Active Wheelchair Market

Active Wheelchair Market By Application (Daily Mobility, Sports & Recreation, Rehabilitation) By Distribution Channel (Online Retailers, Medical Supply Stores, Hospitals & Clinics) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

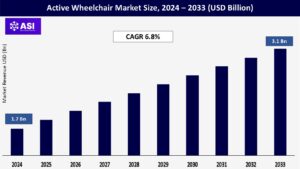

CAGR: 6.8%

Last Updated : February 25, 2026

The global Active Wheelchair Market was valued at approximately USD 1.7 billion in 2024 and is projected to reach USD 3.1 billion by 2033, growing at a CAGR of 6.8% during the forecast period (2025–2033).

Active wheelchairs are lightweight and ergonomically-designed mobility devices that allow users to independently manage their own movement, even in day-to-day life or sports situations. These wheelchairs are designed for users with permanent or longer-term mobility impairments, and have improved performance, durability and customizability. Active wheelchairs typically consist of rigid or foldable styles, utilized to provide strength and agility, created with materials such as aluminum, titanium, or carbon fiber. Smart controls, ergonomic seating, and shock-absorptive characteristics are increasingly incorporated into newer models to facilitate active lifestyles.

The market has exhibited growth due to increased incidence of spinal cord injuries and neuromuscular disorders, the independence to move freely throughout the different environments, and increased demand for sports participation through the para-sports. A part of the change in the market is from technological innovation as well as an improvement in reimbursement for the provision of assistive devices, particularly in regard to markets with developing economies and mature economies.

Both the recent worldwide increase in a variety of “mobility restricted” conditions, particularly spinal cord injury (SCI), multiple sclerosis, muscular dystrophy, and cerebral palsy, has led to the growth of the active wheelchair market. According to the World Health Organization (WHO), up to 500,000 people experience spinal cord injuries yearly, primarily due to preventable causes (road traffic crashes, falls, and violence).

These conditions heavily affect someone’s mobility, and thus, their autonomy; thus, users either use an active wheelchair or will eventually and eventually have to transition to something more suitable. A successful active wheelchair will be lightweight, support and offer customization to the user, and offer a propulsive ability for everyday use. As Research from other sectors such as consumer products identifies new trends, its also being seen in mobility aids when looking at the active wheelchair.

In April 2024, Invacare Corporation, announced a significant upgrade to its Küschall line of active wheelchairs, which showcases an improved biomechanical position for active wheelchair users, according to their own strengths and abilities, ultimately proving the trend of advanced functional needs for mobility aids. Similarly, Sunrise Medical announced, and upgraded its Quickie Nitrum, for active wheelchair users, specifically to address users, who may have some level of athleticism, or those have a more active lifestyle and mobility range.

The rising trend of adaptive sports and awareness of inclusiveness and sporting opportunity for persons with disabilities is substantially increasing the need for performance-based active wheelchairs. Events such as the Paralympic Games, regional disability sports championship events, and recreational sporting activities are motivating wheelchair users to live ferociously active lifestyles.

Hence, there is substantial demand for lightweight, sport specific, and ergonomically designed wheelchairs. For example, in 2023, RGK Wheelchairs (UK) produced a brand new range of made to measure sports wheelchairs to suit basketball and racing athletes.

And in 2024, Top End (a brand within Invacare) launched the Top End Pro Tennis and Racer series to which they intended to offer improved frame flexures and adjusted user comfort whilst meeting the specific performance requirements for para-athletes. Both RGK and Top End enjoyed good market opportunities and the innovation made a real step forward towards advanced mobility.

One of the main obstacles in the active wheelchair market is the high cost associated with models that contain technology. Active wheelchairs can range anywhere from USD 3,000 to even more than USD 10,000 per unit. This limits supply and demand at the consumer level across a large segment of the possible market – especially in LMIC’s where public reimbursement is limited or non-existent.

According to World Bank Development Report – over 50% of the world’s population lack necessary access to essential health services including assistive mobility devices. Even in the developed world, insurance and other sources of reimbursement often do not subsidize either advanced or sport-specific wheelchairs, effectively forcing many consumers to settle for low-cost, low-tech and basic mechanisms that ultimately do not fit their lifestyle or performance needs. The costs of maintenance, customizations and upgrades also significantly impact long-term ownership, potentially limiting the number of potential users interested in investing in high/advanced performance mobility solutions.

The Active Wheelchair Market is segmented by application and distribution channel, each playing a key role in addressing the diverse mobility and lifestyle needs of users across healthcare, recreational, and residential settings.

In 2024, Daily Mobility held the most considerable value of the market, accounting for approximately 52.4% of overall revenue. The Daily Mobility segment features active wheelchairs for normal personal mobility—for example, commuting, household chores, work, or school (usually funded privately). This area has significant demand from individuals with spinal cord injury, amputation, or degenerative conditions needing durable, ergonomic, and self-propelling mobility devices.

Brands such as Sunrise Medical (Quickie) and Invacare dominate this area with lightweight, tailored designs purposely focused on posture, portability, and aesthetics. Alternatively, Sports & Recreation is the fastest-growing application segment fueled by the recent growth in participation surrounding adaptive sports and para-athletics. This category of wheelchair is for activities such as basketball, tennis, racing, and rugby, all of which offer very highly specialized frames for agility and impact resistance.

With the success of globally branded events such as the Paralympic Games and regional funding supporting the initiatives of inclusive sport, the demand for adaptive sports wheelchair products is likely to sustain investment, innovation, and co-development. Companies like RGK, Top End, and Melrose are introducing custom-fit, competition-ready models to meet this increasing need. Rehabilitation applications also represent a major need, especially in a clinical and physiotherapy context, with wheelchairs being prescribed most often after injury, surgery, or after a lengthy recovery from a neurological condition.

This segment is supported by hospitals, rehabilitation facilities, and outpatient clinics. Growth trends are also bolstered by increasing investments in rehabilitative care infrastructure, as well as growing implementation of active mobility devices in post-acute care. Products in this segment emphasize postural alignment, adjustment of support, and ability to maneuver seamlessly while in therapy.

The Offline Medical Supply Store will remain the leading distribution channel with 48.6% of the global market share in 2024. Offline Medical Supply Stores offer the hands-on help needed in fitting, customizing, and servicing items that are even more critical for an active wheelchair user. Medical professionals usually collaborate with the retailer when prescribing and fitting items, and the local dealers and distributors provide essential after-sales support for the respective ways regional markets develop, especially in both North America and Europe, who possess resellers.

Online Retailers are witnessing rapid growth fueled by an increase in both digital penetration and consumers’ shifting preferences to a sharable and hassle-free shopping experience. Online retailing provides a very wide range of product choices from e-commerce sites like Amazon to digital platforms from Health Products For You (HPFY) and to direct consumer channels offered from manufacturers like WHILL, Invacare, and Ki Mobility with product virtual customization.

Rural or under-served areas can benefit through this channel, while online platforms provide further comparative advantages to identify the best fit that may not provide fitting benefits. Hospitals & Clinics also play an important distribution role, especially as part of recovery from injury or for chronic illnesses. Many users receive their first active wheelchair while in hospital or a rehabilitation setting, often with full or partial reimbursement through insurance. Clinical distribution is most effective in countries with universal coverage, or where there is a disability insurance program in place, like Germany, the UK, Canada, and Japan.

In 2024, North America had the highest market share of around 38.7% due to a sophisticated healthcare system and the level of adaptation of assistive technology, with businesses such as Permobil, Sunrise Medical and Invacare Corporation leading this market.

The United States topples this entire region’s market share not only for having a public reimbursement system and other private insurance that have positive compasses for active wheelchairs but also for the sheer amount of spinal cord injury cases, or an estimated 17,000 new cases per year in the United States according to the National Spinal Cord Injury Statistical Center, that speaks to an ongoing demand for active wheelchairs. Equally, the developments in para-sports and opportunities to access services catering to rehabilitation also help the region grow.

The second largest regional market, Europe, is expected to account for approximately 29.4% of global revenue in 2024. Germany, the United Kingdom, France and the Netherlands lead the region due to strong public healthcare systems and proactive engagement towards disability inclusion.

The European Union supports mobility equipment with options from national insurance schemes and through accessibility legislation, such as the European Accessibility Act. Community awareness of independent living, along with the growing trend of custom and sports wheelchairs are increasing demand. Increased demand is further supported by a rapidly aging population in Europe, with over 21% of the population over the age of 65—the unprecedented opportunity for active wheelchairs for senior users.

The Asia-Pacific area is expected to grow the fastest during the period of forecast, with a CAGR over just 8.5% from 2025 to 2033, which will be fueled by increased disability awareness, higher healthcare spending and a growing middle class wanting to improve their quality of life and possibly their own mobility in their life experiences.

Concerning the current leading markets in the near future for the region – Japan will no doubt come out at the top (in terms of age demographics), and China in terms of government-backed initiatives, particularly the “Rehabilitation Aids Industry Development Plan” (Rehabilitation Aids Industry Development Plan, 2021).

In India and Southeast Asia, the market will still remain under-served, but will start to build traction because more NGOs have begun to support programs aimed at disability awareness, and additionally assistive tech start-ups will have started to produce low-cost active wheelchair models or technologies. The Asia-Pacific region has considerable potential through local manufacturing, technology uptake, improvement of public or private sector disability insurance programs.

Latin America has the smallest market share but is starting to emerge thanks to Brazil, Mexico and Argentina. The rise in disability prevalence, improved awareness of assistive technologies and healthcare access have opened the door for further market growth.

Government led programs and initiatives from NGOs encouraging disability inclusion are boosting the accessibility of active wheelchairs. However, issues like the insufficient public funding that is available, inconsistent infrastructure, and reliance on imported products are hindering growth as these such issues, and the high costs affect the size of the market.

The smallest share of the global market in 2024 is MEA, although it is making slow progress. Countries in the Gulf, e.g., UAE and Saudi Arabia are investing in the modernization of healthcare and disability inclusion programs, boosting demand for high-performance mobility solutions.

In contrast, sub Saharan Africa has significant challenges, such as lack of access, costs and poor and unorganized healthcare infrastructure. However, through international organization support, and new low cost, durable wheelchair projects, e.g., South Africa and Kenya, modest growth is likely over time.

The market was valued at USD 1.7 billion in 2024.

The market is projected to grow at a CAGR of 6.8% from 2025 to 2033.

The Manual Active Wheelchairs hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Permobil, Sunrise Medical, Invacare Corporation

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Active Wheelchair Market, By Application

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Active Wheelchair Market, By Distribution Channel

6.1 North America Active Wheelchair Market, By Country

6.1.1 Active Wheelchair Market, By Application

6.1.2 Active Wheelchair Market, By Distribution Channel

6.2 U.S.

6.2.1 Active Wheelchair Market, By Application

6.2.2 Active Wheelchair Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping