Intramedullary Nail Market

Intramedullary Nail Market Share and Trend Analysis, By Technology Type (Stainless Steel Nails, Titanium Alloy Nails, Polymer Coated Nails), By Application (Femoral Fractures, Tibial Fractures, Humeral Fractures, Pediatric Fractures), By End User (Hospitals, Ambulatory Surgical Centres, Rehabilitation Centres & Orthopaedic Clinics) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.5%

Last Updated : November 8, 2025

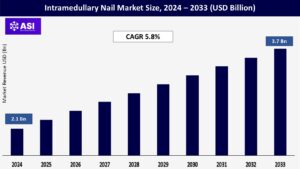

The global intramedullary nail market size was valued at USD 2.1 billion in 2024 and is projected to reach USD 3.7 billion by 2033, expanding at a compound annual growth rate CAGR of 5.8% during the forecast period (2025 – 2033).

The intramedullary nail is a basic orthopaedic device designed to stabilize long bone fractures by being inserted into the medullary canal. Mainly made of medical-grade stainless steel or titanium alloys, it gives important axial and rotatory stability, thus facilitating the early mobilization of patients and bearing of loads. Its indications include femoral and tibial shaft fractures, complicated humeral reconstructions, and increasing use in pediatric and geriatric trauma cohorts as result of new designs.

Ongoing developments in nail shape, locking systems, and bioactive surface coatings increase fixation strength, enhance osseointegration, and reduce infection risk. The simultaneous implementation of image-guided surgical methods and minimally invasive insertion systems reduces soft tissue destruction, fosters faster wound healing, and enhances clinical success. The market growth is also driven by the increasing prevalence of high-energy trauma, growing geriatric population at risk of osteoporosis fractures, and growing interest in effective solutions that enable quick functional recovery.

The worldwide proliferation in traumatic fractures, stimulated mainly by mounting road traffic accidents and involvement in high-impact sports, is a leading spur for the intramedullary nail market. Such injuries commonly lead to complex long bone fractures needing strong internal fixation. Intramedullary nails are increasingly the solution to mid-shaft fractures because of their inherent biomechanical benefits, with improved load-sharing and structural performance compared to plates or external fixators. Their minimally invasive insertion method reduces soft tissue damage, resulting in less postoperative pain, lower infection rates, and shorter hospital stays both addressing clinical needs and healthcare cost-containment pressures.

Increased recognition among orthopedic surgeons for the critical importance of early weight-bearing for patient rehabilitation and bone healing further drives adoption. Concurrently, expanding access to advanced trauma care in developing regions, fueled by government investments in healthcare infrastructure and the establishment of specialized trauma centers, significantly broadens the patient base eligible for this treatment. These converging factors rising trauma prevalence, clinical efficacy, economic efficiency, surgical preference, and improved healthcare access collectively establish a strong foundation for sustained market growth in the foreseeable decade.

Ongoing innovation in implant design and biomaterials is structurally transforming the intramedullary nail environment. State-of-the-art technologies now feature tapered geometries, multi-axial and distant-cortical locking mechanisms, and body-contoured curvatures, optimizing fit across varied patient anatomies and minimizing iatrogenic hazards such as malalignment and iatrogenic fracture. Surface engineering advances are pivotal; plasma-sprayed titanium and hydroxyapatite coatings significantly enhance osseointegration by greatly expanding the speed at which direct bone-implant bonding occurs and yielding enhanced long-term stability. Antimicrobial iodine or silver coatings are on the rise to address periprosthetic joint infection, a significant complication.

Possibly most revolutionary is patient-specific instrumentation (PSI), using precise preoperative CT imaging and 3D printing to create personalized jigs and sometimes even customized nails. Such accuracy maximizes implant placement and alignment with individual bone anatomy, extending indications to more challenging fractures and osteoporotic bone. These advances in technology—ranging from intelligent design, bioactive surfaces, and customized manufacturing—do not only enhance fixation stability and lower rates of complications but also increase surgeon confidence in the procedure, thus fueling wider clinical use across varied patient populations and fracture patterns.

Substantial economic impediments bar the widespread adoption of intramedullary nailing in spite of its benefits clinically. The process comes at a high price, fueled by costly implants (most frequently premium titanium alloys), customized insertion tools, and necessary advanced intraoperative imaging such as fluoroscopy. The aggregate cost makes the process unaffordable in lower- and middle-income countries with limited healthcare budgets and underdeveloped trauma surgery infrastructure. Reimbursement policies are a significant challenge with extreme inconsistencies: national health services often rigorously implement cost-containment, postponing or limiting coverage for newer systems, while private insurers apply coverage limits or onerous prior authorization for cutting-edge devices, commonly labeling them non-essential.

This uncertainty in reimbursement compels hospitals and surgical centers to value fiscal constraints over best care for the patients, often delaying or prohibiting the adoption of the next-generation systems. Therefore, while their potential benefits in outcomes and efficiency, further market extension is constricted. Until market benchmarks become more widely available, standardized reimbursement systems are developed that realize the long-term value (fewer complications, quicker recovery) of such implants, and become manufacturing breakthroughs delivering cheaper offerings without sacrificing quality, ongoing price responsiveness among payers and providers will remain a significant drag, especially in developing economies and cost-conscious settings.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Stainless Steel Nails Titanium Alloy Nails Polymer-Coated Nails

|

| By Application |

Femoral Fractures Tibial Fractures Humeral Fractures Pediatric Fractures

|

| By End User |

Hospitals Ambulatory Surgical Centres Rehabilitation Centres & Orthopaedic Clinics

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The intramedullary nail market segments mainly on core material and surface technology. Stainless steel nails maintain widespread application through established mechanical strength and reduced manufacturing expense, thus being sensible for common fracture cases in cost-conscious institutions. Yet, their elevated nickel content poses greater biocompatibility issues than that of alternatives. Titanium alloy nails are the high-end category, with higher prices commensurate with stronger corrosion resistance and an elastic modulus more similar to human bone—minimizing stress shielding threats and favoring natural load transfer. Their increased osseointegration capability is imperative for osteoporotic or difficult fractures.

Polymer-coated nails constitute a specialized category: antibiotic-impregnated types (e.g., gentamicin-eluting) offer localized infection prophylaxis with open fractures or contaminated wounds, while keeping systemic antibiotic exposure and biofilm development to a minimum. Bioactive hydroxyapatite coatings enhance bone-implant integration in low-quality bone. New biodegradable polymer composites such as polylactic acid–magnesium hybrids are designed to avoid secondary removal procedures without compromising mechanical strength during healing. These material technologies directly affect clinical choices; surgeons weigh fracture severity, patient comorbidities (e.g., osteoporosis, diabetes), risk of infection, and expense when choosing implants. R&D continues to target smart coatings with dual antibiotic/osteogenic agents and resorbable metals, broadening product lines further.

Femoral nails lead to procedure volumes due to aging populations at risk of low-energy hip fractures (intertrochanteric/subtrochanteric) and high-energy femoral shaft fractures. Their overall designs focus on proximal/distal locking stability with early weight-bearing. Tibial nails tackle trauma from motor vehicle accidents or sporting injuries, with specialized versions for open fractures (e.g., minimized anterior bow) maintaining vascularity and soft tissues. Humeral nails, although rarer, treat difficult shaft nonunions or multi-fragment proximal fractures where plating is not effective, particularly in osteoporotic bone that necessitates angular stable locking.

Pediatric-specific nails have smaller diameters, elastic titanium constructs, and partial threading to prevent damage to the physis in growing skeletons. Indications extend beyond acute trauma to include reconstructive orthopedics: reconstructive osteotomies for malunions (e.g., tibial deformity), limb lengthening with extendable nails, and nonunion revisions with augmented dynamization techniques. Surgeon preference is regional—humeral nailing experiences greater utilization in Europe compared to North America—due to training and outcome data variations. The system’s utility further extends into oncology (stabilization of pathologic fractures) and veterinary orthopedics, solidifying its place along the continuum of care.

Hospitals, especially Level I trauma centers, account for most nail consumption due to 24/7 emergency services, high-volume fracture treated in part by availability of imaging/OR resources within the hospital. They emphasize systems with intraoperative adaptability (e.g., multi-planar locking) for use in polytrauma patients. Ambulatory Surgery Centers (ASCs) are quickly embracing nailing for uneventful fractures (e.g., isolated tibial shaft) through the use of minimally invasive strategies that facilitate same-day discharge. ASCs prefer cost-effective, efficient sets with reusable instruments to optimize profitability. Specialty orthopedic practices and rehabilitation clinics indirectly affect device choice via postoperative protocols; nails allowing for early joint motion (e.g., proximal humeral designs that allow for shoulder pendulum exercises) become popular choices.

Academic hospitals lead innovation adoption, testing patient-specific 3D-printed guides or bioactive implants, whereas community hospitals seek reliability and ease of use. Group Purchasing Organizations (GPOs) exert pressure on price, frequently standardizing contracts to stainless steel systems with the exception of high-end indications. In developing economies, trauma units and charity hospitals depend on subsidized or donated stainless-steel nails because of financial limitations. This heterogeneity forces producers to customize business approaches: high-end tech for academic institutions, value-engineered packs for ASCs/GPOs, and long-lasting designs for public hospitals with high volumes.

North America has the biggest market share with substantial orthopedic infrastructure and high per-capita healthcare expenditures. Proven pathways of reimbursement and surgeon comfort with early uptake of premium technology (e.g., titanium nails, patient-specific guides) maintain high utilization rates. Level I trauma centers and specialty ASCs consistently utilize advanced locking systems for high-fractures on a regular basis. Regulatory encouragement of innovation and good payment models for outpatient fracture care further solidify its position of leadership. Yet, hospital procurement organizations and GPO pricing pressures moderate ultra-premium segment growth, concentrating demand on clinically established, value-optimized systems in non-academic environments.

Europe registers constant growth, buoyed by national health systems purchasing standardized trauma networks and aging patient populations with need for fracture care. Centralized buying by agencies such as the NHS encourages cost-efficient stainless-steel nails for uncomplicated cases, whereas Germany and France are leaders in take-up of bioactive-coated titanium systems for osteoporotic fractures. Strict EU MDR ensures higher production costs but guarantees implant quality and safety. There is regional variation: Northern Europe emphasizes same-day ASC procedures using reduced-facility nail kits, whereas Southern/Eastern markets depend increasingly on in-hospital care. Cross-border training programs standardize surgical procedure, increasing overall usage.

The Asia Pacific region has the most growth potential with increasing road traffic injuries, growing hospital infrastructure, and increasing medical tourism in Thailand/India. Stainless steel nail affordability is fueled by local production in China, providing wider access in tier-2/3 cities. Japan and Australia dominate premium segment uptake with demographically driven aged populations and a preference for titanium humeral/femoral systems. Government schemes in Vietnam and Indonesia subsidize implants for state-run hospitals, whereas private chains approach medical tourists with same-day nailing protocols. Challenges cover fragmented reimbursement and unequal surgeon training, although multinational collaborations (e.g., orthopaedic skills transfer programs) speed standardized technique dissemination.

Expansion in Latin America and MEA is hampered by tight healthcare budgets and infrastructure deficits. Brazil and Mexico dominate LATAM with public-private trauma center alliances utilizing mid-range stainless systems. GCC countries (UAE, Saudi) utilize high disposable incomes for high-end imports in private hospitals, while Africa depends on donated implants and NGO-aided programs. Main hindrances are currency fluctuations affecting import prices and unpredictable reimbursement. Efforts such as Mexico’s Seguro Popular expansion and Africa’s surgical camps enhance access. Local assembly centers in South Africa and Turkey look to save costs and target volume growth in trauma-naive markets.

The global Intramedullary Nail Market was valued at USD 2.1 billion in 2024.

The market is projected to grow at a CAGR of 5.8 % from 2025 to 2033.

Femoral hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Stryker Corporation, DePuy Synthes (Johnson & Johnson), Zimmer Biomet, Smith & Nephew, Wright Medical Group.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Intramedullary Nail Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Intramedullary Nail Market, By Application

5.3 Intramedullary Nail Market, By End User

6.1 North America Intramedullary Nail Market , By Country

6.1.1 Intramedullary Nail Market, By Technology

6.1.2 Intramedullary Nail Market, By Application

6.1.3 Intramedullary Nail Market, By End User

6.2 U.S.

6.2.1 Intramedullary Nail Market, By Technology

6.2.2 Intramedullary Nail Market, By Application

6.2.3 Intramedullary Nail Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping