Aortic Valve Replacement Market

Aortic Valve Replacement Market Share & Trends Analysis Report, By Product Type (Transcatheter Aortic Valve Replacement (TAVR), Sutureless Aortic Valve Replacement, Others) By End User (Hospitals, Ambulatory Surgical Centers, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

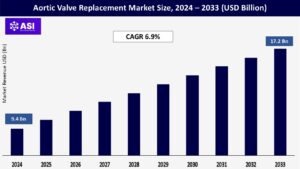

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.9%

Last Updated : February 25, 2026

The global Aortic Valve Replacement Market was valued at approximately USD 9.4 billion in 2024 and is projected to reach USD 17.2 billion by 2033, growing at a CAGR of 6.9% during the forecast period (2025–2033).

Aortic valve replacement consists of a woman with a damaged aortic valve substituted surgically with a prosthetic valve to restore the ability for normal blood flow to the body. The aortic valve replacement usually occurs when there is aortic stenosis or aortic regurgitation. The types of procedures include transcatheter aortic valve replacement (TAVR), open heart surgery, and sutureless.

Provide the horizon TAVR is popular with surgeons because it is relatively low invasive and is more favorable with older older and higher risk patients. Not only is the aortic valve replacement market opportunity driven by the increase rates of valvular heart disease, and the older adult population, but also new prosthetic design and delivery of valve implantation. In developing countries it continues to grow due to the advancement of diagnostic capabilities, an increase in understanding and a greater push for access to cardiac care.

The worldwide rise of aortic stenosis, one of the most prevalent and serious forms of valvular heart disease, is an underlying driver of the aortic valve replacement market. Aortic stenosis affects mainly older adults and occurs from age-related calcifications of the aortic valve, reducing blood flow from the heart to the body. According to the American Heart Association, approximately 12.4% of individuals aged 75 and older have moderate to severe aortic stenosis.

Untreated aortic stenosis can lead to heart failure and sudden cardiac death, and the one-year mortality rate exceeds 50% in symptomatic untreated patients who do not undergo valve replacement. As awareness of aortic valve disorders rises, along with increased diagnostic screenings via echocardiography and cardiac CT, the number of patients being identified for surgical or transcatheter valve replacement interventions is also rising.

In addition, worldwide efforts to improve early diagnosis and treatment, particularly in very high-risk patients, are increasing physician and healthcare system-led interventions. For example, countries such as Japan, Germany, and the U.S. have expanded national screening program for heart disease. Targeting interventions early in disease will increase utilization of aortic valve replacement technology.

Innovations in technology for Transcatheter Aortic Valve Replacement (TAVR) procedures have completely altered the treatment path for aortic valve therapy and contributed substantially to overall market growth. TAVR was first developed for patients at high surgical risk, but now includes intermediate risk and even low-risk patients because it is less invasive, quicker recovery, and very positive outcomes.

New-generation TAVR systems provide new features that will offer patients greater valve durability, greater precision for valve placement, and lower rates of paravalvular leak and stroke. For example, Edwards Lifesciences received CE mark for their new SAPIEN X4 valve system in February 2024 that incorporates the latest sealing technology, and utilizes smart delivery systems for greater procedural success. Alternatively, Medtronic’s Evolut FX TAVR platform, released to market in early 2023, introduces a lower-profile delivery system with better control and visibility during implantation.

Additionally, government regulatory bodies such as the U.S. Food and Drug Administration (FDA) and European Medicines Agency (EMA) have allowed for extended indications for TAVR, enabling younger and healthier patients to replace their valves without open-heart surgery. The introduction of new patient populations, coupled with additional physician adoption and training, is helping to be a driver for global TAVR technology growth.

One of the main restraints that limits the widespread adoption of aortic valve replacement, especially the development of transcatheter aortic valve replacement (TAVR), is the expensive costs associated with the devices themselves and the actual procedure costs. The cost of a single TAVR can be $40,000 to $70,000 USD in countries such as the United States, depending on the valve type, the hospital costs and logistical details of the patients complexity. These costs are higher than the cost of surgical aortic valve replacement (SAVR) in many applications. Although reimbursement coverage has been improving in developed countries, costs remain a very significant issue in low- and medium income countries – with much of the healthcare expenditure taking form as out of pocket costs.

In public healthcare systems, access to TAVR is more often restricted depending on budgetary limits, wait times for access, and ability to treat higher risk patients first. It should also be noted that more fresh generation valve systems with added features such as repositionability, sealing skirts and imaging guidance come at a premium – and there are also plenty of more traditional valves at lower costs that may not be desired or feasible for underfunded hospitals or clinics. The financial consideration is even more critical in rapidly aging regions like Asia Pacific and Latin America, where demand is increasing for replacement but the resources and infrastructures to support them, is lagging.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Transcatheter Aortic Valve Replacement (TAVR) Sutureless Aortic Valve Replacement Others

|

| By End User |

Hospitals Ambulatory Surgical Centers Others

|

| Key Players |

Edwards Lifesciences Corporation Medtronic plc Abbott Laboratories Boston Scientific Corporation LivaNova PLC CryoLife, Inc. MicroPort Scientific Corporation Shanghai MicroPort Medical (Group) Co., Ltd. Venus Medtech (Hangzhou) Inc. JenaValve Technology, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Aortic Valve Replacement Market is segmented by product type and end-user. Each segment plays a critical role in advancing patient outcomes in the management of aortic valve diseases.

In 2024, Transcatheter Aortic Valve Replacement (TAVR) will be the leading product on the market with a market share of 56.8% due to its minimally invasive procedure, shorter hospital stay, and less risk involved in undergoing the medical procedure. TAVR is currently the first choice of treatment for elderly patients as well as for those who have been classified as inoperable or high risk. Even with expanding indications, TAVR continues to have significant adoption among patients referred for TAVR, including intermediate- and low-risk patients, globally. The continued refinement of next-generation valves with greater durability and repositionability will also drive demand.

Sutureless and Rapid Deployment Valves will have the fastest growth during the forecast period. These products generally shorten the cardiopulmonary bypass times and aortic cross-clamp times and are therefore well suited for minimally invasive procedures. They continue to grow in popularity in hybrid procedures and when there are some anatomical restraints associated with the procedure. Currently, Conventional Surgical Aortic Valve Replacement (SAVR), still has a large share of the market, especially for younger patients with better alternatives with mechanical valves that might last longer. The overall growth of this segment of the market will be slower than TAVR because, in both Emerging and Established Markets, TAVR is being increasingly favored.

The hospitals segment is the largest segment by end-user (61.2%) in 2024, with end-user differentiation across hospitals, ambulatory surgical center (ASC), and cardiac clinics/specialty center, largely due to hospitals being the only place to provide intensive cardiovascular services, which includes complex open-heart surgical procedures and transcatheter procedures.

There are large hospitals or ‘institutions’ where cardiac specialty facilities with level 1 or higher hybrid operating rooms are found. Hospitals have more interventional cardiologists than other end-user segments. As a result, both “surgeon” or “cardiologist” can deliver greater volume of surgical aortic valve replacement (SAVR) or transcatheter aortic valve replacement (TAVR) procedures.

However, ambulatory surgical centers (ASCs) are anticipated to drive significant growth in the market due to their increasing use of minimally invasive procedures (e.g., TAVR). ASCs will drive lower cost and shorter recovery course for patients and are a great alternative facility for patients to receive care in the appropriate context. As regulatory approvals for and payer support grows, the role of the ASC in valve replacement procedures will likely increase significantly. The cardiac clinics/specialty centers are growing the overall market as well, as urban markets analyze their prevention and patient referral and general clinic utilization.

These end-user facilities frequently conduct preoperative evaluation and should be connected to the hospital or surgical clinics to feedback patients for postoperative and delivered aortic valve replacement care. Additionally, we anticipate that cardiac clinics/specialty centers could play an interesting supporting role in our aortic valve replacement ecosystem.

At 38.5% market share in 2024, North America provides the largest contribution stemming from an advanced healthcare infrastructure, a high prevalence of valvular heart conditions, and significant adoption of new technologies such as TAVR. The United States dominates North America and is poised to do so in 2024 supported by a commercial insurance base with broad coverage options for the entire population and a robust framework of dedicated cardiac centers and favorable reimbursement policies. The elements of increased public awareness of aortic stenosis and an aging population all support this market’s growth.

Europe makes up a significant proportion of the market, with considerable adoption occurring in countries such as Germany, France, UK, and Italy. In 2023, approximately 120000 valve replacement procedures were completed in each of the major countries in Europe, demonstrating sustained demand. The aging population, increased government healthcare initiatives, and access to existing industry-leading medical device manufacturers supports continuous growth in the market. Additionally, emerging hospitals that are beginning to launch TAVR programs, including Sweden and the Netherlands, help expedite the industry shift toward minimally invasive valve therapy.

Asia-Pacific is projected to register the fastest CAGR of nearly 8.3% during the forecast period. The region is experiencing rapid urbanization, increased disposable incomes, and healthcare spending from governments and individuals in markets such as China, India, Japan, and South Korea. Growth drivers include the increase in healthcare infrastructure, growth in older populations, and increased awareness regarding valvular heart diseases. Emerging markets in APAC are realizing improved access to advanced diagnostic and cardiac therapies, such as transcatheter aortic valve replacement (TAVR), which had previously not been attainable.

Latin America and Middle East & Africa are exhibiting moderate growth due to higher healthcare investments in addition to increased emphasis on managing cardiovascular disease. Countries, such as Brazil, Mexico, Saudi Arabia, and South Africa, are expanding on cardiac care facilities while promoting frameworks around reimbursement for those services. However, the disparity between economic strata, ensuring access to advanced healthcare technologies, and a shortage of specialists remain challenges to market growth in these regions.

The market was valued at USD 9.4 billion in 2024.

The market is projected to grow at a CAGR of 6.9% from 2025 to 2033.

The Transcatheter Aortic Valve Replacement hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Edwards Lifesciences Corporation, Medtronic plc and Abbott Laboratories

1.1 Summary

1.2 Research methodology

2.1 Particulate Adjuvants

2.2 Aluminum-Based Adjuvants

2.3 Toll- Like Receptor Agonists

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Aortic Valve Replacement Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Aortic Valve Replacement Market, By End User

6.1 North America Aortic Valve Replacement Market, By Country

6.1.1 Aortic Valve Replacement Market, By Product Type

6.1.2 Aortic Valve Replacement Market, By End User

6.2 U.S

6.2.1 Aortic Valve Replacement Market, By Product Type

6.2.2 Aortic Valve Replacement Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping