Craniomaxillofacial Devices Market

Craniomaxillofacial Devices Market Share and Trend Analysis, By Technology (Plate and Screw Fixation Systems, Bone Graft Substitutes, Temporomandibular Joint (TMJ) Replacement Systems, Distraction Systems, Cranial Flap and Thoracic Fixation Systems), By Application (Trauma Reconstruction Surgery, Neurosurgery and ENT, Orthognathic and Dental Surgery, Plastic and Cosmetic Surgery), By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

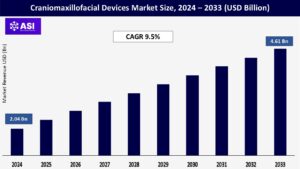

CAGR: 9.5%

Last Updated : February 25, 2026

The global Craniomaxillofacial Devices Market was valued at USD 2.04 billion in 2024 and is projected to reach USD 4.61 billion by 2033, expanding at a compound annual growth rate CAGR of 9.5% during the forecast period (2025 – 2033).

CMF devices are applied during jaw, facial, and skull surgeries. The devices employed include plates, screws, distraction systems, and TMJ implants. in each trauma, reconstructive, and cosmetic procedure. Demand for CMF devices increases owing to an increase in facial trauma, increased numbers of cosmetic surgery procedures, and advancements in implant technology and surgery technology. As healthcare infrastructure increases worldwide, particularly in the developing world, more access to surgical procedures and advanced medical devices increases.

Advances in bioabsorbable implants and patient-specific 3D-printed devices have transformed surgery to provide enhanced clinical outcomes and reduced complications. In addition, computer technology employed in surgery is making operations more precise and less time-consuming. As the population of the aged increases and patients ask for aesthetically desirable as well as functional outcomes, the market must grow aggressively. Advances in biomaterials, strong R&D pipelines, and increases in minimally invasive procedures are shaping the future of the industry, solidifying the place of CMF devices in contemporary medicine.

Increased incidence of facial trauma and congenital deformities is one of the prominent drivers of growth in the craniomaxillofacial devices market. An increase in road traffic accidents, physical violence, and injuries associated with sports has increased the demand for prompt and effective craniofacial surgery. Road traffic accidents are one of the leading causes of injury worldwide and most of these take place in low- and middle-income nations, as stated by the World Health Organization. Road traffic accidents tend to result in multi-fragmentary fractures of facial bones that can frequently be managed surgically. There is also growing incidence of congenital conditions like cleft lip and palate, craniosynostosis, and Treacher Collins syndrome that is driving demand for surgery.

Growth of pediatric and neonatal surgical centers has enhanced early diagnosis and remediation of such deformities. In addition, the aging population is also vulnerable to falls due to accidents, which would most likely result in facial fracture that would require reconstruction. Such a population change would also enhance the application of CMF devices to rebuild form and function. Hospitals and trauma centers are also investing in sophisticated surgical equipment and training to conduct such surgeries. Public health education, government policies, and greater access to healthcare facilities are also contributing to earlier treatment and diagnosis and thus increasing demand for craniomaxillofacial surgical devices across the globe.

Technology advancements have revolutionized the craniomaxillofacial devices market with improved patient outcomes and surgical success. Among the most significant developments is the use of 3D printing technology, which facilitates the use of patient-specific implants developed from the anatomy of the patient. Personalized implants provide a better fit, reduced complications, and recovery rates. Another quantum leap is the development of bioabsorbable materials. These materials render secondary surgery unnecessary for explantation of the implant and hence are appropriate for children and those with low surgical risk.

Also, titanium and polyetheretherketone (PEEK) materials provide higher biocompatibility and strength, enabling stable, long-term implant solutions. Computer-aided design (CAD), surgical navigation systems, and robotics are increasingly precise procedures, shortening surgery time, and general safety. Intraoperative guidance and preoperative planning integration with AI is also being studied. The technologies are driven by partnerships between med-tech firms and university research institutes and clinical trials. Demand is also driven by growing interest in minimally invasive surgery, fueled by ever more powerful and miniaturized devices. All such technology trends collectively help to revolutionize craniomaxillofacial surgery, widening the potential market base and encouraging market growth.

All the latest technological advantages of craniomaxillofacial devices are pre-empted by the totally astronomical expense, a primary block to extensive use. The implants are typically fabricated from the latest materials like titanium alloys, bioresorbable polymers, and biocompatible composites that necessitate precision-fabrication and regulatory affairs at additional cost, which translates into higher-cost production. In addition, the technique methods themselves are sophisticated and require advanced facilities, qualified personnel, and higher-level procedure centers. The sum of hospitalization, anesthetization, post-surgical treatment, and follow-up is prohibitively expensive for the uninsured patients, rendering such interventions unaffordable.

This is particularly concerning in low- and middle-income economies where there is reduced spending on healthcare per head and where reimbursement systems are underdeveloped or non-existent. Both government and private insurance plans don’t cover reconstructive or cosmetic facial surgery, and the full expense is on patients. Apart from this, unawareness of patients regarding the potential availability of surgical treatment and apprehension of undergoing surgery prevents or avoids timely treatment. Unavailability of an equal number of trained maxillofacial surgeons further fuels the demand-supply gap. These issues can be addressed by coordinating the action of device companies, governments, and payers in a manner that advanced CMF solutions are not only cost-effective but accessible to more patients globally.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Plate and Screw Fixation Systems Bone Graft Substitutes Temporomandibular Joint (TMJ) Replacement Systems Distraction Systems Cranial Flap and Thoracic Fixation Systems

|

| By Application |

Trauma Reconstruction Surgery Neurosurgery and ENT Orthognathic and Dental Surgery Plastic and Cosmetic Surgery

|

| By End User |

Hospitals Ambulatory Surgical Centers (ASCs) Specialty Clinics

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Craniomaxillofacial devices market is segmented based on technology as follows: plate and screw fixation systems, bone graft substitutes, TMJ replacement systems, distraction systems, and cranial flap and thoracic fixation systems. Plate and screw fixation devices enjoy the highest volume by percentage since they are used extensively for trauma, reconstructive, and orthognathic surgery. Implants are normally composed of titanium or bioresorbable material, provide rigid stable fixation, and are best suited in terms of modularity and compatibility with radiography. Bone graft substitutes are used in instances of intrinsic bone deficiency, and they find most common use in trauma, tumor resection, or congenital defect reconstruction.

They are demineralized matrices, allografts, and synthetic ceramic biomaterials whose function is the stimulation of osteogenesis. TMJ replacement systems treat jaw disorders ankylosis and arthritis through anatomical and functional reconstruction through the use of CAD-fabricated, custom-designed implants. Distraction osteogenesis systems treat congenital facial deformities through controlled lengthening of bone, frequently applied in the pediatric patient. Finally, cranial flap fixation systems are neurosurgical for the fixation of bone following craniotomy, and thoracic fixation systems are reconstructive in nature within the thoracic cavity. Typically, these technologies are cosmetic as well as functional surgical requirements, with technological advancement concentrated on better materials, precision in design, patient comfort, and minimizing revision surgery.

Craniomaxillofacial devices are applied in trauma reconstruction, neurosurgery and ENT, orthognathic and dental surgery, and plastic and cosmetic surgery. The demand for trauma reconstruction is greatest because facial trauma due to road accidents, falls, and violence is extremely prevalent. The patients must be treated promptly and successfully by accessible fixation appliances and implants to achieve facial anatomy and function. CMF devices play a very crucial part in neurosurgery and ENT for the management of cranial base neoplasms, skull defects, and compound infection. Their precision and stability are of utmost priority for successful operation in sensitive brain and facial nerve fields.

CMF devices are utilized in dental and orthognathic procedures for the adjustment of jaw malalignments, malocclusions, and various other maxillofacial deformities. Increased demand for cosmetically enhanced smiles and functional rearrangements of the jaw is driving this segment. Cosmetic and plastic surgery simultaneously has experienced increased acceptance of CMF devices for chin, jaw, and cheek augmentations. With advances in technology, natural contours are feasible without extended scarring and healing and thus are perfectly suited to cosmetic augmentation. With an escalating degree of surgical competence and a need for patients, these applications increasingly overlap and expand, requiring devices that provide structural integrity and cosmetic precision. Together, these markets represent the need for widespread clinical use of CMF products in contemporary medicine.

Ambulatory surgical centers (ASCs), specialty clinics, and hospitals are three general end users of the craniomaxillofacial devices market. Hospitals have the greatest market share through shared infrastructure, multidisciplinary surgical teams and backup for managing emergency as well as complicated reconstructive cases. With their imaging capabilities and operating room services, hospitals are the site of attack for trauma treatment and management of congenitally deformed craniofacial disorders. ASCs, however, are emerging center-stage players with their cost-effective operations, reduced patient turnover, and applicability towards elective or limited procedures. With healthcare moving to outpatient centers, there is increasing usage of CMF devices in such centers for routine orthognathic, dental, and cosmetic surgeries.

Cosmetic facial surgery and targeted corrections are performed quite widely in specialty clinics, emphasizing treatment tailoring with the use of advanced surgery planning equipment and 3D imaging. The clinics encounter a patient population seeking individually tailored, typically elective procedures emphasizing appearance to an equal extent as functionality. Growing medical tourism and familiarity with facial-enhancing procedures are driving this segment’s growth. As healthcare delivery patterns change, all three end consumers—hospitals for urgency, ASCs for convenience, and clinics for personalization—are synergistic in establishing future demand for craniomaxillofacial devices.

North America leads the market of craniomaxillofacial devices because it has a most advanced healthcare system, strict reimbursement systems, and highest facial trauma cases. The United States holds the maximum regional market share due to excellent investments in R&D, extensive use of advanced surgical technology, and the availability of world-leading medical device companies. Increased demand for cosmetic as well as reconstructive procedures also leads to the growth of the market. Germany, driven by highly trained surgeons, patient-friendly attitudes, and well-established trauma care networks, is also contributing to the region’s domination. Canada is also adding market growth with its increasing investment in healthcare and increasing emphasis on craniofacial procedures.

Europe dominates the craniomaxillofacial devices market, with the United Kingdom, France, and Germany being at the forefront of technology adoption and surgical experience. The region boasts a well-established healthcare infrastructure, mature patient population, and increasing demand for aesthetic and reconstructive treatments. Increased emphasis on craniofacial trauma care and increased awareness towards congenital defect repair lead to constant market expansion. Regulatory stringency in Europe guarantees product quality and safety, and reliance on CMF products. Constant investment in maxillofacial surgical training, research and development activities, and availability of maxillofacial specialist centers position Europe as the leader in CMF technology advancements.

Asia-Pacific is also experiencing maximum growth in the craniomaxillofacial devices market because of growth in road accidents, growth in healthcare expenditure, and rising demand for reconstructive operations. China, India, and Japan are the most critical drivers facilitated by greater surgical training programs and better infrastructure in hospitals. Rising numbers of the middle class and concern for facial trauma restoration are driving demand for CMF procedures. In addition to this, there has been government spending on creating state-of-the-art public health networks. Government spending is directed towards trauma and plastic surgery centers. Increased medical tourism in Thailand and South Korea also gives Asia-Pacific region market growth impetus.

LAMEA craniomaxillofacial devices market is being fueled by modest but encouraging growth due to constant development in healthcare accessibility and infrastructural facilities. India, China, and Vietnam will emerge as regional CMF procedure hubs in terms of increased demand for aesthetic procedures and trauma conditions. Reimbursement mechanisms limited in scope, economic inequalities, and absence of even rural access, however, are inhibiting wide-scale adoption. Even so, growing medical tourism, urbanization, and expanding public expenditures are expected to propel market expansion. Training initiatives and strategic alliances can continue to support growth activities in the new markets.

The global Craniomaxillofacial Devices Market was valued at USD 2.04 billion in 2024.

The market is projected to grow at a CAGR of 9.5 % from 2025 to 2033.

Trauma Reconstruction Surgery hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Stryker, Johnson & Johnson (DePuy Synthes), Medtronic, Zimmer Biomet, KLS Martin, B. Braun, OsteoMed, Integra LifeSciences, Acumed, and Medartis.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Craniomaxillofacial Devices Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Craniomaxillofacial Devices Market, By Application

5.3 Craniomaxillofacial Devices Market, By End User

6.1 North America Craniomaxillofacial Devices Market, By Country Type

6.1.1 Craniomaxillofacial Devices Market, By Technology

6.1.2 Craniomaxillofacial Devices Market, By Application

6.1.3 Craniomaxillofacial Devices Market, By End User

6.2 U.S.

6.2.1 Craniomaxillofacial Devices Market, By Technology

6.2.2 Craniomaxillofacial Devices Market, By Application

6.2.3 Craniomaxillofacial Devices Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping