Assisted Walking Devices Market

The Assisted Walking Devices Market Share & Trends Analysis Report, By Device Type (Canes, Crutches, Walkers, Gait Trainers, Powered Scooters & Wheelchairs) By Technology (Manual Devices, Powered Devices, Smart/Robotic Exoskeletons) By Application / End-User (Mobility Impairment, Elderly Care, Post-Surgical Recovery, Rehabilitation Centers, Homecare Settings, Hospitals & Clinics) By Distribution Channel (Offline Retail, Online Stores, Rental Services, Institutional Procurement) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

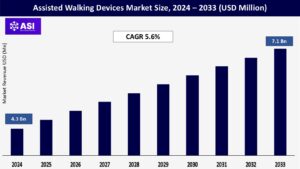

CAGR: 5.6%

Last Updated : August 29, 2025

The global Assisted Walking Devices Market was valued at approximately USD 4.3 billion in 2024 and is projected to reach USD 7.1 billion by 2033, growing at a CAGR of 5.6% during the forecast period (2025–2033).

Mobility aids are assistive walking devices that enable people who have temporary or permanent disabilities due to aging, injury, surgery, or neurological disorders to walk. Those devices include canes, crutches, walkers, gait trainers, and motorized systems used for mobility, such as electric scooters and electric wheelchairs. Mobility aids promote improved balance, stability, and independence, allowing people to engage in daily activities more easily and safely. Major drivers of demand shape the market, and include an increasing geriatric population across the globe, in addition to rising incidence of mobility-related conditions like arthritis, Parkinson’s, and stroke as well as greater numbers of orthopedic surgeries.

Accordingly, kinds of mobility aids have increased, with builds that are foldable, made with lighter materials, and have smart features that appeal to different populations. Also, the expansion of home healthcare and increased access to mobility aids via e-commerce and online availability, particularly in developing economies and countries, are contributing to the growth of the assisted walking devices market.

One of the key drivers for the growth of the global assisted walking devices market is the increasing number of seniors around the world. As people age, they are more likely to develop osteoarthritis, osteoporosis, Parkinson’s disease, and other musculoskeletal degeneration which leads to limited mobility.

The United Nations estimates that the global population age 60 years and older is projected to increase from 1.4 billion in 2023 to 2.1 billion people by 2050, with the majority of seniors being from Europe, North America, and East Asia. Seniors are using walkers, cane, motor scooters, and powered mobility which can help contribute to their independent movement and daily mobility.

For example, Japan is currently one of the oldest countries in the world and has recently seen a spike in rollator walker use among its elderly population. In the United States, the National Institute on Aging reports that almost 1 in 4 adults (aged 65+) use some sort of mobility device (e.g., cane, walker, scooter, etc.). As people around the world live longer, there will be a growing need for mobility assistance options at home, and in long-term care settings.

The ever-increasing volume of orthopedic surgeries and instances of trauma related injuries is another primary driver for market growth. Many knee and hip replacements, spinal surgeries, and fracture repairs typically have some degree of temporary or permanent mobility assisted required. The agency for healthcare research and quality (AHRQ) states that nationally over 790,000 total knee replacements, plus 450,000 hip replacements, happen annually.

The world health organization (WHO) states that every year in the world between 20 to 50 million people have non-fatal injuries, many of whom will need to use crutches or walkers for some period of rehabilitation. As there are more minimally invasive surgical techniques, patients are sent home earlier from hospitals and recuperating as outpatient and homecare.

This leads to an increase in the demand for lightweight, foldable, easy to use walking devices. As an example, Drive Medical and Medline have both seen increasing sales of crutches and foldable walkers with ergonomic features for patients requiring short term rehabilitation. This directly relates the implant device trends to what devices patients received during staging.

The relatively high cost of many assisted walking devices is arguably the main limitation inhibiting the growth of this market. Several of these technologically advanced devices such as powered wheelchairs, robotic exoskeletons, and smart walkers, have extremely high costs which can cause barriers for many potential users who could otherwise benefit from these devices, especially people living in developing countries and low-income populations.

Most advanced devices have high initial purchase costs that range into the thousands of dollars, which makes it impossible for many individuals to purchase without significant assistance. Additionally, most devices need ongoing support and thus can incur high long-term ownership costs (maintenance, battery replacement, rare repair costs) on top of initial purchase costs, and limited insurance coverage and reimbursement in many areas can further exacerbate the expense to users. As a result, many people either delay their purchase of walking assistive devices or abandon their purchase altogether even when they need them for mobility independence.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Device Type |

Canes Crutches Walkers Gait Trainers Powered Scooters & Wheelchairs |

| By Technology |

Manual Devices Powered Devices Smart/Robotic Exoskeletons |

| By Application / End-User |

Mobility Impairment Elderly Care Post-Surgical Recovery Rehabilitation Centers Homecare Settings Hospitals & Clinics |

| By Distribution Channel |

Offline Retail Online Stores Rental Services Institutional Procurement |

| Key Players |

Drive Medical Medline Industries Invacare Corporation Rollz International Ekso Bionics Sunrise Medical Nova Medical Products Otto Bock Healthcare Pride Mobility Product |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The walkers segment leads the market from high usage share, with the elderly and patients recovering from surgery, and thus it accounted for the largest market share in terms of revenues in 2024. Rollator walkers account for most of the volumes, leveraging their ease of mobility, stability, and safety features, even for short distances. Canes accounted for the second largest segment, leveraging low mobility limitations, (desirable in portable products).

Generally, demand is especially strong and prevalent in lower income areas due primarily to price point and simplicity. Crutches are considered a key component of short-term mobility aids, especially post injury or for temporary orthopedic recovery. Forearm crutches are gaining popularity due to the ergonomic benefits associated with them.

Gait trainers are growing the fastest due to the increased usage in pediatric rehabilitation and neurological rehabilitation, in stroke and spinal cord injury cases, in particular. Companies have reportedly incorporated smart sensors to help gait correction and feedback, and this fact will likely help this segment gain market share as more and more providers differentiate offerings in the gait trainer market. Powered scooters & wheelchairs, while often considered separate categories from walking aids, do fit into a definition of walking aid.

Generally these devices serve users who have significant limitations on mobility and increasingly benefit from ever greater advancements in technology (i.e., lighter-weight materials, better batteries & stability, and improved & intelligent navigation), especially in high income countries.

In 2024, hospitals and clinics will remain the largest end-user in this supply chain and will represent the largest share of device distribution. The largest end-user will remain at the forefront of recommending walking aids during rehabilitation after surgery and after significant injury. Devices like walkers, crutches, and canes will frequently be handed out day-to-day upon release from an orthopedic procedure.

Homecare is advancing quickly, especially compared to nursing homes and assisted living, because of an aging population who prefer to age-in-place and recover at home. Growth is related to the growth of online channels and product configurations (essentially easier to use and foldable). The rehabilitation center is a necessary part of the care continuum, particularly for patients recovering from strokes, spinal procedure injury and other neurological events.

Rehabilitation centers are using assistive technology and have been incorporated with gait trainers, forearm crutches, and robotic devices for functional recovery. Elderly care facilities including nursing homes and assisted living are a constant user group of robust devices that are easy to use and require consumers to use safer modes of transport when performing ambulation care.

Post-surgical recovery and management of mobility impairment also represents a major area specifically for patients recovering from knee surgery, hip surgery and spine surgery. Management of mobility impairment also includes chronic conditions including Parkinson’s and arthritis that are labels driving very consistent long-term demand for supportive devices in all areas of care.

The manual devices category is the largest share of the market because of the ubiquity of the traditional or non-powered equipment, specifically canes, crutches and walkers, as a mobility solution. Manual equipment is generally less expensive, easier to use, and more broadly available for short- or long-term mobility use by all populations.

The use of manual devices also remains popular due to their ease-of-use and lack of mechanical or electronic components, and these devices are more available and used by low- and middle-income populations. Powered transport equipment, such as power scooters and battery powered wheelchairs, is coming into greater use for those with a severe mobility impairment who require little exertion. Progress is primarily seen in high-income markets, where the healthcare systems and insurance programs provide some reimbursements.

An emerging area of powered devices is smart / robotic exoskeletons, driven largely by electronic advances in artificial intelligence, sensors, and biomechanics. Smart / robotic exoskeletons are still emerging technology, and while they remain in the experimental or early adoption stage, they have been used in rehabilitation centers and advanced care facilities to assist patients with spinal cord injuries, strokes or neurodegenerative disorders.

Robotic exoskeletons are expected to see more widespread use as their costs decrease and functionality improves. Together, the advancements in technology are growing user independence, improving dynamic support, and broadening the scope of walking support.

Offline retail will continue to dominate the assisted walking devices market, particularly given the importance of in-person fittings, product trials, and professional consultation. The primary offline channels for assisted walking devices are medical supply stores, hospitals, and rehabilitation centers, which are especially important for devices like crutches, walkers, and powered wheelchairs.

Patients are provided with these devices in the post-treatment package, thereby reinforcing offline retail as the bulk of the segment. Although offline retail will continue to dominate the market, online stores are anticipated to grow the fastest. With an increase in the availability of Internet, purchase through e-commerce, and home delivery/dropshippping convenience, online sales will continue to quickly grow.

Additionally, consumers now can quickly compare brands, features, and prices with online channels. This is especially true for home care users and caregivers. Lightweight and foldable products like canes and rollator walkers are very well-suited to be sold online. Market rental services are also an emerging, but small, distribution channel, especially for patients recovering from surgery or injury with a short-term need for mobility.

There are often rental packages for crutches, walkers, or scooters offered by hospitals, clinics or through specialty vendors. Finally there is institutional procurement of walking aids, mainly by senior living facilities, rehabilitation centers, or public sector healthcare (government) systems which also plays a role (and considerable cost savings) in the wholesale purchase of walking aids. This market segment is expected to grow steadily with novices funding for public health infrastructure.

North America has the largest market share (approximately 39.5%) in 2024. The market in this region is influenced by a well-established healthcare infrastructure, large aging population, and high awareness of mobility-related health issues.

The United States is the largest contributor to this market and has the highest utilization with over 24% of its population 65 years and older using mobility aids such as walkers and canes. The United States also has rapidly growing technologically advanced devices and insurance reimbursement policies that continue to strengthen the market growth.

Europe’s share of the market is substantial and is influenced by aging population and a broad healthcare system in countries such as Germany, France, the UK, Italy etc. which continue to grow. In areas such as Germany, an estimated 22% of persons 65 years and older use walking aids. This market is supported by growing geriatric care services and countries taking government initiatives to work to increase mobility as well as to prevent falls, which continues to foster continued market growth.

The Asia-Pacific region is expected to grow at the highest rate, estimated at a CAGR of 7.5% during the forecast period. Rapid urbanization, rising healthcare expenditures, and increased geriatric population in countries such as China, Japan, and India, facilitate the request for assisted walking devices. The rise in awareness for homecare and rehabilitation has also contributed to the rise in growth for assisted walking devices.

Latin America and Middle East & Africa are expected to grow moderately given increasing healthcare infrastructure and government emphasis on caring for the elderly sector of health. However, challenges such as Income inequality, limited access to complex healthcare products, and limited knowledge has prevented faster market growth.

The market was valued at USD 4.3 billion in 2024.

The market is projected to grow at a CAGR of 5.6% from 2025 to 2033.

The Walkers hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Drive Medical, Medline Industries and Invacare Corporation

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 The Assisted Walking Devices Market, By Device Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 The Assisted Walking Devices Market, By Technology

5.3 The Assisted Walking Devices, By Application / End-User

5.4 The Assisted Walking Devices, By Distribution Channel

6.1 North America The Assisted Walking Devices Market, By Country

6.1.1 The Assisted Walking Devices Market, By Device Type

6.1.2 The Assisted Walking Devices Market, By Technology

6.1.3 The Assisted Walking Devices Market, By Application / End-User

6.1.4 The Assisted Walking Devices Market, By Distribution Channel

6.2 U.S.

6.2.1 The Assisted Walking Devices Market, By Device Type

6.2.2 The Assisted Walking Devices Market, By Technology

6.2.3 The Assisted Walking Devices Market, By Application / End-User

6.2.4 The Assisted Walking Devices Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping