Capnography Device Market

Capnography Device Market Share and Trend Analysis, By Technology (Mainstream Capnography, Sidestream Capnography), By Application (Anesthesia Monitoring, Critical Care Unit (ICU) Monitoring, Procedural Sedation, Emergency Medicine, Home Healthcare), By End User (Hospitals, Ambulatory Surgery Centers & Outpatient Clinics, Emergency Medical Services (EMS), Home Healthcare Providers & Sleep Laboratories) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

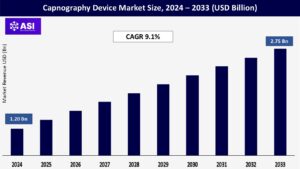

CAGR: 9.1%

Last Updated : May 9, 2026

The global capnography device market size was valued at USD 1.20 billion in 2024 and is projected to reach USD 2.75 billion by 2033, expanding at a compound annual growth rate CAGR of 9.1% during the forecast period (2025 – 2033).

Capnography, widely employed in operating rooms, intensive care units, and emergency departments, tracks the level of carbon dioxide (CO₂) in a patient’s exhaled breath, offering real-time measurement of ventilation status and respiratory function. Capnography monitors include mainstream sensors (directly attached at the airway) and sidestream analyzers (sensing gas through a small tubing line). Anesthesia providers count on these devices to monitor anesthesia adjustments, verify endotracheal tube placement, identify hypoventilation or apnea, and monitor pulmonary blood flow dynamics in resuscitation situations.

With healthcare professionals placing greater emphasis on patient safety and trying to minimize perioperative complications, there is now a growing demand for accurate, reliable, and easy-to-use capnography solutions. Technological innovations like microstream sampling, compatibility with multi-parameter monitors, and wireless communication have also expanded the device’s clinical applications further. Increasing recognition of the value of continuous CO₂ monitoring, particularly in high-dependency areas, firmly establishes capnography as an accepted standard of care in both inpatient and ambulatory health care environments.

Over the past decade, initiatives by professional associations such as the American Society of Anesthesiologists (ASA) and the World Federation of Societies of Anaesthesiologists (WFSA) have strongly advocated for continuous capnography during sedation and general anesthesia. Ensuring precise ventilation monitoring helps clinicians identify early signs of hypoventilation, airway obstruction, or disconnections in the breathing circuit, each of which can lead to severe hypoxia if not addressed promptly. Hospitals and ambulatory surgical facilities have incorporated capnography into their routine operative protocols to reduce perioperative adverse outcomes.

In addition, the Joint Commission and several North American and European accreditation organizations now mandate capnography use in anesthesia safety checklists, influencing de facto unit purchasing determinations. Consequently, even modest-sized surgical clinics and dental practices are embracing portable capnography modules in conjunction with pulse oximetry to meet patient safety requirements. Ultimately, increased clinician perception of the medico-legal and clinical advantages of capnography has contributed to steady market expansion, especially in economically advanced economies with strict regulations for anesthesia monitoring.

Improved miniaturization of sensors, gas sampling technology, and digital signal processing have widened the capability and performance of capnography equipment. Microstream technology, whereby a minimal-flow sampling line draws exhaled air continuously to a distant analyzer, has decreased the volume of sample needed to 50 mL/min. The innovation decreases the potential for airway obstruction and allows use with neonates and children. At the same time, mainstream infrared sensors have become smaller and more rugged, opening the door to direct in-line measurements that avoid sampling latency and deliver instantaneous breath-by-breath CO₂ waveforms.

Suppliers have also concentrated on embedding capnography modules into multi-parameter patient monitors so clinicians can display CO₂ values along with ECG, SpO₂, blood pressure, and temperature on a single touchscreen. Wireless connectivity options now enable remote monitoring of capnography trends, facilitating tele-ICU services and centralized monitoring across large hospital campuses. The addition of artificial intelligence (AI)-driven algorithms to identify subtle waveform abnormalities further extends clinical applications, e.g., early detection of sepsis and real-time monitoring of sedation depth, thereby expanding end-use opportunities and prompting hospital procurement of sophisticated capnography systems.

While capnography devices provide unambiguous clinical benefits for the prevention of adverse events, their fairly high costs of acquisition and maintenance can hinder uptake, especially in resource-poor environments. An independent mainstream sensor system will be two or three times more expensive than standard pulse oximeters. Sidestream analyzers necessitate frequent sampling line and filter replacements, as well as regular calibration by experienced biomedical engineers, contributing to the cost of ownership. In small clinics or rural hospitals in developing markets, tight budgets tend to favor the most necessary monitoring devices, and capnography gets postponed or skipped.

Also, regular maintenance requirements like yearly infrared light source replacement, software upgrades, and sensor recalibration—require a committed service agreement, driving operating expenses higher. More than the technology itself, healthcare systems need qualified staff who are well-trained in the analysis of capnography waveforms and the elimination of artifacts. In most low- and middle-income nations, access to such specialized anesthesiologists or respiratory therapists is limited. Therefore, even with increasing clinical data in favor of continuous CO₂ monitoring, cost limitations and shortages of staff still delay wide market penetration in cost-sensitive markets.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Mainstream Capnography Sidestream Capnography (Microstream) |

| By Application |

Anesthesia Monitoring Critical Care Unit (ICU) Monitoring Procedural Sedation Emergency Medicine (Pre-hospital & Ambulance) Home Healthcare (Sleep Centers) |

| By End User |

Hospitals (Operating Rooms & ICUs) Ambulatory Surgery Centers & Outpatient Clinics Emergency Medical Services (EMS) Home Healthcare Providers & Sleep Laboratories |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Capnography equipment is divided mainly into Mainstream Capnography and Sidestream Capnography, each having its own unique operational features. Mainstream Capnography entails positioning an infrared CO₂ sensor directly into the patient’s airway, usually between the mask or endotracheal tube and the breathing circuit. This positions the sensor for real-time breath-by-breath analysis with little to no lag time. Direct airway placement of the sensor, however, does increase weight and dead-space volume, which can be problematic for neonates and pediatric patients. Mainstream devices are preferred in operating rooms and intensive care units where rapid feedback is needed, and bulk from the sensor is not an issue.

Sidestream Capnography works by extracting a small, constant amount of expired gas (e.g., 50–200 mL/min) via a narrow tubing line to a distant analyzer contained in a portable module. This technique lightens the load on the patient’s airway adapter, making it more appropriate for spontaneous breathing patients and neonatal applications. Sidestream analyzers are available to be incorporated into transport monitors, procedural sedations, and ambulance installations.

The minimal lag, usually less than one second between exhalation and display of data, is deemed acceptable in most clinical situations. New advances encompass microstream technology, which further decreases the sampling volume needed and increases tubing life. Although mainstream devices tend to come with high prices, sidestream devices are attractive to cost-sensitive providers because of their modular architecture and reduced initial costs.

The versatility of capnography cuts across several clinical applications, such as Anesthesia Monitoring, Critical Care Unit (ICU) Monitoring, Procedural Sedation, Emergency Medicine, and Out-of-Hospital Care. Under Anesthesia Monitoring, anesthesiologists depend on capnography to guarantee that patients receive proper ventilation throughout induction, maintenance, and emergence phases. Abrupt waveform flattening or alarm-mediated hypoventilation warning facilitates instant intervention, minimizing perioperative morbidity. ICU Monitoring employs capnography in invasively and non-invasively ventilated patients to monitor respiratory status continuously, direct weaning protocols, and early recognize inadvertent endotracheal tube dislodgments or circuit disconnections.

During Procedural Sedation, capnography is an accepted standard of care in gastroenterology suites, dental offices, and radiology departments. Early identification of respiratory depression under conscious sedation procedures minimizes the risk of hypoxic events. In Emergency Medicine, paramedics with field-capable capnography machines are able to monitor patients in transit, checking vital ventilation in trauma patients, overdose patients, or respiratory failure. Lastly, in Out-of-Hospital Care, sidestream capnography-enabled pre-hospital monitors with specialized features aid first responders in quality-assured ventilation during CPR, providing real-time feedback on the effectiveness of chest compressions and directing advanced life support.

End users of the capnography equipment include Hospitals (Operating Rooms & ICUs), Ambulatory Surgery Centers and Outpatient Clinics, Emergency Medical Services (EMS), and Home Healthcare / Sleep Centers. Tertiary care hospitals with high surgical volumes and dedicated trauma centers are the largest segment of the capnography market. They need to have constant CO₂ monitoring to meet anesthesia safety guidelines and for complicated critical care cases. Ambulatory Surgery Centers (ASCs) and Outpatient Clinics have also embraced portable, space-saving capnography devices in order to handle conscious sedation with minor procedures reducing recovery times and enhancing patient throughput.

Emergency Medical Services (EMS) represent another expanding segment. Paramedic units and air-ambulance services need portable, battery-operated monitors with sidestream capnography modules to monitor ventilation during transport. This immediate feedback is essential in trauma cases and cardiac arrest treatment, where capnography-aided chest compressions enhance resuscitation success. In Home Healthcare and Sleep Centers, capnography is employed in conjunction with polysomnography to diagnose sleep-disordered breathing monitoring end-tidal CO₂ variability in obstructive sleep apnea patients. As reimbursement for home respiratory monitoring increases, there will be increased demand for easy-to-use capnography machines that can be telemonitored.

The North American region dominates the international capnography device market due to developed healthcare infrastructure, strict patient safety standards, and early embrace by professional societies of anesthesia. The United States dominates with a majority share, where hospitals and ambulatory surgical centers all use capnography for procedural and critical care applications.

Canada’s single-payer system also favors extensive capnography utilization, especially in CAUTI prevention guidelines. Heavy R&D spending by leading OEMs and supportive reimbursement policies for anesthesia monitoring devices also fuel regional expansion, leading to high demand for both mainstream and sidestream solutions.

Europe is the second-largest capnography market, led primarily by Germany, the UK, and France, in which regulatory authorities require capnography during moderate-to-deep sedation and general anesthesia. The European Society of Anaesthesiology (ESA) and the National Health Service have published guidelines recommending ongoing CO₂ monitoring in operating rooms and ICUs.

Eastern European nations are increasingly implementing capnography as healthcare budgets continue to grow. Elevated per-capita healthcare expenditure, continuous hospital upgrading programmes, and pan-European tenders for multi-parameter monitors with capnography modules embedded continue to drive continuous market growth throughout the continent.

The Asia-Pacific region is set for quick capnography market expansion due to the development of China, India, Japan, and Australia’s healthcare infrastructure. Greater awareness of perioperative security, together with increasing surgical volume, boosts demand for precise ventilation monitoring tools.

The government of China has boosted investment in hospital modernization, while private chains of hospitals in India are quickly embracing state-of-the-art anesthesia monitors. In Japan and Australia, strict clinical guidelines and quality care guarantee capnography uptake in community and tertiary hospitals. Cost-conscious markets like Southeast Asia are experiencing slow adoption with local distributors providing tiered sidestream systems.

Latin America and Middle East & Africa (MEA) are developing markets for capnography, where economic instability and irregular reimbursement strategies are challenges. Brazil, Mexico, and Argentina are the leading Latin American countries incorporating capnography in major private hospitals and surgical centers.

In the MEA region, Gulf Cooperation Council (GCC) nations, particularly Saudi Arabia and the UAE, invest heavily in healthcare modernization, leading to increased capnography device imports. Conversely, much of Sub-Saharan Africa remains underserved, with limited access to anesthesia monitoring infrastructure. However, public–private partnerships and international aid initiatives are progressively building critical care monitoring capacity in a limited number of countries.

The global capnography device market was valued at USD 1.20 billion in 2024.

The capnography device market is projected to grow at a CAGR of 9.1 % from 2025 to 2033.

The Mainstream hold the largest market share of capnography device.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Philips, Masimo, Dräger, Medtronic

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Capnography Device Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Capnography Device Market, By Application

5.3 Capnography Device Oil Market, By End User

6.1 North America Capnography Device Market, By Country

6.1.1 Capnography Device Market, By Technology

6.1.2 Capnography Device Market, By Application

6.1.3 Capnography Device Market, By End User

6.2 U.S.

6.2.1 Capnography Device Market, By Technology

6.2.2 Capnography Device Market, By Application

6.2.3 Capnography Device Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping