Dental X-Ray Market

Dental X-Ray Market Share & Trends Analysis Report By Product (Analog X-Ray Systems, Digital X-Ray Systems) By Type (Intraoral X-Rays, Bitewing, Periapical, Occlusal, Extraoral X-Rays, Panoramic, Cephalometric) By End User (Dental Hospitals & Clinics, Dental Academic & Research Institutes, Forensic Laboratories) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code : ASIPHR1011

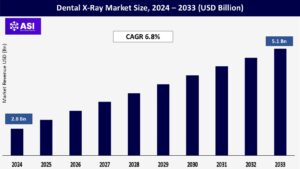

CAGR: 6.8%

Last Updated : August 27, 2025

The global market for Dental X-Rays was worth around USD 2.8 billion in 2024 and is expected to grow to USD 5.1 billion by the year 2033, with a CAGR of 6.8% from 2025-2033.

Dental X-ray systems are indispensable diagnostic instruments in the field of dentistry; they are used to produce diagnostic information including images of the oral cavity, teeth, bones, and soft tissues to check for cavities, bone loss, and other dental problems. Dental X-ray systems are also essential when planning treatments such as implants, root canals, and orthodontic treatment.

Dental X-ray systems include both intraoral and extraoral radiographs including extraoral imaging such as panoramic and cephalometric imaging which provide high-resolution diagnostics using minimal radiation exposure. The advent of digital systems has enabled faster image distribution and processing capabilities and better archiving and sharing features than analog systems.

Major factors driving growth of the dental X-ray market include the rising incidence of dental disorders, increasing awareness of oral related health issues, advances in digital imaging technology, and growing concerns surrounding cosmetic dental procedures. Furthermore, government funding for improved dental care resources, the expansion of dental tourism in developing markets, and numerous other factors are influencing the growth of the dental X-ray market.

The rising rates of dental diseases such as caries, periodontitis, and oral cancer are a major factor driving the market for X-ray systems. Oral diseases are the most common health condition in the world, impacting almost 3.5 billion people according to the World Health Organization (WHO). Untreated dental caries (tooth decay) in permanent teeth represents the most common of these conditions; the trend is upticking.

The increase in oral health issues has led to a greater need to provide accurate and early diagnostics, in which dental X-ray systems are a key component. Dental X-ray technology is beneficial for both detection of tooth decay, monitoring bone loss, assessing tooth development, and developing treatment plans. The American Dental Association (ADA) recommends radiographic exams as part of preventive care for diagnosed patients, or for people perceived to be at risk (e.g., children, people with diabetes, people age 30 or older).

In the USA dental insurance policies are increasingly covering annual preventive checkups and for imaging; therefore clinicians will improve the need in compliance. Emerging economies, such as India and Brazil, have increased awareness of oral hygiene as well dental-related conditions and the means to access dental services have been growing as well, which can compound the effect across the market.

Quick changes in dental imaging technology, especially this idea of moving from analog to digital systems, have vastly improved the accuracy of diagnosis and improved speed, in addition to improving radiation safety. Digital dental X-ray systems can acquire images faster, allow for better image storage and sharing, and reduce radiation exposure making them better choice to have in dental practices.

For example, in June 2023, Carestream Dental launched its CS 9600 CBCT system equipped with AI-powered positioning technology, which led to more accurate and reproducible imaging results. Planmeca introduced its ProX intraoral X-ray unit, which was designed to obtain low-dose imaging results and supported image-aided AI diagnostic tools.

AI-based tools are also now available for lesion detection and offer automatic measurements, which streamlines the process of obtaining an image along with improving efficiency and reducing diagnostic errors. In these ways, innovations in dental imaging are changing diagnostics from a reactive care element to a more predictive aspect of care. This will help the dentist assess risks prior to symptoms appearing, leading to greater adoption across routine, surgical, and cosmetic procedures.

A major constraint in the dental X-ray market is the significant upfront costs related to the purchase and maintenance of modern advanced imaging systems, specifically digital and cone-beam computed tomography (CBCT) units. For instance, high-end digital intraoral systems cost approximately $10,000–$30,000, CBCT units cost about $60,000, to sometimes even greater than $150,000 depending on specifications and brand.

Due to the capital intensive nature of the product, it is a significant constraint for small- to mid-sized dental facilities; this is especially true in developing countries where limited budgets and limited government subsidization have limited them from utilizing more advanced technology. Additionally, many dental facilities in rural or semi-urban communities across Asia, Africa, and Latin America still continue to work from outdated analog X-ray units, paying just slightly less than advanced digital options, even if their quality of diagnostic imaging is limited.

In India, one of the country’s leading medical products, many private practitioners in tier-2 and tier-3 cities note that investing in a digital X-ray system is difficult to justify first without insurance support and/or a government incentive for them. The issues with affordability and is further worsened since they have no options of alternatively financing the device, especially since they add import duties on top for medical devices.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Analog X-Ray Systems Digital X-Ray Systems |

| By Type |

Intraoral X-Rays Bitewing Periapical Occlusal Extraoral X-Rays Panoramic Cephalometric |

| By End User |

Dental Hospitals & Clinics Dental Academic & Research Institutes Forensic Laboratories |

| Key Players |

Dentsply Sirona Planmeca Group Carestream Dental LLC Vatech Co., Ltd. Danaher Corporation (Envista Holdings) Midmark Corporation Owandy Radiology Cefla S.C. (NewTom) Acteon Group Yoshida Dental Mfg. Co., Ltd. Asahi Roentgen Air Techniques, Inc. PreXion, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Dental X-Ray Market is segmented by product, type, and end-user. Each segment plays a crucial role in improving diagnostic accuracy, workflow efficiency, and patient outcomes in dental practices.

Digital X-Ray Systems accounted for the largest market share of 67.4% in 2024 as a result of their rapid image processing, lowered radiation exposure, and convenience for storing and retrieving digital images. As digital systems become standard in dentistry, their adoption is accelerated by the newer generation of systems which can also provide direct integration to eHealth records and AI-based diagnostics. The most pronounced transition from analog to digital system is occurring in more developed markets that have established regulatory structures and reimbursement schedules, for example, the U.S., Germany, and Japan.

Analog X-Ray Systems, while witnessing a continued decline in utilization, are still used in cost-sensitive parts of the world (e.g. parts of Africa, South Asia, and Latin America), where accessibility and affordability for the initial investment in equipment continues to be an obstacle. However, with the move toward digitization finding its way into wider uses, analog systems are ultimately becoming less and less often used.

Intraoral X-Rays led the solution segment with 58.2%, as they are routinely used to identify decay, examine bone levels, and plan cavities, crowns, and root canals. The main two types of intraoral are bitewing and periapical which can be represented as the traditional X-Ray with separate views of individual teeth and the level of bone with respect to those teeth.

Extraoral X-Rays are growing, especially panoramic X-Rays and cephalometric, which is expected to grow at a CAGR of 7.1% till 2033. Panoramic X-Rays are gaining traction in becoming a new standard of care in implantology, oral surgery, and orthodontics. Panoramic X-Rays have become popular due to the ability to capture the entire mouth in a single view. Cephalometric imaging has been used for years for orthodontic purposes, mainly to plan movements in the jaws and maxillofacial area.

The dental X-ray market will be led by Dental Hospitals & Clinics, with a projected market share of 64.8% in 2024 and most major segments under the umbrella of preventive and corrective care. The majority of dental X-ray exams, such as intraoral and panoramic, are performed outside of private practice settings in dental hospitals and clinics with access to advanced imaging systems and technologists who have gone through the proper training.

The segment for Dental Academic & Research Institutes is expected to show a stable trend as Plans to cease, replace or advance the use of radiographic imaging in training dental professionals and clinical research is considered foundational. Dental academic institutions typically have advanced imaging systems in place to account for changing their approach if new imaging technologies emerge that could further their mission.

The other portion, but substantially less, belongs to Forensic Laboratories. In these cases, the request for dental X-rays is either to inspect of a legal case, military forensic case, or identification to benefit a life. The growth in this segment has come from more investment in these types of forensic infrastructures and joint opportunities via inter-agency cooperation in dealing with disaster recovery.

North America captures the highest share of 38.5% of the market in 2024 due to the region’s established dental care infrastructure and awareness, as well as improved adoption of advanced digital imaging technologies. The United States is the major contributor due to the existence of top dental equipment manufacturers, insurance coverage of dental diagnostics, and increased dental visits.

In fact, the American Dental Association (ADA) indicates that around 85% of adults in the U.S. have a dentist visit at least once every two years, supporting consistent demand for diagnostic X-ray examinations. Canada is also exhibiting increasing adoption of digital dental imaging, particularly in urban clinics and educational institutions.

Europe is the second-largest contributor to the market, globally. Germany, the UK, France, Italy and the Netherlands play key roles in the continent’s market share. In 2024, Europe contributed approximately 28.3% of the global market. The global market continues to grow due to the increasing population of elderly adults, an increasing burden of dental diseases, and government-funded oral health programs.

Germany is unique as it has a significant number of dental imaging centers in place, along with effective and regularly updated reimbursement policies supporting imaging in both general and specialized dentistry. Data from the OECD shows that more than 75% of adults in Europe have dental imaging conducted at least once every two years, which reflects a significant volume of procedures.

The Asia-Pacific is projected to be the fastest-growing region developing a CAGR of 8.1% from 2025 to 2033. The increase in urbanization, emphasis on oral health, increased disposable incomes with a rapid increase in digital infrastructure funding from governments across countries such as China, India, Japan, and South Korea will contribute to the development of the market size.

The National Health Commission of China continues to push for the detection of oral diseases at an early stage as a public health obligation. Japan continues to add resources to their geriatric care for aging citizens with respect to dental care as diagnostic imaging will be a component to advancement in care protocols. In India and Thailand, the private dental clinic, and dental tourism opportunities developed additional market penetration for digital X-ray systems.

Latin America, and the Middle East & Africa (MEA) regions are continuing with moderate growth with supportive improvements in healthcare investments, an expanding middle-class population, and improved access to dental services. Brazil and Mexico are the two main countries in Latin America that accounted for the overall growth of the market size with an increase in private dental clinics and uptake of digital dentistry practices.

Countries in the MEA region, such as the UAE and Saudi Arabia, are investing money and resources into changing their healthcare infrastructure to digitally include dental diagnostics. Growth is limited as healthcare access varies, funding for insurance is limited in public-sector health, and budgets are difficult for healthcare systems.

The market was valued at USD 2.8 billion in 2024.

The market is projected to grow at a CAGR of 6.8% from 2025 to 2033.

The Intraoral X-ray hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Dentsply Sirona, Planmeca Group and Carestream Dental LLC

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Dental X-Ray Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Dental X-Ray Market, By Type

5.3 Dental X-Ray Market, By End User

6.1 North America Dental X-Ray Market, By Country

6.1.1 Dental X-Ray Market, By Product

6.1.2 Dental X-Ray Market, By Type

6.1.3 Dental X-Ray Market, By End User

6.2 U.S.

6.2.1 Dental X-Ray Market, By Product

6.2.2 Dental X-Ray Market, By Type

6.2.3 Dental X-Ray Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping