Urinary Catheters Market

Urinary Catheters Market Share & Trends Analysis Report, By Product Type (Indwelling (Foley) Catheters, Intermittent Catheters, External Catheters), By Material Type (Silicone Catheters, PVC (Polyvinyl Chloride) Catheters, Latex Catheters, Other Materials), By Application (Urinary Incontinence, Benign Prostatic Hyperplasia (BPH) & Prostate Surgeries, Spinal Cord Injury, Urinary Retention, General Surgery/Post-Surgical Care, Other Applications), By End-User (Hospitals & Clinics, Long-Term Care Facilities (LTCFs), Homecare Settings, Specialty Clinics, Ambulatory Surgical Centers (ASCs)) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

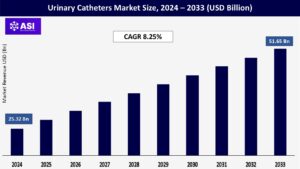

CAGR: 8.25%

Last Updated : November 8, 2025

The worldwide market for Urinary Catheters Market was valued at approximately USD 25.32 billion in 2024 and is projected to reach USD 51.65 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 8.25% during the forecast period of 2025–2033.

The urinary catheters market is an important part of the wider medical devices sector and is expected to grow consistently between 2024 and 2033. This steady rise is being driven by factors such as the increasing prevalence of urinary disorders, a growing elderly population, and advances in catheter design and materials. However, the market also faces challenges, including the risk of infections associated with catheter use and the availability of alternative treatments. At the same time, there are promising opportunities, particularly in emerging economies where healthcare infrastructure is expanding and awareness about urinary health is improving. Several major companies play a central role in shaping this landscape by developing innovative products and strengthening their global presence.

As the global population continues to age, more people are becoming vulnerable to a range of urological issues. Older adults are especially prone to conditions like urinary incontinence, benign prostatic hyperplasia (BPH), urinary retention, and chronic kidney disease. Managing these problems often requires the use of catheters, making them an essential tool in caring for aging patients. In addition, aging increases the likelihood of developing chronic diseases such as diabetes, neurological disorders like Parkinson’s or multiple sclerosis, and spinal cord injuries. These conditions can cause bladder dysfunction, creating a need for either long-term or intermittent catheter use to help patients maintain comfort, dignity, and quality of life.

Urinary incontinence (UI) is a common condition, especially among women often due to pregnancy, childbirth, and menopause as well as older adults. When other treatments don’t work, catheters become an important tool for managing it. Benign prostatic hyperplasia (BPH), the age-related enlargement of the prostate gland in men, is another major reason for catheter use, as it frequently causes urinary retention that requires catheterization for relief.

Urinary retention itself—when someone can’t fully empty their bladder can result from various causes, including neurological disorders, prostate problems, or complications after surgery. Spinal cord injuries and other neurological conditions often disrupt normal bladder control, making regular or long-term catheter use essential for many patients throughout their lives. While not strictly urinary, patients with end-stage kidney disease also rely on dialysis catheters, contributing to demand within the broader catheter market.

Finally, urinary tract infections (UTIs) and urethral blockages sometimes make catheterization necessary for effective drainage, treatment, or even diagnostic purposes.

One of the biggest challenges with urinary catheters is the risk of catheter-associated urinary tract infections (CAUTIs), which are actually the most common type of healthcare-associated infection. These infections can be serious, causing significant illness and even leading to deaths in some cases. Indwelling catheters, especially when used for long periods, create a direct pathway for bacteria to enter the bladder, making infections more likely. This risk is a major concern for both patients and healthcare providers.

CAUTIs can result in longer hospital stays, higher healthcare costs, and serious discomfort or complications for patients. Even though there have been advances in catheter technology—like antimicrobial and hydrophilic coatings designed to reduce infection risk—the threat of CAUTIs still leads many clinicians to use catheters only when absolutely necessary or to remove them as early as possible. Adding to the problem is the rise of antibiotic-resistant bacteria, which makes treating these infections even more difficult. This reality underscores the importance of prevention and can limit broader catheter adoption if effective safety measures aren’t consistently in place.

Using urinary catheters isn’t without its challenges. Insertion and removal can be painful experiences for patients, and having an indwelling catheter in place for a long time can cause ongoing discomfort, including bladder spasms and irritation. If a catheter isn’t inserted properly, or if there’s not enough lubrication, it can damage the urethra, sometimes leading to strictures (narrowing of the urethra) or even bleeding. Catheters can also irritate the bladder lining, triggering painful spasms that can be distressing for patients. Another common problem is blockages, which can happen if debris, blood clots, or mineral deposits build up inside the catheter. These blockages can stop urine from draining properly, causing retention and often requiring immediate medical care to fix.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Indwelling (Foley) Catheters Intermittent Catheters External Catheters |

| By Material Type |

Silicone Catheters PVC (Polyvinyl Chloride) Catheters Latex Catheters Other Materials |

| By Application |

Oncology (various cancer types) Central Nervous System (CNS) Disorders Immunology, Respiratory Diseases Genetic Diseases Infectious Diseases |

| By End User |

Hospitals & Clinics Long-Term Care Facilities (LTCFs) Homecare Settings Specialty Clinics Ambulatory Surgical Centers (ASCs) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Urinary Catheters Market is categorized by product type, by material, by application and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Each segment provide a comprehensive understanding of its dynamics and growth opportunities. The urinary catheters market can be segmented and analyzed based on several key factors, providing a more detailed understanding of its dynamics.

The urinary catheters market includes several key types, each with its own role in patient care. Indwelling (Foley) catheters are designed for long-term or continuous drainage and remain in the bladder with the help of an inflatable balloon. They come in sub-types like 2-way, 3-way, and 4-way catheters, differentiated by the number of channels for drainage, irrigation, and balloon inflation. Despite growing interest in alternatives, indwelling catheters still hold a substantial share of the market, largely because they’re widely used in hospitals for critical care and post-surgical patients.

In contrast, intermittent catheters are single-use devices meant for periodic bladder emptying and are removed after each use. These have become the largest and fastest-growing segment of the market, thanks to their lower infection risk compared to indwelling catheters and rising adoption for self-catheterization at home. Meanwhile, external catheters—non-invasive devices often used for male patients (like condom catheters) and increasingly for females—are also seeing rapid growth. Their appeal lies in being non-invasive, reducing the risk of catheter-associated urinary tract infections (CAUTIs), and offering greater comfort and convenience for people managing urinary incontinence.

Silicone catheters are especially popular because they’re highly biocompatible, flexible, and non-reactive, which makes them ideal for long-term use. They help reduce the risk of allergic reactions and irritation, and as a result, they currently lead the market in terms of material choice. PVC (polyvinyl chloride) catheters, on the other hand, are valued for being more affordable, making them a practical option in healthcare settings where cost is a major concern. Latex catheters are still in use but have been falling out of favor due to worries about latex allergies and the higher likelihood of causing irritation compared to silicone. There are also other specialized materials and composites being developed to meet specific needs, offering additional options for tailored patient care.

Urinary incontinence is the biggest area of use for urinary catheters, largely because it’s so common worldwide—especially among older adults. Another major application is in managing benign prostatic hyperplasia (BPH) and prostate surgeries. Many older men experience BPH, and catheterization is often necessary during and after these procedures. Patients with spinal cord injuries also rely on long-term catheterization to help manage bladder function. For those with urinary retention—when the bladder can’t empty naturally—catheters are essential for relief and care. Catheters are also widely used in general surgery and post-surgical care to track urine output and ensure proper bladder management. Beyond these, there are other important uses, including for conditions like spina bifida, multiple sclerosis, Parkinson’s disease, and various other urological disorders.

Hospitals are the biggest users of urinary catheters, since they handle a large number of surgeries, emergencies, and critically ill patients who need catheterization. Long-term care facilities are another important and growing segment, as the aging population means more residents with chronic conditions that require ongoing catheter management.

Homecare settings are also seeing strong growth. More people are choosing self-catheterization at home, thanks to user-friendly designs and technological improvements, as well as a broader shift toward more decentralized, patient-centered healthcare. Specialty clinics—like urology clinics—also drive demand for catheters by offering focused care for urinary conditions. Additionally, ambulatory surgical centers are important users too, given the increase in outpatient procedures where catheterization is often needed.

When you look at the urinary catheters market by region, you see a mix of trends and opportunities. North America and Europe are well-established, mature markets where catheter use is already widespread. In contrast, the Asia Pacific region is expected to see rapid growth, thanks to aging populations and ongoing improvements in healthcare systems. Latin America and the Middle East & Africa are also emerging as promising markets. As these regions continue to strengthen their healthcare infrastructure, they offer significant potential for future expansion.

North America especially the U.S. and Canada has the largest share of the global urinary catheters market, and this lead is expected to continue for the foreseeable future. Several factors drive this dominance. First, there’s a high rate of chronic and urological conditions like urinary incontinence, benign prostatic hyperplasia (BPH), bladder obstruction, and spinal cord injuries, all of which create consistent demand for catheterization. The region also benefits from advanced healthcare infrastructure, with well-equipped hospitals, easy access to specialized care, and strong diagnostic capabilities.

Favorable reimbursement policies—like Medicare and Medicaid covering intermittent catheter use—help make these products more accessible to patients. Technological innovation is another big factor. There’s high awareness and quick adoption of advanced catheter designs, such as coated or antimicrobial options that help reduce the risk of infections (CAUTIs). The region is also home to many leading catheter manufacturers, which fuels ongoing research, development, and competitive product offerings. One important trend is the growing preference for home care and self-catheterization. More patients are choosing intermittent catheters they can use themselves, boosting demand in this segment. Overall, the broader North American catheter market was valued at over USD 12.03 billion in 2024 and is expected to see steady growth in the coming years.

Europe is a major market for urinary catheters, second only to North America in terms of size. Several factors are driving this strong demand. One of the biggest is the region’s aging population, which is especially prone to urological issues and age-related bladder problems. The rising number of people with chronic kidney disease and other urinary disorders is also boosting the need for catheters.

Europe benefits from well-developed healthcare systems and public health initiatives aimed at effectively managing chronic conditions. Many countries also have supportive reimbursement policies that help patients access continence aids and self-catheterization kits more easily.

A notable trend in the region is the growing preference for intermittent catheters, which offer lower infection risks and allow patients greater independence. Germany, the UK, and France are among the leading contributors to this market’s growth. Looking ahead, the urinary catheters market in Europe is expected to reach around US$ 2.16 billion by 2030, growing at a steady rate of about 5.3% annually from 2025 to 2030.

The Asia Pacific region is expected to be the fastest-growing market for urinary catheters, with the highest projected growth rate over the coming years, making it an especially attractive area for investment. This rapid expansion is driven by several key factors. The region has a massive and aging population, particularly in countries like China, India, and Japan, leading to a sharp rise in urological conditions.

Healthcare infrastructure is improving quickly, with significant investments going into modernizing hospitals and clinics. Alongside this, rising disposable incomes and greater healthcare spending from both governments and the private sector are making advanced medical care more accessible. Awareness is also on the rise, with more patients and healthcare providers recognizing the benefits of modern catheterization techniques.

The region also faces a high incidence of conditions like spinal cord injuries, BPH, and urinary tract infections, which all drive demand for catheters. Additionally, the growth of medical tourism in countries like Thailand, India, and Singapore is boosting demand for advanced medical devices, including catheters. That said, the market isn’t without its challenges. Some areas still struggle with limited device availability, fragmented distribution channels, and inconsistent reimbursement policies. Despite these hurdles, there’s a strong focus on adopting new technologies, especially intermittent self-catheters (ISCs), which support patient independence. Overall, the Asia Pacific urinary catheters market is projected to reach around US$ 1.5 billion by 2031, growing at a healthy rate of 7.1% annually between 2021 and 2031.

The Middle East and Africa (MEA) region is expected to see solid growth in the urinary catheters market over the coming years, even though it’s starting from a smaller base compared to other regions. Several factors are contributing to this growth. There’s a rising incidence of urological diseases and emergencies, along with an expanding elderly population that needs more consistent urological care. Healthcare infrastructure is also improving steadily, thanks to increased investments from both governments and private companies aiming to expand and modernize medical facilities.

Awarness about urinary health is growing as well, with more patient education efforts and campaigns helping people understand their options for treatment. However, the region still faces some challenges. In certain areas, healthcare spending per person remains relatively low. There’s also a risk of catheter-associated infections (CAUTIs), partly due to variations in hygiene standards, and reimbursement systems for medical devices are often less developed.

Despite these hurdles, there’s a clear trend toward adopting intermittent catheters, which help lower infection risks and support patient independence. There’s also a stronger focus on infection prevention strategies overall. South Africa stands out as a particularly promising market within the region, showing high growth potential. Overall, the urinary catheters market in the Middle East and Africa is projected to reach about US$ 419.4 million by 2030, growing at an annual rate of 5.5% between 2025 and 2030.

The market was valued at USD 25.32 billion in 2024.

The market is projected to grow at a CAGR of 8.25% from 2025 to 2033.

urinary incontinence segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include Becton, Dickinson and Company, Boston Scientific Corporation, Coloplast A/S, Teleflex Incorporated, and Medtronic plc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Urinary Catheters Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Urinary Catheters Market, By Material Type

5.3 Urinary Catheters Market, By Application

5.4 Urinary Catheters Market, By End User

6.1 Urinary Catheters Market, By Country

6.1.1 Urinary Catheters Market, By Product Type

6.1.2 Urinary Catheters Market, By Material Type

6.1.3 Urinary Catheters Market, By Application

6.1.4 Urinary Catheters Market, By End User

6.2 U.S.

6.2.1 Urinary Catheters Market, By Product Type

6.2.2 Urinary Catheters Market, By Material Type

6.2.3 Urinary Catheters Market, By Application

6.2.4 Urinary Catheters Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping