospitals and clinics across the globe to address the growing need to examine and treat intricate lung diseases.

Numerous individuals across the globe battle serious lung conditions, directly swelling the demand for bronchoscopes. Conditions such as COPD, which progressively destroy airways, affect thousands and thousands of people. COPD is usually managed by repeated bronchoscopies to treat sudden exacerbations or issues. Lung cancer, one of the major cancer killers, relies almost exclusively upon these scopes. Physicians utilize them to detect cancer in its early stages by removing tissue samples from suspicious areas and determining how widespread it is within the chest.

Severe infections, such as tuberculosis and complicated pneumonias, particularly in vulnerable patients, often require a bronchoscopic examination. Even after patients have recovered from serious COVID-19, residual lung injury, such as scarring, may require examination with a scope. With more people living longer and air quality not improving, these debilitating breathing issues are not disappearing. This steady increase equates to more patients needing the specialized capabilities of bronchoscopes, both to determine what is ailing and to treat it, driving the market steadily upwards.

Dramatic advances in what bronchoscopes are capable of doing and how they operate are revolutionizing the way physicians utilize them, driving up their use. Transitioning from outdated fiber-optic scopes to new video models is a gigantic leap forward. Video scopes project much higher-quality images on large screens. This increases the accuracy of identifying issues and allows the entire medical team to view what is occurring, making complex procedures less complicated and safer.

Tagging on added imaging tricks, such as Narrow Band Imaging (NBI), identifies small early cancer signs that normal light cannot detect. The introduction and rapid adoption of one-time use, throw-away bronchoscopes address significant headaches. They eliminate the fear of germ transmission among patients and cut back the enormous time and resources invested in cleaning reused scopes repeatedly. This is crucial for infection prevention and in emergency conditions. New robotic assistants and specialized scopes for procedures such as Endobronchial Ultrasound (EBUS) are also opening up tantalizing opportunities for more gentle lung exams and treatments, drawing investment and forcing hospitals to equip themselves better.

The high cost factor associated with bronchoscopy presents a big hurdle, particularly in regions with limited budgets or third-world nations. Purchasing one high-quality video bronchoscope costs a small fortune, sometimes approaching tens of thousands of dollars. That is only the beginning. Hospitals must also have costly matching gear: video processors, intense-focus lights, monitors, and special instruments such as biopsy grabbers or needles. This adds up to a tremendous up-front expenditure. On reusable scopes, the cost does not end there. They are a constant, expensive hassle requiring trained personnel, expensive chemicals, special testing equipment, and replacing them when they inevitably malfunction.

Disposable scopes avoid the expense of cleaning them, but the cost of buying a new one every time accumulates versus amortizing the cost of a reusable scope over lots of patients. The treatment itself, especially complex treatments, can be highly costly because of operating room expenses, specialist physician time, anesthesia, and laboratory studies. What is reimbursed by insurance or government programs usually doesn’t reimburse completely these actual costs. This money crunch makes it more difficult for clinics to make investments and can restrict patient access, particularly when healthcare funding is poor.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Flexible Bronchoscopes Rigid Bronchoscopes Hybrid/Advanced Bronchoscopes

|

| By Application |

Diagnostics Therapeutics Surgical Procedures

|

| By End User |

Hospitals Ambulatory Surgical Centers (ASCs) Diagnostic Centers Specialty Clinics

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Flexible bronchoscopes are the market leaders, preferred for patient tolerance and exploring complex airways. Video bronchoscopes are firmly supplanting fiber-optic bronchoscopes with significantly better high-definition imaging, better ergonomics to decrease operator fatigue, and digital recording to document and teach. Rigid bronchoscopes still have the necessary use for particular high-risk procedures requiring a sturdy tool, like removing large airway obstructions (e.g., food, dentures) or controlling severe, life-threatening bleeding. The most aggressive growth is in hybrid and advanced segments.

Disposable, single-use bronchoscopes are quickly gaining popularity, eliminating almost entirely the risks of cross-contamination and the enormous labor and resource intensity of reusing scopes – indispensable for infection control and emergency situations. Robotic-assisted bronchoscopy systems improve accuracy for peripheral lung nodule navigation. Endobronchial Ultrasound (EBUS) scopes are a significant innovation, combining real-time ultrasound imaging to facilitate safe and precise biopsies of structures near the airways, most importantly lymph nodes, revolutionizing lung cancer diagnosis and staging. These advancements are the core of market development and future growth potential.

Diagnostic applications constitute the underlying use case for bronchoscopes. This involves direct visualization of the tracheobronchial tree to detect abnormalities, along with the important sampling procedures: forceps biopsies for tissue diagnosis of cancer or infection, bronchoalveolar lavage (BAL) to harvest deep lung fluid for microbiological or cytological examination, bronchial washing, and transbronchial needle aspiration (TBNA) for sampling peribronchial lymph nodes or masses. Endobronchial Ultrasound (EBUS) has become invaluable, with the utilization of ultrasound guidance in real-time TBNA, markedly enhancing lung cancer staging accuracy. Therapeutic use is the most rapidly growing category.

The primary therapeutic applications are the physical extraction of aspirated foreign bodies within the airways and the insertion of stents to ensure patency within obstructed or compressed airway segments. More common are newer energy-based procedures: laser ablation for tumor debulking, electrocautery for hemostasis or tissue removal, cryotherapy for tumor ablation or debulking by freezing, and argon plasma coagulation for superficial bleeding or tumor coagulation. Balloon bronchoplasty expands stenosed airways, and bronchial thermoplasty delivers controlled heat to decrease airway smooth muscle in severe refractory asthma. This trend reflects the growing role of interventional pulmonology.

Hospitals, especially large tertiary and academic teaching hospitals with specialized pulmonology and thoracic surgery units, continue to be the preponderant buyers. These centers handle the largest volume and most complicated cases, requiring a complete range of bronchoscopes (flexible, rigid, EBUS) and accessories, complemented by specialized personnel and facilities such as operating rooms and intensive care. Ambulatory Surgical Centers (ASCs) are growing most quickly. Pursued by cost-saving healthcare systems favoring outpatient treatment, ASCs are increasingly doing diagnostic bronchoscopies (biopsies, BAL) and less involved therapeutic procedures (small foreign body extraction, simple stent placement).

Diagnostic imaging facilities are mainly engaged in offering outpatient diagnostic bronchoscopy services, forwarding the therapeutic cases further. Specialty clinics, especially large independent pulmonology groups, are a new emerging segment. Driven by practice economics and patient convenience, these clinics are opening in-office bronchoscopy suites, which usually include video towers and prefer disposable scopes for easier diagnostic procedures and surveillance tests. This trend decentralizes access to bronchoscopy but requires proper physician training and facility accreditation standards. Cost pressure in clinics and ASCs enhances demand for disposable scopes and value-driven capital equipment.

North America dominates the bronchoscope market. This dominance is due to high-quality hospitals, extensive use of sophisticated equipment such as video and disposable scopes, and high healthcare expenditures. High incidence of lung ailments such as COPD and cancer drives constant demand. Compared to other areas, reimbursement of procedures is often more prevalent, promoting adoption. This blend of advanced infrastructure, tech adoption, disease prevalence, and supportive payment systems makes it its leading position, underpinning steady market activity and innovation in the region.

Europe is a large, mature bronchoscopes market. High-quality healthcare systems and a high emphasis on quality care support demand, which is enhanced by a growing elderly population with greater need for respiratory diagnostics. Expansion continues unabated, sustained by the integration of newer technologies such as video bronchoscopy and EBUS to enhance lung cancer detection and staging. Nevertheless, entry into and development in the market can be hindered by the region’s strict regulatory guidelines governing medical devices, increasing complexity and duration to bring new products to market versus in certain other regions.

The Asia-Pacific region displays the world’s highest rate of bronchoscope market expansion. Large populations, increasingly modernized hospitals and clinics, and improved patient access drive this growth. Increased incomes enable more individuals to pay for sophisticated care, as increasing knowledge among physicians and enhanced understanding of lung health increase demand. The growth of medical tourism destination centers in nations such as India and Thailand, where high-quality procedures are provided at lower prices, further drive adoption. This intersection of variables produces explosive potential for diagnostic and therapeutic bronchoscopy throughout the region.

The LAMEA region demonstrates fragmented but consistent bronchoscope development. Latin America experiences gradual advancement, fueled by economic growth and targeted healthcare investment in nations such as Brazil and Mexico. The Middle East, particularly affluent GCC countries, sees growth driven by high expenditure on healthcare per capita and advanced medical equipment. Africa is extremely challenged; access is drastically underdeveloped outside larger cities because of resource shortages and infrastructure deficiencies, though nascent development is taking place in a few urban areas. Growth prospects contrast sharply across this highly varied region.

The global Bronchoscope market was valued at USD 2.3 billion in 2024.

The market is projected to grow at a CAGR of 6.5 % from 2025 to 2033.

Flexible Bronchoscopes hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Olympus Corporation, KARL STORZ SE & Co. KG, HOYA Corporation (Pentax Medical), Ambu A/S, Boston Scientific Corporation, FUJIFILM Holdings Corporation, Richard Wolf GmbH, Cook Medical, EMOS Technology GmbH, and Vathin Medical.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Bronchoscopes Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Bronchoscopes Market, By Application

5.3 Bronchoscopes Market, By End User

6.1 North America Breast Implants Market , By Country

6.1.1 Bronchoscopes Market, By Technology

6.1.2 Bronchoscopes Market, By Application

6.1.3 Bronchoscopes Market, By End User

6.2 U.S.

6.2.1 Bronchoscopes Market, By Technology

6.2.2 Bronchoscopes Market, By Application

6.2.3 Bronchoscopes Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping