Connected Medical Device Market

Connected Medical Device Market Share and Trend Analysis, By Technology Type (Wireless Devices, Wired Devices, Hybrid Devices), By Application (Remote Patient Monitoring, Chronic Disease Management, Diagnostic Devices, Treatment Devices, Wellness and Fitness Devices), By End User (Hospitals & Surgical Centers, Home Care Settings, Specialty Clinics, Ambulatory Surgical Centers, Others) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 11.2%

Last Updated : August 6, 2025

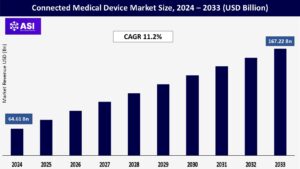

The global Connected Medical Device Market was valued at USD 64.61 billion in 2024 and is projected to reach USD 167.22 billion by 2033, expanding at a compound annual growth rate (CAGR) of 11.2% during the forecast period (2025–2033).

Networked healthcare devices are transforming medicine with the capability to exchange information in real time among patients, providers, and caregivers. The networked devices include wireless diagnostic devices, implantable sensors, wearables fitness trackers, and intelligent drug delivery devices. They all gather and send health data, with applications ranging from preventative care to early detection, tracking post-surgery, and chronic disease management. Through integration with cloud computing, artificial intelligence, and secure wireless networks, these devices enable round-the-clock monitoring of patients and prompt medical interventions.

This creates a more proactive and individualized style of healthcare that increases patient involvement and enhances outcomes. The growth in the market is fueled by increasing consumer awareness, growing prevalence of chronic diseases, and the worldwide transformation to value-based care. While healthcare systems strive to reduce costs and expand access, networked medical devices are increasingly facilitating reimagination of existing paradigms of care, making healthcare more efficient, accessible, and patient-centric than ever.

These technologies allow caregivers to continuously track critical patient vital health signs – i.e., cardiac rhythm, blood pressure, blood oxygen, and blood glucose – in real-time, from a distance, without taking care out of the classic clinical setting. On-going evolution of real-time data streaming capabilities offer multiple times earlier detection of early deteriorating health or developing complications, which can allow on-time, life-saving interventions. The effect is significant on patients with generalized chronic condition care (diabetes, heart failure, COPD), helping older individuals remain independent in their homes and allowing successful post-operative convalescence without a course of hospital appointments.

For patients as well, even the issue of convenience about not needing to make several, occasionally time-consuming, hospital or clinic appointments matters, enhancing satisfaction and compliance with monitoring regimes. Concurrently, the healthcare system benefits with clearly lowered emergency visit and avoidable hospitalization costs. The COVID-19 pandemic served as a powerful catalyst which hastened adoption and underscored the natural need for strong digital infrastructure and reliable connected devices. Most importantly, governments and payers are energetically driving this change with progressively supportive reimbursement policies for RPM services. As the world healthcare trend shifts towards more preventive, patient-centric, and proactive care paradigms, connected medical devices that form the backbone of RPM and telemedicine have become essential devices, enhancing outcomes and optimizing resource utilization across the entire continuum of care.

Backbone technology innovation is fueling growth in the market for connected medical devices. Rapid advances in miniaturization allow the devices to be smaller, more unobtrusive, and more comfortable to wear around the clock. Simultaneously, sensor technology development delivers higher accuracy and sensitivity in detecting physiological information, and wireless communications developments (e.g., Bluetooth Low Energy, 5G, and medical-specific frequencies) deliver low-power, secure data transfer. Most revolutionary, however, is the profound integration of Artificial Intelligence (AI) and the Internet of Things (IoT). Artificial intelligence technologies base their operations on the high amount of data produced by such devices and provide complex analytics beyond mere monitoring.

Some examples include recognizing subtle patterns, anticipating probable adverse effects (e.g., anticipating a hypoglycemic event in a diabetic patient or anticipating atrial fibrillation from heart rate variability), and creating individualized recommendations for intervention. IoT platforms serve as the nervous system, connecting heterogeneous devices – implantables, home monitors, wearables – to one another, to electronic health records (EHRs), and to telehealth platforms. It provides an integrated, real-time picture of the patient. Examples include AI-based wearables that alert for cardiac arrhythmias or smart insulin pumps that automatically adjust dosage in response to continuous glucose monitor feedback. This convergence of technology significantly enhances diagnosis accuracy, customization of care, and clinical workflow productivity and, further, empowers patients with relevant information regarding their own health care. Ongoing innovation promises even more intelligent, even more secure, and even more connected solutions.

The greatest advantages of networked health devices are offset by ongoing fear for data security and privacy since the devices generate and share highly sensitive patient health information (PHI), thus becoming prime targets for cyberattacks in pursuit of data theft, fraud, or sabotage. Successful compromises can be catastrophic in effect, breaching patient confidentiality, inhibiting necessary clinic procedures, inflicting possible physical damage as fraudulent data or device conduct, and dismantling cornerstone trust in health digital technologies. The character of the Internet of Medical Things (IoMT) infrastructure that unifies heterogeneous devices and platforms doubles threats through multiple security protocols, vintage systems, insecure patches, or physical tampering.

Compliance with robust global standards such as HIPAA and GDPR involves substantive technical and financial expenditures, including the use of robust encryption (at rest and in transit), access controls, audit trails, and secure storage, potentially beyond the means of smaller suppliers and producers. Application of end-to-end security controls such as robust encryption, multi-factor authentication, real-time monitoring, and regular patching is thus a requirement and not an option for facilitating long-term market expansion. Such trust among providers and patients can only be realized and guaranteed by being able to prove beyond a shadow of doubt the security, integrity, and confidentiality of health data.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Wireless Devices Wired Devices Hybrid Devices

|

| By Application |

Remote Patient Monitoring Chronic Disease Management Diagnostic Devices Treatment Devices Wellness and Fitness Devices

|

| By End User |

Hospitals & Surgical Centers Home Care Settings Specialty Clinics Ambulatory Surgical Centers Others

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The market of connected medical devices is segmented mainly by base connectivity technology, and prevailing among them are wireless technologies (Wi-Fi, Bluetooth, Zigbee, cellular networks such as 4G/5G). This is attributed to their intrinsic strengths: patient mobility liberty, convenience of integrability with implanted networks and consumer equipment (tablets, smartphones), and facilitating real-time continuous data transmission. These characteristics make wireless most appropriate for home care, remote patient monitoring (RPM), and ambulatory settings where patient mobility ranks top. Physical technologies (USB, Ethernet, medical-use specialized cables), however, provide greater reliability and embedded security through physical connection and are the first choice in operating rooms, intensive care units, and high-acuity hospital areas where unbroken, high-fidelity data transmission is not a possibility.

Hybrid systems that blend wireless and wired devices are increasingly common, especially in multicomplex hospitals. They add necessary redundancy and make connectivity transparent when patients are being transferred between areas of treatment (e.g., ER to ward). Selection of technology is also dominated by considerations such as range required, power issues, cost considerations, bandwidth data requirements, and timeliness demanded by the respective clinical application. As more wireless infrastructure (particularly 5G) is made secure, energy efficient, and resilient, this will be the default choice for most new installs to enable the transition towards decentralized, patient-centred models of care.

Internet of Things (IoT) connected medical devices are applied in various places in the healthcare sector. Remote Patient Monitoring (RPM) and Chronic Disease Management is the largest and the most rapidly growing segment. Devices such as continuous glucose monitors (CGMs), networked blood pressure cuffs, and pulse oximeters facilitate round-the-clock, real-time data collection for illnesses such as diabetes, heart failure, hypertension, and COPD, which can lead to early treatment, personalized care plans, and lower hospitalizations. Diagnostic Applications utilize networked devices to facilitate rapid, precise diagnoses, such as point-of-care testing (e.g., network-capable ECGs, ultrasounds), digital stethoscopes for heart/lung sound transfer, and mobile ophthalmoscopes to facilitate remote and clinic-based diagnostics.

Treatment-Focused Devices deliver adaptive therapy with patient feedback in real-time; examples include adaptive insulin pumps that adjust based on CGM levels, network-capable CPAP machines monitoring sleep apnea therapy adherence and response, and remote-programmable neuromodulation devices. Consumer Health and Fitness Wearables (such as activity monitors, smart scales, and simple heart rate monitors), though not medical grade per se, are increasingly found in use for preventive care, lifestyle management, and early warning sign detection and dump their data into larger health ecosystems. Connecting these isolated devices to telehealth systems and Electronic Health Records (EHRs) doubles their worth in value exponentially, rendering networked devices as focal resources in facilitating proactive, individualized, and data-driven styles of healthcare provision.

End User Hospitals and Surgical Centers represent the largest end-user market for connected medical devices today. This is propelled by their huge patient volumes, mature IT and clinical infrastructures in place, huge purchasing power, and the absolute imperative for integrated, interoperable systems to function and serve complex workflows, assure patient safety, and increase operating efficiencies in ICUs, ORs, and general wards. But the fastest growth is quite evidently occurring in the Home Care Settings segment. It is driven by strong macro trends: strategic realignment towards decentralized, value-based care, aging populations’ need to live longer in place, increased prevalence of chronic conditions that need to be managed over the long term, and patients’ desire for greater convenience and engaged care.

Specialty Clinics (cardiology, oncology, dialysis) and Ambulatory Surgical Centers (ASCs) are large and expanding adopters, using networked devices for improved pre/post-procedure care, improved patient flow, and improved outcomes in the ambulatory environment. Diagnostic Laboratories (connecting networked analyzers), Emergency Medical Services (EMS), and Long-Term Care Facilities (nursing homes, rehab facilities) are also heavy end users. With healthcare models worldwide focusing more on value-based results, patient centrality, and resource stewardship, adoption of networked medical devices by all end-user groups is growing, enhancing clinical performance, patient experience, and overall health-care effectiveness.

North America dominates the market with cutting-edge healthcare infrastructure, high digital health uptake, and favorable reimbursement (e.g., Medicare reimbursement for RPM). Giants drive innovation, strong FDA regulations, and more than investment in R&D. Strong patient/provider adoption and 5G rollout allow for scale. Gaps in interoperability and security are the pain points. Value-based care models become more dependent on connected device data for outcome-based reimbursement.

Europe has a big market share, supported by EU digital health endeavors (e.g., EHDS) and proactive GDPR. Aging populations and universal health coverage are drivers of demand for remote monitoring. Chronic disease management and cross-border telehealth (e.g., Nordic projects) are growth drivers. Integration and fragmentation are present, but priority is being given to interoperability standards to support long-term growth.

Growth segment, driven by increasing healthcare expenditure, large populations, and mHealth uptake (India’s Ayushman Bharat). Government backing, network expansion, and Chinese, Japanese, and Indian consumers who are tech savvy drive innovation. Telehealth growth, AI implementation, and point-of-care diagnostics drive the industry. Convergence of regulations is an issue.

Demonstrating gradual growth with infrastructural advancements and investment in telemedicine. Public health programs (e.g., UAE AI initiatives, Brazil’s Conecte SUS) and rising chronic disease loads are motivating factors. Limiting reimbursements and connectivity continue but PPPs and epidemiological surveillance programs are solid long-term prospects.

The global connected medical device market was valued at USD 64.61 billion in 2024.

The connected medical device market is projected to grow at a CAGR of 11.2 % from 2025 to 2033.

The Radiofrequency-based renal denervation segment holds the largest market share of connected medical device.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Medtronic plc, ReCor Medical Inc. (Otsuka), Abbott Laboratories, Boston Scientific Corporation, Ablative Solutions Inc., Terumo Corporation, and Symap Medical.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Connected Medical Device Market, By Technology Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Connected Medical Device Market, By Application

5.3 Connected Medical Device Market, By End User

5.1 North America Connected Medical Device Market, By Country

6.1.1 Connected Medical Device Market, By Technology Type

6.1.2 Connected Medical Device Market, By Application

6.1.3 Connected Medical Device Market, By End User

6.2 U.S.

6.2.1 Connected Medical Device Market, By Technology Type

6.2.2 Connected Medical Device Market, By Application

6.2.3 Connected Medical Device Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping