Mobile Cardiac Telemetry Systems Market

Mobile Cardiac Telemetry Systems Market Share & Trends Analysis Report, By Technology (Lead-based Mobile Cardiac Telemetry Devices, Patch-based Mobile Cardiac Telemetry Devices) By End User (Hospitals, Cardiac Centers, Ambulatory Surgical Centers, Homecare Settings) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

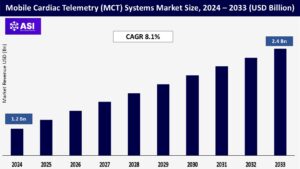

CAGR: 8.1%

Last Updated : March 7, 2026

The global Mobile Cardiac Telemetry (MCT) Systems Market size was valued at approximately USD 1.2 billion in 2024 and is projected to reach USD 2.4 billion by 2033, growing at a CAGR of 8.1% during the forecast period (2025–2033).

Mobile cardiac telemetry devices are sophisticated cardiac monitoring devices, allowing for real-time continuous recording and transmission of a patient’s ECG data for possible arrhythmias and other cardiac abnormalities. Mobile cardiac telemetry devices can utilize either a patch or lead-based technology to provide real-time ECG monitoring generally in an outpatient setting, improving diagnosis times and patient compliance.

MCT is the most advanced level of cardiac monitoring and offers real-time cardiac event notification in contrast to Holter monitors, the previous standard, which typically do not notify of abnormal cardiac events until after the recording period has ended. As a market, the MCT devices are experiencing growth from the rise of cardiovascular disorder patients, an increased demand for remote monitoring devices, growth of the aging population, and existing supported reimbursement in developed regions.

As the number of cardiac arrhythmias increases, the demand for mobile cardiac telemetry (MCT) systems has catapulted. As predicted by the Centers for Disease Control and Prevention (CDC), there will be an estimated 12.1 million people affected by atrial fibrillation (AFib) in the United States by 2030. AFib increases the risk of stroke fivefold, making early detection essential.

MCT systems employ continuous ECG monitoring and relay important telemetry data in real time much more reliably and securely than the methods used previously. MCT systems use video transmitters to better detect asymptomatic and/or intermittent arrhythmic events than Holter type monitors which have been used for decades that record data in 1, 2, or 3 days but without real time monitoring. Additionally, MCT systems have a better diagnostic yield than Holter monitors that allow for quicker diagnosis that can be essential in some emergency and non-emergency scenarios.

By raising the awareness and diagnosis of these abnormalities around the world, our reliance on systems to monitor these arrhythmias dramatically increases. Since the use of advanced technology has led to increased patient care beyond technology in hospitals and clinics, its clear that there will be more wearables available to monitor telemetry than ever before. Age related issues in populations such as Germany and Japan create a society with an increasing prevalence of arrhythmia incidences making the modification of traditional systems more ideal for timely telemonitoring of cardiac events.

The rapid growth of telehealth and remote patient monitoring (RPM) capabilities has been a primary driver of growth in the mobile cardiac telemetry systems market. The global push to deliver care to patients remotely—triggered largely by the COVID-19 pandemic—forced providers to push the investment envelope heavily into digital health technology.

The most well-suited technology for remote patient monitoring is MCT because it can provide real-time cardiac data sent to the physician from the patient’s home rather than a hospital. In 2023, the American Medical Association (AMA) produced a report where over 70% of doctors used telehealth modalities, versus just 25% before the pandemic. MCT fits into telehealth and provides better continuity of care especially in remote or low-income areas.

Companies like BioTelemetry (Philips) and iRhythm Technologies have adjusted their MCT offering to provide processes for remote diagnostics using AI based data analytics to down-sample high-risk patients. The elevated demand for affordable cardiac monitoring at home and reimbursement programs in places like the U.S. and Germany that support such methods will continue to foster the growth of the MCT systems market.

One of the main barriers limiting the growth of the mobile cardiac telemetry systems market is the high cost of purchasing the devices, transmitting data and monitoring services. Advanced MCT systems usually consist of multiple instances of wearable hardware, continuous ECG data analysis and remote monitoring infrastructure of the system. All these require considerable operational costs.

For example, developed nations such as the U.S. or parts of Europe are able to provide reimbursement systems that hospitals can rely upon through Medicare and private insurance. But developing markets typically don’t have reimbursement systems for remote cardiac monitoring services. Budget limitations for both healthcare providers and patients lead to financial disincentives, particularly in low-cost areas like Latin America, Southeast Asia, and parts of Africa, where access to MCT technology is limited.

Furthermore, maintenance and data storage limitations as well as interpretation services require expertise and back-end infrastructure that are often costly as well. Technical staff, such as trained engineers, also need oversight involving qualified personnel that have received training to service the maintenance needs of the MCT or remote ECG monitors.

Rural hospitals and outpatient clinics often could not implement MCT systems based on budget limitations, logistical support and lack of engineers or trained technicians. So the limited availability and access to MCT solutions in low- and middle-income countries present a significant barrier to the global expansion of the market despite the growing consumer demand for remote cardiac monitoring.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Lead-based Mobile Cardiac Telemetry Devices Patch-based Mobile Cardiac Telemetry Devices

|

| By End User |

Hospitals Cardiac Centers Ambulatory Surgical Centers Homecare Settings

|

| Key Players |

iRhythm Technologies (Philips) BioTelemetry, Inc. (Philips) Biotricity, Inc. Preventice Solutions, Inc. (an Abbott company) Hillrom (now part of Baxter International) Cardiac Insight, Inc. AliveCor, Inc. Medtronic plc GE Healthcare Qardio, Inc. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The growth of patch-based MCT devices is currently the fasted segment and they will lead the MCT market over the forecast period. Some patch MCT devices are designed to be small, wireless, and adhesive wearable chest patches that are typically not visible (unless you are paying attention) and can stay on the body for weeks. They are easy to apply/remove and patients can use them in their home environment or as outpatient monitoring devices.

The demand explosion for long-term ECG arrhythmia detection (e.g., paroxysmal atrial fibrillation) has led to increased adoption of these kinds of devices. It is anticipated that companies like iRhythm Technologies (Zio patch) and Biotricity will continue to innovate their products in this area. The lead based MCT devices will always have a place, particularly in clinical practice, as they provide much better accuracy in the detection of complex type arrhythmias.

Lead-based systems involve the use of electrodes applied to the patient’s chest with leads connected to the electrodes, and wirelessly transmitting either data or digitally recorded leads to an electronic monitoring station. The lead-based MCT systems are particularly important in acute care heart monitoring unit patients and in cardiovascular monitoring units where more intelligent and simultaneous monitoring is required in regards to heart failure events, ECG arrhythmias, etc.

Although these are more bulky and inconvenient for patients to wear, they do provide active monitoring and should trend relatively slower in the market than patch-based systems, but they will be considered an important pillar in the cardiac monitoring space, especially as it applies to higher and triage risk patients, where, in many application areas, lives depend on operational reliability in regards to diagnosing precision.

The Hospitals segment accounted for the largest market share while representing over 50% of the total Mobile Cardiac Telemetry Systems Market in 2024. Hospitals use MCT systems for inpatient applications (continuous cardiac monitoring for post-surgical patients), outpatient applications (ambulatory monitoring for arrhythmia cases and/or cardiac stability during medication titration), and also employ the MCT systems for timely clinical decision-making. Because hospitals operate electronic health record (EHR) systems and centralized telemetry centers, MCT is highly advantageous in a hospital setting.

Hospitals have a higher demand for telemetry systems due to the continued growth of cardiovascular conditions and the volume of patients routinely monitored for ambulatory or inpatient settings. The Home Care segment is considered the fastest-growing segment of end users. As remote patient monitoring continues to trend upwards and healthcare is decentralized, MCT devices are crucial for managing chronic cardiac conditions from home for patients with known arrhythmias, patients recovering from cardiac procedures, and patients with a very high-risk of stroke events (and high-level of concern) where wearable telemetry systems are utilized for ambulation and remote monitoring.

This segment will continue to grow as practitioners increase telehealth utilization across lines of service, infrastructure improves, and reimbursement policies for MCT services are implemented (e.g. United States, Germany).

In 2024, North America has the largest market share at 41.2% due to strong healthcare frameworks, an increasing burden of cardiovascular diseases, and an early adoption of remote monitoring technologies. The United States leads the region with strong reimbursement policies, high use of mobile cardiac telemetry in hospitals and outpatient settings, and high rates of atrial fibrillation.

According to the CDC, nearly 6 million Americans have AFib, which will be increased to 12.1 million by 2030. With several significant players in the MCT space, such as BioTelemetry (a Philips company), Preventice Solutions, and iRhythm Technologies, which are all headquartered in the U.S. They provide innovation and availability of patch- and lead-based MCT devices. The shift of the U.S. healthcare system to value-based care and remote patient monitoring will increase MCT market growth.

Europe occupies a greater share in the MCT systems market primarily due to countries like Germany, the UK, France, and the Netherlands. Europe also has an aging population, along with a growing increase in arrhythmias and stroke-related ailments. As an example, Germany has one of the biggest aging populations in Europe, currently having more than 22% aged 65 years or older in 2024. Consequently, these demographic transitions will lead to an increase in the demand for early detection of arrhythmias and home-based cardiac monitoring solutions.

Also, national health systems are beginning to promote integration with public health digital systems and governmental action, regulatory factors are enacting the uptake of mobile telemetry solutions. Lastly, while reimbursement policies differ from country to country, I expect increased government funding in digital health will create growth for the region.

Europe occupies a greater share in the MCT systems market primarily due to countries like Germany, the UK, France, and the Netherlands. Europe also has an aging population, along with a growing increase in arrhythmias and stroke-related ailments. As an example, Germany has one of the biggest aging populations in Europe, currently having more than 22% aged 65 years or older in 2024. Consequently, these demographic transitions will lead to an increase in the demand for early detection of arrhythmias and home-based cardiac monitoring solutions.

Also, national health systems are beginning to promote integration with public health digital systems and governmental action, regulatory factors, are enacting uptake of mobile telemetry solutions. Lastly, while reimbursement policies differ from country to country, I expect increased government funding in digital health will create growth for the region.

Latin America and the Middle East & Africa (MEA) market is experiencing moderate growth with increasing healthcare investments, advancements in diagnostic infrastructure, and enhanced focus on cardiovascular health. Countries such as Brazil, Mexico, South Africa, and the UAE are making investments in telemedicine platforms and wearable technologies as part of a wider digital health strategy.

Latin America has also seen private healthcare providers look to mobile telemetry for more portability in care, allowing remote management of high-risk cardiac patients. However, economic inequalities, limits in reimbursement, and access to advanced medical technology in rural and underserved areas will continue to inhibit market growth. Nonetheless, increased awareness and analytical partnerships with global medtech companies may present growth opportunities in the coming years.

The market was valued at USD 1.2 billion in 2024.

The market is projected to grow at a CAGR of 8.1% from 2025 to 2033.

The lead- based mobile cardiac telemetry hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include iRhythm Technologies (Philips), BioTelemetry, Inc. (Philips) and Biotricity, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Mobile Cardiac Telemetry Systems Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Mobile Cardiac Telemetry Systems Market, By End User

6.1 North America Mobile Cardiac Telemetry Systems Market, By Country

6.1.1 Mobile Cardiac Telemetry Systems Market, By Technology

6.1.2 Mobile Cardiac Telemetry Systems Market, By End User

6.2 U.S

6.2.1 Mobile Cardiac Telemetry Systems Market, By Technology

6.2.2 Mobile Cardiac Telemetry Systems Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping