Surgical Robots Market

Surgical Robots Market Share & Trends Analysis Report, By Component (Robotic Surgical Systems, Instruments & Accessories, Services), By Application (Gynecological, Urological, Neurosurgery, Orthopedic, General & Other Surgeries), By End‑User (Hospitals, Ambulatory Surgical Centers)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

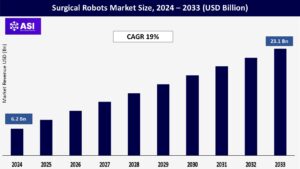

CAGR: 19%

Last Updated : August 20, 2025

The global Surgical Robots Market was valued at approximately USD 6.2 billion in 2024 and is projected to reach USD 23.1 billion by 2033, growing at a CAGR of 19% during the forecast period (2025–2033).

The Surgical Robots Market comprises advanced robotic systems used to assist surgeons in performing minimally invasive surgeries with enhanced precision, control, and flexibility. These robotic platforms are employed in a wide range of medical specialties including urology, orthopedics, cardiothoracic, gynecology, and general surgery. Surgical robots offer features such as 3D high-definition vision, articulated instrument arms, motion scaling, and tremor elimination, allowing for greater surgical accuracy and patient safety.

The core properties of surgical robots include real-time feedback, enhanced dexterity, minimal invasiveness, reduced blood loss, quicker recovery times, and lower infection risk. The increasing demand for precision surgeries and the integration of artificial intelligence in robotic systems are key factors driving market growth.

Minimally invasive procedures are becoming the gold standard across various surgical disciplines due to their benefits such as reduced postoperative pain, shorter hospital stays, minimal scarring, and faster recovery times. Robotic-assisted surgeries enhance precision, enable complex operations through small incisions, and reduce complication rates. As both patients and healthcare providers recognize these benefits, the demand for surgical robots continues to grow rapidly.

Modern surgical robots are now equipped with AI algorithms, real-time imaging, and machine learning capabilities. These systems assist in planning surgeries, navigating anatomy with higher precision, and adapting to patient-specific variations. Additionally, data collected during procedures is used for outcome prediction and training purposes. This integration boosts the capabilities of surgical robots and drives demand, especially in technologically advanced healthcare systems.

One of the most significant restraints on the Surgical Robots Market is the extremely high capital investment and ongoing maintenance costs associated with robotic surgical systems. A single surgical robot can cost anywhere between $1 million to $2.5 million, with additional costs for specialized surgical instruments, software updates, service contracts, and training programs for staff.

These expenses are difficult to justify for smaller hospitals and clinics, especially those with lower surgical volumes. Furthermore, the high total cost of ownership may deter healthcare systems in low- and middle-income countries, limiting the global penetration of robotic surgery.

| Report Metric | Details |

|---|---|

| By Component |

Robotic Surgical Systems Instruments & Accessories Services |

| By Application |

Gynecological Urological Neurosurgery Orthopedic General & Other Surgeries |

| By End-User |

Hospitals Ambulatory Surgical Centers |

| Key Players |

|

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Surgical Robots Market is segmented by Component, Application and End User. Each factor plays a critical role in transforming surgical practices, enhancing the precision and safety of complex procedures, and enabling faster patient recovery.

The combination of minimally invasive techniques, advanced imaging, and robotic precision is leading to better surgical outcomes, reduced hospital stays, and increased surgeon efficiency.

The Surgical Robots Market is segmented by component into Robotic Surgical Systems, Instruments & Accessories, and Services. Robotic Surgical Systems are the core of this market and include the main surgical console, robotic arms, and vision systems.

These systems enable precise, minimally invasive procedures and represent a significant capital investment for healthcare providers. Instruments & Accessories form a recurring revenue stream, comprising surgical tools such as cannulas, forceps, scissors, suturing tools, and energy devices specifically designed for robotic systems.

Due to their disposable or limited-use nature, this segment contributes significantly to ongoing operational costs. Services include training, maintenance, software updates, and system integration support, which are crucial for ensuring optimal performance and uptime of these high-tech systems.

By application, the market is divided into Gynecological, Urological, Neurosurgery, Orthopedic, and General & Other Surgeries. surgeries, including hysterectomies and fibroid removals, were among the first to adopt robotic systems due to the need for precision in the pelvic region. Urological surgeries, particularly prostatectomies, are a major growth area due to the effectiveness of robotic systems in navigating narrow anatomical spaces with reduced complications.

Neurosurgery is an emerging segment where robots assist in highly delicate spinal and cranial procedures, enhancing accuracy and reducing surgical fatigue. Orthopedic applications such as knee and hip replacements benefit from robotic planning and alignment systems, resulting in better implant placement and improved outcomes. General and other surgeries, including colorectal, thoracic, and bariatric procedures, are increasingly adopting robotic systems as the technology becomes more versatile and cost-effective.

In terms of end-users, the market is segmented into Hospitals and Ambulatory Surgical Centers (ASCs). Hospitals are the primary adopters of surgical robots due to their large budgets, multidisciplinary surgical departments, and the ability to spread the investment across high surgical volumes. They often integrate multiple robotic systems to cover various specialties.

Ambulatory Surgical Centers, though relatively new to robotic surgery, are seeing rising adoption due to the growing demand for same-day, minimally invasive procedures. Portable and cost-efficient robotic systems are enabling ASCs to expand their capabilities while maintaining affordability and quick patient turnover. This segment is expected to grow rapidly as technology becomes more accessible and compact.

The global leader in the surgical robots market, due to early adoption, robust healthcare funding, and high volumes of minimally invasive surgeries. The U.S. is home to several key players (e.g., Intuitive Surgical) and leads in robotic-assisted procedures across urology, gynecology, and orthopedics.

A well-established market with strong adoption in Germany, the UK, France, and Italy. A focus on precision medicine, favorable reimbursement scenarios, and support for technological innovation continue to drive robotic surgery adoption.

Emerging as a major growth engine, led by rising healthcare investments, large patient populations, and increasing awareness of minimally invasive procedures. China, India, Japan, and South Korea are rapidly adopting surgical robots, supported by both government funding and private hospital growth.

Still in the early stages of robotic surgery adoption. Brazil and Mexico are the primary markets where private hospitals and specialty centers are beginning to invest in robotic systems, though high costs remain a barrier.

Experiencing steady but limited adoption. Gulf countries like the UAE and Saudi Arabia are investing in advanced surgical technologies as part of broader healthcare modernization initiatives, while most African countries face infrastructural and financial hurdles.

The market was valued at USD 6.2 billion in 2024.

The market is projected to grow at a CAGR of 19% from 2025 to 2033.

Robotic Surgical Systems hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Intuitive Surgical, Inc., Medtronic plc and Stryker Corporation

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Surgical Robot Market , By Component

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Surgical Robot Market , By Application

5.3 Surgical Robot Market , By End User

6.1 North America Surgical Robot Market , By Country

6.1.1 Surgical Robot Market , By Component

6.1.2 Surgical Robot Market , By Application

6.1.3 Surgical Robot Market , By End User

6.2 U.S.

6.2.1 Surgical Robot Market , By Technology

6.2.2 Surgical Robot Market , By Application

6.2.3 Surgical Robot Market , By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping