Medical Digital Imaging System Market

Medical Digital Imaging System Market Share & Trends Analysis Report, By Product Type( X-ray Imaging Systems, Computed Tomography (CT) Scanners, Magnetic Resonance Imaging (MRI) Systems, Ultrasound Systems, Nuclear Imaging Systems, Mammography Systems, Fluoroscopy Systems) By Application (Cardiology, Neurology, Orthopedics, Oncology, Gynecology, Gastroenterology, Dental Applications, Urology, General Imaging) By End-User (Hospitals, Diagnostic Imaging Centers, Specialty Clinics, Ambulatory Surgical Centers (ASCs), Academic and Research Institutes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

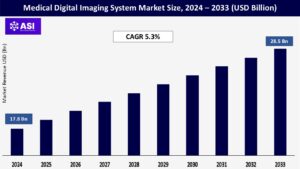

CAGR: 5.3%

Last Updated : March 7, 2026

The global Medical Digital Imaging System Market was valued at approximately USD 17.8 billion in 2024 and is projected to reach USD 28.5 billion by 2033, growing at a CAGR of 5.3% during the forecast period (2025–2033).

Medical digital imaging systems represent advanced methodologies for capturing, processing, and storing images of the human body for purposes that include clinical diagnosis, treatment planning, and monitoring. These systems are considered advanced digital imaging technologies such as X-rays, MRI, CT, Ultrasound, and Nuclear imaging, which allow users to observe high-resolution images of internal human anatomical structures and perform real-time imaging with non-invasive or minimal invasive imaging rather than with invasive approaches. Digital imaging enables improved diagnostic accuracy, improves workflow using PACS (Picture Archiving and Communication Systems), and allows commonality with AI-assisted diagnostic imaging.

The growth of the market for Digital imaging is driven by an increasing burden of chronic diseases, increasing age of populations worldwide, increased innovations in imaging modalities and increase demand for earlier and more accurate diagnosis. The market growth is also being driven by increased acceptance of Digital health approaches, and throughout the world, government departments are supporting initiatives to develop modern healthcare and health infrastructure.

The growing global incidence of chronic diseases, including cancer, cardiovascular diseases, diabetes, and neurological disorders, is significantly contributing to the growth of the medical digital imaging system market. Many of these chronic diseases require timely and accurate imaging for diagnostics, therapy planning, and disease follow-up. The World Health Organization (WHO) estimates that non-communicable diseases (NCDs) contributed to almost 74% of all deaths worldwide, with cardiovascular diseases and cancer being the leading killers.

In 2023, the International Agency for Research on Cancer (IARC) reported that there were over 20 million new global cases of cancer and estimated that this number will exceed over 30 million cases by 2040. These statistics illustrate the increasing demand for advanced imaging modalities, including MRI, CT, PET scan, and digital mammography. These imaging technologies are essential for the detection of tumors and other abnormalities in the cardiovascular and neurological systems in their early stages.

For example, Siemens Healthineers launched its MAGNETOM Free. Max MRI system towards enabling easy access to high-field imaging for lung and cardiac assessment,s particularly in low-resource settings. The increasing demand for timely and accurate diagnostic imaging for the management of the disease burden is greatly driving the medical digital imaging system market.

Rapid improvements in imaging technology and imaging-related artificial intelligence (AI), machine learning, and automation have produced huge shifts in all imaging contexts, including the medical digital imaging landscape. AI-equipped medical imaging devices provide improved image interpretation, automated reporting and diagnostics, improved workflow throughput, and predictive analytics.

One example is GE HealthCare’s AI-based Revolution Apex CT scanner, launched in January 2023, which utilized deep learning to facilitate improvements in image clarity and to lower radiation doses by about 82%—an enormous advantage from a patient safety perspective. The increased prevalence of portable and point-of-care imaging, including but not limited to digital X-ray and ultrasound, is expanding imaging’s applicability in emergency settings, remote locations, or ICU units.

For example, Philips Entertainment announced its Compact Ultrasound 5000 series in March 2024, which features built-in AI tools for obstetrics, cardiac, and abdominal imaging, empowering faster decision-making during critical care scenarios. These transformative impacts on imaging practice have been spurred by heavy investments into healthcare modernization efforts.

Substantial capital investment from both the public sector and private enterprises, along with the rising investments in healthcare digitization and modernization, have established upgrades to radiology infrastructures in the U.S., China, and India, along with investments in PACS and RIS systems, and training of clinicians in AI-based interpretation of diagnoses and reporting—all of which continue to reinforce demand for digital imaging systems around the world.

A significant limitation in the medical digital imaging system market is thehigh capital and ongoing cost of the forms of advanced imaging technology, including MRI, PET/CT, and photon-counting CT scanner devices. These systems require significant investment not only in acquiring the equipment (more than USD 1 million to more than USD 3 million), but also in site preparation, shielding, and employing specialized personnel to operate and maintain the devices.

For example, when purchasing a high-field 3T MRI scanner, the site will require changes to infrastructure and there are usually long-term maintenance contracts that can be cost-prohibitive for small clinics and primary care health facilities in low- and middle-income countries. Furthermore, reimbursement for some imaging procedures is limited or unavailable in both the private and public insurance spaces, which serves to limit investment. These economic barriers slow the adoption of digital imaging in rural areas and emerging markets, and subsequently create inequities in access to diagnosis and healthcare outcomes.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

X-ray Imaging Systems Computed Tomography (CT) Scanners Magnetic Resonance Imaging (MRI) Systems Ultrasound Systems Nuclear Imaging Systems Mammography Systems Fluoroscopy Systems |

| By Application |

Cardiology, Neurology Orthopedics Oncology Gynecology Gastroenterology Dental Applications Urology General Imaging |

| By End User |

Hospitals Diagnostic Imaging Centers Specialty Clinics Ambulatory Surgical Centers (ASCs) Academic and Research Institutes |

| Key Players |

Siemens Healthineers GE HealthCare Philips Healthcare Canon Medical Systems Corporation Fujifilm Holdings Corporation Hologic, Inc. Carestream Health Samsung Medison Shimadzu Corporation Esaote SpA Konica Minolta, Inc. Agfa-Gevaert Group Neusoft Medical Systems Mindray Medical International Limited United Imaging Healthcare |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Digital Imaging System Market is segmented by Product Type, Application, and End-User. Each segment plays a vital role in enhancing diagnostic capabilities across diverse clinical specialties.

X-ray imaging systems captured the largest market share in 2024, due to their extensive use in routine diagnostics, trauma, and mobile imaging. The recent trend toward digital radiography (DR) has improved the quality of images and decreased radiation doses, which has increased the rate of adoption in hospitals and clinics. Demand continues to be strong for computed tomography (CT) scanners, due in part to their precision in imaging in parallel cross-sections, with specific advancements in oncology and emergency care.

The introduction of artificial intelligence (AI) enabled low-dose CT scanners provided by vendors such as GE HealthCare and Siemens Healthineers will increase the rate of adoption. Magnetic resonance imaging (MRI) systems are experiencing rapid growth based in areas of neurology and in musculoskeletal diagnostic imaging capabilities. There is increased demand for 3T and portable MRI scanners by client practitioners, particularly in developed regions where advanced clinical functionality is present.

Ultrasound systems that are primarily utilized in obstetrics/gynecology, cardiology, and point-of-care (POC) type locations are also strong. Portable and handheld ultrasound units are advancing imaging in low-resource environments. Along with PET, SPECT is also beginning to be utilized by oncologists and cardiologists as part of their diagnostic processes. There is a demand for Nuclear Imaging Systems (e.g., PET and SPECT) that are in a hybrid system format (e.g., PET/CT) as it improves the diagnostic precision.

Mammography Systems are continuing steady growth as programs for breast cancer screenings continue to evolve. Systems utilizing tomosynthesis (3D mammography) are rapidly being adopted. Fluoroscopy Systems continue to be widely used systems due to being used for real-time imaging applications, such as interventional procedures, orthopedics, and gastrointestinal studies. Fluoroscopy growth is supported by the movement toward minimally invasive procedures as well.

Cardiology is the biggest application area considering the extremely high burden of cardiovascular disease (CVD) across the world. Imaging technologies such as CT angiography, echocardiography, and nuclear cardiology technologies are exclusively used for diagnosis and eventual treatment planning. Neurology is the most growing segment considering the high increase in prevalence of stroke, dementia, and brain tumors. MRI and PET/CT imaging systems are extremely relevant in neurology.

Orthopedics has extensive use of X-ray, MRI, and CT imaging to assess conditions such as fractures, arthritis, and spinal problems. The ageing population and increase in sports injuries are certain determinants of Orthopedics imaging. Oncology is highly based on CT, MRI, PET, and ultrasound to find cancer early, to stage cancer, and to monitor the treatment of the cancer.

The use of hybrid imaging modalities is critical for precision oncology. In gynecology, hybrid imaging is achieved through ultrasound and magnetic resonance imaging (MRI) in the management of pregnancy, reproductive health, and diagnosis of uterine abnormalities. There is an increase in the demand and use of portable ultrasound for prenatal care. Fluoroscopy, ultrasound, and computed tomography (CT) imaging are for diagnostics in liver, pancreas, and bowel conditions in gastroenterology.

There is an increase in imaging-guided interventions, including the placement of intragastric balloons. Dental Applications utilize intraoral digital X-ray systems and cone beam computed tomography systems in their practice; dental imaging applications account for very high resolution. The growth in this area is mainly from cosmetic dentists incorporating more imaging in their practice, and high-resolution imaging for implant planning.

Urology also relies on ultrasound and CT imaging for imaging conditions like kidney stones, enlarged prostate, and urinary tract infections. General Imaging includes routine medical checks, injury assessments, and health screening as a preventive measure. We can see considerable demand for general imaging across multiple clinical departments.

The hospital segment retained the largest market share in 2024 due to their existing infrastructures for diagnostics, volumes of patients, and use of multimodal imaging systems. Leading hospitals are making investments to obtain AI-capable and hybrid imaging technologies for improved clinical decisions. Diagnostic Imaging Centers are rapidly emerging as standalone imaging facilities are providing faster appointments, more cost-effective options, and specialist diagnostic agents to patients.

Diagnostic Imaging Centers are investing more in advanced digital systems for a distinctive competitive edge. Specialty Clinics, such as cardiology, oncology, and neurology clinics are utilizing imaging modalities for the determination of diagnosis and management of other patient cohort and imaging-guided therapies. Portable imaging devices, direct digital x-ray, and focused imaging modalities are proving invaluable in these environments.

Ambulatory Surgical Centers are adopting portable digital imaging systems to pre-screen patients (ex. x-rays of orthopedic patients) for operative use and as images for intraoperative needs through their own infrastructure such as intraoperative fluoroscopy. Academic and Research Institutes are amongst the key buyers of high end MRI, CT, and nuclear imaging systems for research and training purposes and clinical trials. We are seeing a growing trend in Academic and Research attribute imaging systems towards supporting either imaging data into their AI and machine learning studies or using data for these studies.

In 2024, North America led the world in the medical digital imaging system market due to its advanced healthcare infrastructure, rapid adoption of state-of-the-art diagnostic technologies, and considerable healthcare expenditures. The U.S. is the dominant market for medical imaging systems in North America because the public and private sectors are investing in AI-integrated imaging and hybrid modalities, e.g., PET/CT, SPECT/CT, etc.

The innovative imaging systems approved by the FDA, notably portable MRI and handheld ultrasound devices, continue to spur market development. The region hosts many of the large medical imaging players (e.g., GE HealthCare and Hologic), which lends to an innovative environment and early adoption. Public healthcare initiatives, awareness of point-of-care ultrasound systems, and demand for these systems in rural/remote areas continue to support the growth of Canada.

Europe has a large share of the market as a result of the higher incidence of chronic diseases, an aging population, and strong reimbursement models. Germany, the UK, and France contribute to increased demand for MRI and CT imaging mainly for oncology and neurology. Initiatives like the EU’s “Europe’s Beating Cancer Plan” resulted in greater screening and early diagnosis, which increased demands for digital imaging solutions.

In addition, collaborative partnerships between imaging companies and university hospitals in Germany and the Netherlands have only helped to advance the adoption of AI-based diagnostic platforms and tele-radiology services in the region.

The medical digital imaging system market in the Asia-Pacific region is growing faster than any other region of the world driven by increased investments in healthcare, large populations of patients, and a growing awareness of early diagnosis. China and India lead the way as the fastest-growing markets due to the rapidly urbanizing population in cities and the areas surrounding their cities, along with the digital transformation of hospitals.

Government sponsored programs like China’s “Healthy China 2030” and India’s Ayushman Bharat are expanding access to imaging services for new patient populations as well. In Japan and South Korea, early adopters of high-end MRI systems and CT systems benefit from advanced healthcare systems. Major OEM manufacturers of imaging systems are building manufacturing plants in the region that can change the price points of medical imaging systems but also provide access to more of their local populations.

There is consistent growth in Latin America, driven by investments in health care infrastructure and public-private collaborations in diagnostics. Brazil and Mexico are the primary markets, both investing heavily in programs to modernize radiology and deploy digital advancements in health care networks. There is growing regional demand for mobile X-ray units and ultrasound systems, particularly in rural areas with limited access to imaging.

Nonetheless, economic instability and increasing inequities in access to health care will restrict the uptake of high-value imaging systems, while sales of refurbished equipment remains strong. The Middle East & Africa region is growing moderately, supported by increased investment in health care infrastructure in GCC nations like the UAE and Saudi Arabia, where they are building diagnostic centers with significant capabilities in digital CT, MRI and PET/CT.

Africa’s growth trajectory remains constrained due to limited budgets and inequity of access, however mobile imaging units and donor funded programs are helping to alleviate the burden. With increased medical tourism in the Middle East and Government led digital health programs, expect to see their market share increase in the future.

The market was valued at USD 17.8 billion in 2024.

The market is projected to grow at a CAGR of 5.3% from 2025 to 2033.

X- ray imaging Systems hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Siemens Healthineers, GE HealthCare and Philips Healthcare.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Digital Imaging System Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Digital Imaging System Market, By Application

5.3 Medical Digital Imaging System Market, By End-User

6.1 North America Medical Digital Imaging System Market, By Country

6.1.1 Medical Digital Imaging System Market, By Product Type

6.1.2 Medical Digital Imaging System Market, By Application

6.1.3 Medical Digital Imaging System Market, By End-User

6.2 U.S

6.2.1 Medical Digital Imaging System Market, By Product Type

6.2.2 Medical Digital Imaging System Market, By Application

6.2.3 Medical Digital Imaging System Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping