Continuous Blood Glucose Monitoring Market

Continuous Blood Glucose Monitoring Market Share and Trend Analysis, By Technology (Real-Time CGM (rtCGM), Intermittently Scanned CGM (isCGM), Implantable CGM, Non-Invasive CGM), By Application (Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes Mellitus, Prediabetes & Wellness, Pediatric Diabetes), By End User (Home Healthcare, Hospitals & Clinics, Specialty Diabetes Centers, Digital Health & Wellness, Clinical Research Organizations) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

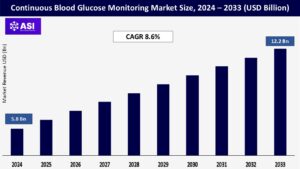

CAGR: 8.6%

Last Updated : August 6, 2025

The global Continuous Blood Glucose Monitoring Market was valued at USD 5.8 billion in 2024 and is projected to reach USD 12.2 billion by 2033, expanding at a compound annual growth rate CAGR of 8.6% during the forecast period (2025 – 2033).

Continuous glucose monitoring (CGM) systems include subcutaneous sensors, transmitters and display units (receivers or smartphone applications) that offer real-time or near-real-time glucose results. Interstitial fluid glucose at regular intervals is measured by CGMs, which allow for closer glycemic control, prevention of hypoglycemia and therapy adjustment based on data for type 1 and type 2 diabetic patients. Coupling with insulin pumps, smart pens and digital health platforms also enables closed-loop “artificial pancreas” solutions.

Adoption has grown across home care and hospital environments, fueled by increasing diabetes prevalence, technology improvements in sensor precision and connectivity, and widening reimbursement models. End users include endocrinology clinics and diabetes clinics, primary-care practices, and individual consumers looking for proactive glucose control. While healthcare models focus on value-based care, CGMs are known to lower hospitalization rates, enhance quality of life and reduce long-term complication expenses cementing their central position in contemporary diabetes care.

The worldwide increase in the number of diabetes cases is a leading driver prompting the use of CGM. As life changes and populations grow older, another million more people develop diabetes every year, so controlling blood sugar is essential to avoid serious complications such as nerve damage or heart problems. Physicians and payers increasingly support CGM technology since real-world evidence demonstrates it allows individuals to reduce their blood sugar levels and steer clear of harmful highs and lows more effectively than standard finger-prick testing. It results in fewer emergency room visits and hospitalizations. Diabetes organizations and patient communities have disseminated this message, emphasizing the benefits of CGM for insulin-treated and non-insulin-treated patients alike.

Large medical societies now recommend CGMs in their treatment guidelines. Meanwhile, individuals desire more intelligent health technology—devices that monitor how exercise, food, and daily routines influence their sugar levels from afar. The scope of the epidemic compels healthcare systems to find scalable solutions. CGMs cut long-term expenditures by avoiding costly complications and are therefore crucial for stretched public health budgets. Increased media attention and support groups in the community dispel the mystery surrounding the technology, leading to further acceptance by those outside of the tech community. Employers now incorporate CGMs into health programs due to their ability to ensure productive workforces. This combination of medical evidence, professional acceptance, and patient pressure continues to grow the CGM market consistently.

Advances in sensor technology, battery longevity, and wireless technology have made CGMs go from clunky devices to slim, easy-to-use devices. New sensors can last weeks or months without a finger-stick check, thanks to calibration at the factory. Bluetooth and other wireless connections beam real-time glucose information directly into phones or apps, allowing remote physician visits and automated insulin pumps. Open-format tech standards let different brands of pumps, sensors, and software work together smoothly. Smart algorithms now predict sugar spikes or drops hours early, sending alerts to prevent emergencies. Meanwhile, over-the-counter CGMs sold without prescriptions—like those for general wellness or fitness tracking—have opened the market to new users beyond traditional diabetes patients.

Integration with smartwatches and fitness trackers creates unified health dashboards. Cloud platforms enable remote monitoring of at-risk patients by caregivers. Subscription plans ship sensors discreetly to residences, enhancing adherence. Pharmacies provide onboarding assistance, making the learning process simpler for seniors. Such ecosystems transform raw data into useful insights through customized feedback loops. Advances in battery life enable smaller, water-resistant designs supporting active lifestyles. As CGMs converge with nutrition apps, digital coaching, and pharmacy services, companies that provide these integrated health ecosystems benefit the most. This technology revolution isn’t as much about improved devices as it is about integrating CGMs into daily health management without compromise.

Though well-documented benefits to health, the adoption of CGMs is severely hampered by high financial hurdles. Starter kits entail high initial costs, while repeated sensor replacement creates repeat expenses that overtax family budgets. Insurance coverage is uneven around the world: whereas some policies cover CGMs for insulin-dependent individuals, type 2 diabetics who do not take insulin receive limited or no reimbursement. In many countries, public healthcare systems do not have specific funding channels for these devices, so clinics and patients receive partial or zero coverage. Out-of-pocket expenses impose hard decisions—families tend to extend sensor use beyond recommended durations or forgo monitoring entirely, sacrificing diabetes control. This access gap most heavily affects fixed-income elderly and disadvantaged populations.

Manufacturers have yet to provide genuinely low-cost sensor alternatives that can increase accessibility. With no coherent reimbursement policies that account for CGM’s long-term cost savings by avoiding emergencies and hospitalizations, and with no industry innovation towards hardware affordability, these financial barriers will continue to hold back real-world adoption. Unless payers, providers, and device manufacturers get on the same page for sustainable funding models, life-changing glucose monitoring will elude millions who would benefit most. The potential of the technology is clear, but its potential must be realized in spite of these economic realities by means of cooperative solutions and innovative pricing strategies.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Real-Time CGM (rtCGM) Intermittently Scanned CGM (isCGM) Implantable CGM Non-Invasive CGM

|

| By Application |

Type 1 Diabetes Type 2 Diabetes Gestational Diabetes Mellitus Prediabetes & Wellness Pediatric Diabetes

|

| By End User |

Home Healthcare Hospitals & Clinics Specialty Diabetes Centers Digital Health & Wellness Clinical Research Organizations

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Continuous Blood Glucose Monitoring market is divided by sensor modality and data delivery. Real-Time CGM (rtCGM) systems offer continuous glucose data at 1–5 minute intervals with hypo-/hyperglycemia alerts, which can be tailored; these are ideal for high-risk patients in need of tight glycemic management. Intermittently Scanned CGM (isCGM)—also referred to as flash glucose monitoring—provides on-demand glucose levels upon user scanning of the sensor with a reader or smartphone; with less complex calibration and reduced sensor expense, isCGM is appropriate for users with lower risk of hypoglycemia.

Implantable CGM sensors, implanted subcutaneously with multi-month durations, provide extended-wear but require minor procedures for insertion and removal. Prototypes in development that do not involve invasive procedures utilize optical or transdermal approaches to estimate glucose without subcutaneous insertion; promising for user comfort enhancement, they are at present confronted with accuracy and regulatory approval challenges. Systems also vary by connectivity—Bluetooth, NFC and proprietary RF protocols—and by integration capability with insulin pumps, mobile apps and cloud-based analytics. As interoperability standards emerge, there is a growing need for integrated platforms that support data sharing between multiple devices and clinical systems.

CGM applications cover Type 1 Diabetes, Type 2 Diabetes, and Gestational Diabetes Mellitus (GDM). Type 1 Diabetes patients, usually employing intensive insulin regimens or closed-loop pumps, experience the most glycemic benefit from rtCGM, minimizing hypoglycemia and enhancing time-in-range measures. Type 2 Diabetes patients, both insulin- and non-insulin-treated, increasingly embrace isCGM for remote care and lifestyle changes as evidence continues to build for CGM’s ability to maximize oral and injectable therapies. GDM screening and management utilize CGM to track glucose excursions in pregnancy, optimizing maternal and fetal outcome as well as reinforcing nutritional counseling.

New applications encompass prediabetes management—where short-term CGM assists in determining the effect of diet and exercise intervention—and sports and wellness, where over-the-counter CGMs guide metabolic wellness optimization in athletes and health-oriented consumers. Pediatric uses overcome special challenges in preschool children, including limiting finger-sticks and enabling remote parental monitoring. Across every application, clinical trials highlight CGM’s potential to lower HbA1c as much as 1 percent, lower severe hypoglycemia events by more than 40 percent and enhance patient-reported outcomes.

The CGM market addresses Home Healthcare, Hospitals & Clinics, and Specialty Diabetes Centers, with a growing Digital Health & Wellness subsegment. Home Healthcare leads the way with patients monitoring themselves through wearable sensors and smartphone apps; pharmacy-dispensing models and telemedicine platforms enable direct-to-consumer sales and remote management of type 1 and type 2 diabetics. Hospitals & Clinics apply CGMs in the inpatient environment—especially endocrinology units and intensive care units—to manage critically ill patients with diabetes and perioperative glucose management, using real-time data to inform protocolized interventions.

Specialty Diabetes Clinics and Diabetes Education Programs incorporate CGM data into multidisciplinary care plans, providing formal training, dietician assistance and pump-to-CGM commissioning services. Digital Health & Wellness end-users are fitness enthusiasts, athletes and wellness-oriented preventive health consumers embracing OTC CGMs for metabolic information, leading partnerships with fitness trackers and nutrition applications. In addition, Clinical Research Organizations (CROs) use CGMs in drug trials to measure glycemic impacts of new therapeutics, and Employer Health Programs and Payers investigate CGM coverage for high-risk groups to minimize long-term complications.

North America accounted for more than 38 percent of world CGM revenues in 2024, fueled by high incidence of diabetes, sophisticated reimbursement practices and robust clinician uptake. The U.S. Centers for Medicare & Medicaid Services broadened type 2 diabetic coverage criteria in 2023, while private payers increasingly reimburse isCGM under wellness programs. Provincial health plans in Canada cover rtCGM for type 1 patients, further strengthening market maturity.

Europe held around 28 percent of market share in 2024, with Germany, the U.K. and France as the leading countries. Social insurance funds and national health services cover CGMs for insulin users, but the coverage for non-insulin users is not uniform. Harmonization under the European Medical Device Regulation (MDR) simplifies approvals, and multi-country registries for diabetes facilitate real-world evidence generation.

Asia-Pacific is the region with the highest growth, with more than 10 percent CAGR led by China, Japan, India and Australia. Public policy—e.g., China’s Diabetes Prevention and Control Plan—supports CGM adoption into chronic disease management. Increased disposable incomes, growth of private payers and telehealth use drive home-use CGM adoption, while local manufacturing collaborations reduce sensor prices.

Latin America, the Middle East & Africa combined account for approximately 14 percent of worldwide CGM sales. South Africa and Brazil are at the forefront of regional adoption through public-private screening initiatives, while other regions are still in their infancy. Financial limitations and sparse reimbursement schemes hold back wider adoption, which has driven manufacturers to use tiered pricing, reagent-rental schemes and charitable programs to establish early demand.

The global continuous blood glucose monitoring market was valued at USD 5.8 billion in 2024.

The continuous blood glucose monitoring market is projected to grow at a CAGR of 8.6% from 2025 to 2033.

The Real-Time CGM (rtCGM) hold the largest continuous blood glucose monitoring market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Dexcom, Inc., Abbott Laboratories, Medtronic plc, Senseonics Holdings, Inc., Roche Diagnostics, Genteel LLC

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Continuous Blood Glucose Monitoring Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Continuous Blood Glucose Monitoring Market, By Application

5.3 Continuous Blood Glucose Monitoring Market, By End User

6.1 Continuous Blood Glucose Monitoring Market, By Country Type

6.1.1 Continuous Blood Glucose Monitoring Market, By Technology

6.1.2 Continuous Blood Glucose Monitoring Market, By Application

6.1.3 Continuous Blood Glucose Monitoring Market, By End User

6.2 U.S.

6.2.1 Continuous Blood Glucose Monitoring Market, By Technology

6.2.2 Continuous Blood Glucose Monitoring Market, By Application

6.2.3 Continuous Blood Glucose Monitoring Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping