Medical Screws and Plates Market

Medical Screws and Plates Market Share & Trends Analysis Report, By Product Type (Plates, Screws), By Material Type (Metallic Implants, Polymer Implants, Composite Materials, Others), By Application (Orthopedic Applications (Fracture Fixation), Dental / Maxillofacial Applications, Craniofacial Applications, Trauma, Reconstruction, Osteotomy, Arthrodesis, Others), By End-User (Hospitals & Clinics, Orthopedic Clinics, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Research & Academic Institutions). Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

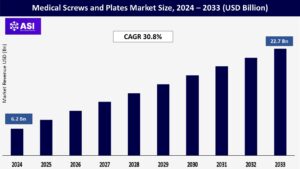

CAGR: 30.8%

Last Updated : December 25, 2025

The worldwide Medical Screws and Plates Market size was valued at approximately USD 6.2 billion in 2024 and is projected to reach USD 22.7 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 30.8% during the forecast period of 2025–2033.

The global orthopedic plates and screws market is witnessing strong momentum in 2024, fueled by a combination of demographic and technological factors. As the global population continues to age, the incidence of bone-related conditions such as fractures, osteoporosis, and degenerative joint diseases is rising sharply. This growing patient pool is driving increased demand for reliable and effective orthopedic solutions, with plates and screws playing a crucial role in both trauma care and elective orthopedic surgeries. At the same time, advancements in surgical techniques such as minimally invasive procedures and image-guided interventions are making orthopedic surgeries more precise, less invasive, and more accessible, further boosting the adoption of these devices.

The medical screws and plates market has become an integral part of modern orthopedic and trauma care, offering critical support for bone stabilization and recovery. With continuous innovations in implant materials, biomechanics, and custom-fit solutions, the market is poised for sustained growth well into the next decade. This evolving landscape presents significant opportunities for medical device manufacturers, healthcare providers, and investors alike.

One of the most powerful forces driving the global demand for medical screws and plates is the rapidly aging population. As people live longer, age-related conditions such as osteoporosis, arthritis, and other degenerative bone diseases are becoming increasingly common. These conditions significantly elevate the risk of fragility fractures, particularly in vulnerable areas like the hip, spine, and wrist, making surgical intervention and fixation devices essential for restoring mobility and quality of life in elderly patients.

Alongside this demographic shift, the world is also witnessing a steady increase in trauma cases, largely due to road accidents, falls, and workplace injuries. These incidents often result in complex fractures that require surgical treatment with plates and screws to stabilize and heal properly. In both urban and rural areas, the demand for effective orthopedic care is rising in tandem with these injury trends.Another major contributor is the growing popularity of sports and physical activities across age groups. Whether it’s high-impact competitive sports or recreational fitness routines, more people particularly in the younger and middle-aged demographics are engaging in active lifestyles. This has led to a notable uptick in sports-related injuries, many of which involve bone fractures or ligament damage that call for surgical repair using orthopedic implants.

Additionally, lifestyle-related health conditions like obesity and diabetes are playing a more subtle yet impactful role in driving demand. These chronic conditions often lead to musculoskeletal problems and joint degeneration over time, making patients more susceptible to orthopedic complications that require surgical intervention. Collectively, these interconnected trends are shaping a strong and sustained demand for medical screws and plates globally, making them a cornerstone of modern orthopedic care.

Technological advancements are playing a transformative role in reshaping the medical screws and plates market, greatly enhancing both implant performance and patient outcomes. A major area of progress lies in the development of improved biomaterials. Advanced titanium alloys, prized for their exceptional biocompatibility, strength, and corrosion resistance, are becoming increasingly dominant in surgical applications.

Stainless steel remains widely used due to its durability and cost-effectiveness, while bioabsorbable or biodegradable polymers are gaining traction, especially in cases where avoiding a second surgery for implant removal is critical offering both clinical and economic advantages. Alongside materials innovation, design and manufacturing technologies have evolved significantly. The advent of 3D printing has enabled the production of highly customized, patient-specific implants tailored precisely to an individual’s anatomy. This not only enhances surgical precision but also minimizes complications and recovery time, particularly in complex fracture cases. Similarly, anatomically contoured plates pre-shaped to fit specific bones, are becoming more common, as they help reduce operating time and provide more stable fixation. Innovations in locking plate technology, including variable-angle screw systems, are offering improved solutions for treating osteoporotic and multifragmentary fractures, enabling early mobilization and reducing implant failure.

Another key trend driving demand is the widespread adoption of minimally invasive surgical (MIS) techniques. These approaches require smaller incisions and cause less tissue trauma, leading to faster recoveries and shorter hospital stays. As a result, there’s growing demand for low-profile screws and plates specifically designed for MIS procedures. Further boosting the future outlook is the emergence of smart implants devices embedded with sensors and AI-driven features that can monitor healing in real-time, provide feedback to surgeons, and support more informed post-operative care. Complementing these innovations is the rise of robotic-assisted and computer-guided surgeries, which are redefining surgical precision. These technologies help surgeons place implants with greater accuracy, thereby reducing risks and improving long-term outcomes. Altogether, these breakthroughs are not only expanding the capabilities of orthopedic care but are also setting new standards for what is possible in trauma and reconstructive surgery.

One of the key challenges facing the medical screws and plates market is the high cost associated with advanced materials and cutting-edge technologies. Implants made from premium materials like titanium alloys, or those featuring sophisticated coatings and 3D-printed, patient-specific designs, are considerably more expensive than traditional options such as stainless steel. While these innovations offer undeniable clinical benefits, such as better biocompatibility, reduced complication rates, and improved outcomes, they also come with a steep price tag. This financial burden is typically absorbed by healthcare providers and, in many cases, passed on to patients or insurance systems, creating access barriers.

Moreover, the cost of an orthopedic implant is only one part of the financial equation. The entire surgical process, including the surgeon’s fees, anesthesia, hospitalization, and post-operative care, can be prohibitively expensive, particularly in regions where public healthcare support is limited or insurance coverage is inadequate. For many patients in low- and middle-income countries, these costs make surgical intervention either difficult to afford or entirely out of reach. Adding to the challenge are the budgetary constraints faced by hospitals and healthcare systems, especially in public institutions and in developing economies.

Limited funding can restrict their ability to adopt the most advanced implant technologies, forcing them to opt for more economical but potentially less optimal solutions. These financial limitations not only affect the accessibility of high-quality orthopedic care but can also contribute to disparities in treatment outcomes across different regions and healthcare settings.

One of the major hurdles facing the medical screws and plates market and the broader medical device industry is the lack of regulatory harmonization across global markets. Manufacturers often find themselves navigating a maze of region-specific approval processes, each with its own stringent requirements. While international efforts like the IMDRF (International Medical Device Regulators Forum) aim to align regulatory frameworks, significant differences remain between major markets such as the U.S. FDA, the EU’s MDR, and China’s NMPA. This fragmented landscape means companies must invest significant time and resources to gain separate approvals for each market, making global expansion slower and more expensive.

Adding to the challenge is the heightened level of regulatory scrutiny in recent years, particularly post-market. Authorities are demanding more robust clinical evidence, not just before a product hits the market, but long after it’s in use. The EU’s Medical Device Regulation (MDR), which became fully enforceable in May 2021, is a prime example. It has introduced much stricter rules around clinical data, traceability, and ongoing surveillance. While intended to improve patient safety, the MDR has created several practical challenges for manufacturers. For one, the limited number of Notified Bodies organizations responsible for certifying medical devices in the EU has created a bottleneck, leading to long delays in certification and recertification processes.

What once took several months can now stretch to over a year, putting pressure on launch timelines and operational planning. Additionally, the cost and complexity of complying with MDR have forced some manufacturers, especially smaller players, to discontinue certain products from the European market altogether. This not only limits patient access but can also lead to shortages of essential devices. Furthermore, these regulatory hurdles have an unintended consequence: they can slow down innovation. Companies often prioritize getting their existing devices recertified under stricter rules, leaving less time, budget, and energy for developing and bringing new technologies to market. In the long run, this could dampen the pace of medical advancement despite rising global demand for better, more advanced orthopedic care.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Plates Screws |

| By Material Type |

Metallic Implants Polymer Implants Composite Materials Others |

| By Application |

Orthopedic Applications (Fracture Fixation) Dental / Maxillofacial Applications Craniofacial Applications Trauma Reconstruction Osteotomy Arthrodesis Others |

| By End User |

Hospitals & Clinics Orthopedic Clinics Ambulatory Surgical Centers (ASCs) Specialty Clinics Research & Academic Institutions |

| Key Players |

Johnson & Johnson (DePuy Synthes) Stryker Corporation Zimmer Biomet Holdings Inc. Smith & Nephew PLC Medtronic PLC B. Braun Melsungen AG (Aesculap division) Arthrex Inc. Globus Medical Inc. NuVasive Inc. Orthofix Medical Inc. Exactech Inc. Medartis aap Implantate AG Integra LifeSciences CorporatioN MicroPort Scientific Corporation Enovis (formerly DJO Global) Medacta ulrich medical CarboFix Orthopedics Syntellix ChM |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Screws and Plates Market is categorized by product type, by technology, by application and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Each segment provide a comprehensive understanding of its dynamics and growth opportunities. The Medical Screws and Plates Market is highly dynamic and segmented to provide a comprehensive understanding of its various facets.

The orthopedic plates and screws market is fundamentally segmented based on the specific types of fixation devices used in a wide range of surgical procedures. This segmentation is essential, as different fractures and anatomical locations require tailored solutions for optimal healing and stability. Plates play a critical role in fracture fixation, and among them, locking plates are widely used, particularly in cases involving complex or osteoporotic fractures.

These plates offer angular stability and come in two main forms: Variable Angle Locking Plates (VALCP), which allow surgeons flexibility in screw placement, and Fixed Angle Locking Plates (LCP), which provide rigid fixation. In contrast, non-locking plates such as Dynamic Compression Plates (DCP) and Limited Contact DCP (LC-DCP) are traditional devices that achieve bone stabilization through direct compression. For anatomically challenging or irregular areas, reconstruction plates are designed to be shaped or contoured during surgery to fit the bone precisely.

Specialty plates further enhance treatment options by addressing specific surgical needs these include periarticular plates for joint areas, anatomical plates pre-contoured for particular bones, and osteotomy plates used in corrective bone procedures. On the other hand, the market for screws is equally diverse. Cortical screws are engineered for the dense outer layer of bone, featuring fine threads, while cancellous screws have coarser threads suited for the spongier, inner bone structure. Locking screws are designed to be used with locking plates, creating a fixed-angle construct that improves stability in compromised bone. Cannulated screws, which are hollow and inserted over a guide wire, offer enhanced accuracy during minimally invasive procedures.

Additionally, headless screws are fully embedded within the bone, helping reduce soft tissue irritation, making them ideal for small bone or joint procedures. Lag screws are used to compress bone fragments together, promoting faster healing. There are also self-tapping and self-drilling screws, which simplify the surgical process by eliminating the need for pre-drilling. The broader category of bone screws encompasses a variety of types used for general bone fixation, while pedicle screws are specially designed for spinal fusion surgeries, providing critical support for the vertebral column. Together, these segments reflect the complexity and precision required in orthopedic surgery, highlighting the importance of tailored devices for specific clinical needs and driving continued innovation within the industry.

The choice of material in orthopedic plates and screws is a critical factor, as it directly impacts the implant’s strength, biocompatibility, and whether it will remain in the body permanently or eventually be removed. Metallic implants have long been the standard in the field, with stainless steel (such as 316L) being historically dominant due to its excellent mechanical strength, corrosion resistance, and affordability. It remains a widely used option, particularly in trauma cases.

However, titanium and titanium alloys (like Ti-6Al-4V) are increasingly becoming the preferred choice, thanks to their superior biocompatibility, high strength-to-weight ratio, and compatibility with MRI imaging. These properties make titanium especially suitable for long-term implantation. For applications requiring exceptional durability under stress, cobalt-based alloys are employed, offering outstanding wear resistance in high-load situations.

On the innovation front, magnesium alloys are gaining attention as biodegradable metals. These materials gradually dissolve in the body, reducing the need for secondary removal surgeries, an especially appealing option in pediatric and trauma care. Alongside metals, polymer implants are gaining traction, particularly bioabsorbable or biodegradable polymers such as PLLA, PLA, and PEEK (Polyether Ether Ketone). These materials break down naturally in the body over time, eliminating the need for follow-up procedures to remove the implant.

PEEK is notable for its radiolucency meaning it doesn’t interfere with X-rays and for having an elastic modulus close to that of natural bone, which helps reduce stress shielding. For cases where permanent fixation is needed, non-resorbable polymers are still utilized. In some instances, composite materials—which combine metals and polymers are used to balance strength, flexibility, and biological integration. Beyond these, a small but growing segment of emerging materials continues to push the boundaries of what’s possible in orthopedic care. Overall, material choice is becoming more personalized and application-specific, reflecting the evolving demands of modern orthopedic surgery.

The orthopedic plates and screws market can be segmented based on where these devices are primarily used in the body, offering a clear picture of their diverse clinical applications. The largest and most dominant segment is orthopedic fracture fixation, which spans both upper and lower extremities and addresses a wide range of injuries and conditions. In the upper extremity, plates and screws are commonly used to treat humeral fractures (in the shoulder and upper arm), clavicle fractures (collarbone), scapula fractures (shoulder blade), elbow fractures, and distal radius and forearm fractures, which are especially common from falls.

Smaller, more delicate devices are used for hand and wrist fractures, including metacarpal and phalangeal breaks. In the lower extremity, the demand is equally significant, with devices used for stabilizing femoral fractures (particularly around the hip), tibial fractures (the shin bone), and ankle and foot fractures, including metatarsal injuries. Pelvic fractures, often resulting from high-impact trauma, also require specialized plating systems. Beyond limb fractures, spinal fixation is another major application area. Devices like pedicle screws and anterior cervical plates are essential for spinal fusion surgeries and stabilization, particularly in cases of degenerative conditions, trauma, or deformities.

Dental and maxillofacial applications represent a specialized but important segment, involving the use of small, precision-engineered plates and screws for jaw corrections, facial bone reconstruction, and dental implants. Closely related are craniofacial applications, which focus on skull and facial bone reconstruction, often following trauma, congenital abnormalities, or tumor resections. The market also extends into procedural categories. In trauma cases, plates and screws are vital for the immediate stabilization of acute injuries.

Reconstruction procedures use these devices to rebuild or restore damaged bone structures. Osteotomy, where bones are cut and repositioned to correct deformities, relies heavily on stable fixation systems. Similarly, arthrodesis or joint fusion surgery uses screws and plates to achieve long-term bone union. Lastly, the “others” category includes niche applications such as sports medicine, where specialized fixation devices are used to treat athletic injuries with a focus on rapid recovery and joint preservation. Together, this broad range of applications highlights the critical role that plates and screws play in modern surgical care across nearly every area of the body.

The end-user landscape for orthopedic plates and screws is diverse, reflecting the range of healthcare settings in which these devices are utilized. Hospitals and clinics make up the largest and most critical segment, as they handle a high volume of complex surgical procedures and trauma cases. These facilities are equipped with advanced surgical infrastructure and specialized teams, making them the primary centers for orthopedic implant use, especially in emergencies and multi-disciplinary cases.

Orthopedic clinics represent another important segment, offering specialized care focused exclusively on musculoskeletal conditions. These centers often perform planned, elective surgeries and provide ongoing patient care, making them key users of implants designed for long-term fixation and recovery. Ambulatory surgical centers (ASCs) are rapidly gaining traction due to their cost-effective and patient-friendly approach to care. As more orthopedic procedures shift to outpatient settings, ASCs are becoming increasingly important for their ability to perform surgeries in a streamlined, efficient environment. This trend is driving demand for implants that are optimized for quicker procedures and faster recovery.

Specialty clinics, which may focus on areas like sports medicine or spine care, also contribute to the market by catering to specific types of injuries or patient populations, requiring customized implant solutions. Lastly, research and academic institutions play a foundational role in the development and testing of new materials, designs, and surgical techniques. These centers are crucial for innovation, clinical trials, and training the next generation of orthopedic surgeons, making them an important though smaller part of the overall end-user ecosystem. Together, these varied healthcare settings underscore the widespread and growing reliance on orthopedic plates and screws in modern medicine.

The global medical screws and plates market shows marked regional differences, with each area shaped by unique growth drivers, levels of market maturity, and competitive dynamics. From 2024 to 2033, these regional variations will continue to influence how the market evolves. In North America, particularly the United States, the market remains highly mature, driven by a strong healthcare infrastructure, early adoption of advanced surgical technologies, and the presence of major industry players.

The region also benefits from high healthcare spending and a large aging population, further fueling demand for orthopedic implants. Europe presents a mixed picture, with Western European countries like Germany, France, and the UK leading in terms of adoption and innovation, while Eastern Europe is expected to experience faster growth due to improving healthcare systems and increasing access to advanced surgical care.

Asia-Pacific is emerging as one of the most promising regions, fueled by rapid urbanization, growing awareness of orthopedic health, expanding healthcare coverage, and a surge in the elderly population. Countries such as China, India, and Japan are investing heavily in medical infrastructure, making this region a hotbed for future growth.

Latin America and the Middle East & Africa are also showing steady progress. Although these regions currently have lower market penetration, they offer significant potential due to a rising burden of orthopedic conditions, increasing government healthcare initiatives, and improving access to specialized medical care. Each region brings its own opportunities and challenges, but together they contribute to a dynamic global market landscape that will continue to expand over the next decade.

North America particularly the United States continues to dominate the global medical screws and plates market, a position it is expected to maintain well into the forecast period. This leadership is underpinned by a combination of structural, demographic, and technological advantages. The region benefits from a highly advanced healthcare infrastructure, with a dense network of specialized orthopedic surgical centers and a strong emphasis on expert care. This creates a favorable environment for the widespread use of sophisticated implants.

Aging demographics play a significant role in driving demand, as the U.S. faces a growing number of age-related bone conditions such as osteoporosis and fragility fractures. Additionally, the region sees a high rate of sports-related injuries and road accidents, further increasing the need for reliable fracture fixation solutions. North America is also known for being at the forefront of technological adoption, with early integration of innovations like minimally invasive surgical techniques, 3D-printed patient-specific implants, and advanced materials such as bioresorbable and variable-angle locking systems.

Supportive reimbursement policies and broad insurance coverage help ease the financial burden of high-cost procedures, allowing greater access to cutting-edge treatments. Moreover, the presence of many leading global orthopedic implant manufacturers in the U.S. has made the region a hub for research and development, accelerating the introduction of new products to market. Ongoing trends include a focus on next-generation implant materials, digitally guided surgical planning tools, and a rising demand for premium and specialized solutions tailored to individual patient needs all reinforcing North America’s dominant position in this growing global market.

Europe holds a significant share of the global medical screws and plates market and is poised for steady growth over the coming years. While its growth rate may not match that of some rapidly expanding emerging markets, Europe’s mature healthcare infrastructure and aging population provide a strong foundation for continued market expansion. Much like North America, Europe faces a rising number of elderly patients, which has led to a high prevalence of age-related conditions such as osteoporotic fractures and other degenerative bone diseases driving consistent demand for orthopedic implants.

Western Europe, in particular, benefits from robust healthcare systems that ensure widespread access to orthopedic care, enabling the regular use of fracture fixation devices in both trauma and elective procedures. The region also shows growing demand for bone fixation solutions across a range of clinical applications, supported by the adoption of advanced technologies. There is a notable shift toward the use of anatomical plates that better fit specific bone structures, enhancing patient recovery and surgical outcomes.

Additionally, the use of biocompatible materials, especially titanium, is on the rise, although stainless steel remains prevalent in some markets due to its ease of removal and cost-effectiveness particularly important in Europe, where implant removal after healing is more common than in North America. Despite strong overall adoption, regional variations persist. Western European countries like Germany, France, and the UK are quicker to implement innovative surgical techniques and materials, while some parts of Eastern Europe face limitations due to tighter budgets, regulatory complexity, and infrastructure disparities. Nevertheless, Europe’s emphasis on patient-specific care, technological refinement, and safety standards continues to shape a dynamic and evolving orthopedic implant market.

The Asia-Pacific (APAC) region is emerging as the fastest-growing market for medical screws and plates, with strong momentum expected to continue through the forecast period. This rapid growth is fueled by several converging factors. One of the most significant is the region’s sheer population size particularly in countries like China, India, and Japan combined with a rapidly aging demographic, creating a substantial and growing patient pool requiring orthopedic care.

As musculoskeletal disorders, fractures, and degenerative bone conditions become more prevalent, the demand for surgical interventions and fixation devices is accelerating. Healthcare infrastructure across many APAC nations is undergoing a major transformation. Governments and private sectors are investing heavily in expanding and upgrading hospitals, clinics, and surgical centers, especially in urban and semi-urban areas. This development is making advanced orthopedic care more accessible to a broader segment of the population. At the same time, rising disposable incomes and a growing middle class are enabling more people to afford modern medical treatments, including implants and fixation devices.

Awareness of orthopedic conditions and the availability of surgical solutions is also increasing, contributing to higher treatment-seeking behavior. Urbanization and lifestyle changes have led to a spike in road traffic accidents and sports-related injuries, further driving the demand for trauma-related bone fixation products. While high-end implants are still often imported, countries like China and India are rapidly strengthening their local manufacturing capabilities and investing in R&D. This not only improves supply chain efficiency but also enables cost-effective production, aligning well with the price-sensitive nature of many APAC markets.

Key trends shaping the region include rising adoption of titanium implants, strong demand for both basic and advanced fixation solutions, and a growing emphasis on localized production and competitive pricing. Moreover, the booming medical tourism sector, particularly in countries like India, Thailand, and Malaysia is also bolstering demand, as international patients seek affordable yet high-quality orthopedic treatments. Altogether, these factors position APAC as a dynamic and highly promising region in the global medical screws and plates market.

The Middle East and Africa (MEA) region represents a developing yet promising market for medical screws and plates, characterized by growing momentum and untapped potential. Although the market currently operates from a relatively smaller base compared to more mature regions, several factors are driving its upward trajectory. A key growth catalyst is the substantial investment being funneled into healthcare infrastructure, particularly in wealthier Gulf nations like Saudi Arabia and the United Arab Emirates. These countries are actively modernizing hospitals and medical facilities as part of broader national health reforms, which include upgrading surgical capabilities and expanding specialized services such as orthopedics.

The demand for orthopedic interventions is also on the rise across the MEA region, fueled by a growing number of trauma-related injuries, many resulting from traffic accidents, and a gradually aging population that is increasingly affected by bone and joint disorders. As a result, the volume of orthopedic surgeries is steadily increasing, prompting greater demand for fixation devices such as screws and plates. Additionally, the region is witnessing the gradual adoption of advanced medical technologies, most of which are imported from established global manufacturers. This is helping raise the standard of care and introduce more modern treatment protocols. Current trends in the MEA market include a stronger emphasis on enhancing trauma care services and the expansion of specialized orthopedic centers. There is also a growing awareness among both patients and providers about advanced surgical options, which is contributing to rising acceptance and adoption.

However, the pace of progress varies considerably within the region. While countries like the UAE are leading in terms of technology adoption and healthcare quality, other parts of the region, particularly in less developed nations, face challenges related to infrastructure gaps, affordability, and regulatory complexity. Despite these disparities, the overall outlook for the MEA medical screws and plates market is positive, with continued improvements expected in access, awareness, and clinical capabilities over the coming years.

The medical screws and plates market was valued at USD 6.6 billion in 2024.

The medical screws and plates market is projected to grow at a CAGR of 30.8% from 2025 to 2033.

The Screws segment holds the largest medical screws and plates market share.

The Asia-Pacific region is expected to witness the highest growth rate.

The medical screws and plates market major players include Johnson & Johnson (DePuy Synthes), Stryker, Zimmer Biomet, Smith & Nephew, and Medtronic.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Screws and Plates Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Screws and Plates Market, By Material Type

5.3 Medical Screws and Plates Market, By Application

5.4 Medical Screws and Plates Market, By End User

6.1 North America Medical Screws and Plates Market, By Country

6.1.1 Medical Screws and Plates Market, By Product Type

6.1.2 Medical Screws and Plates Market, By Material Type

6.1.3 Medical Screws and Plates Market, By Application

6.1.4 Medical Screws and Plates Market, By End User

6.2 U.S

6.2.1 Medical Screws and Plates Market, By Product Type

6.2.2 Medical Screws and Plates Market, By Material Type

6.2.3 Medical Screws and Plates Market, By Application

6.2.4 Medical Screws and Plates Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping