Intrauterine Contraceptive Devices Market

Intrauterine Contraceptive Devices Market Share and Trend Analysis, By Technology (Hormonal IUCDs, Copper IUCDs, Emerging Technologies), By Application (Contraception, Therapeutic Applications, Emergency Contraception), By End Users (Hospitals, Gynecology Clinics, Community Health Centers) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2026–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 6.5%

Last Updated : November 8, 2025

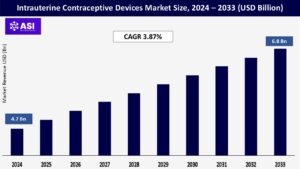

The global intrauterine contraceptive devices market size was valued at USD 4.7 billion in 2024 and is projected to reach USD 6.8 billion by 2033, expanding at a compound annual growth rate CAGR of 3.87% during the forecast period (2025 – 2033).

Intrauterine contraceptive devices (IUCDs) refer to thin, flexible medical implants inserted within the uterus for pregnancy prevention. Both of these T-shaped devices are classified into two groups: hormonal IUCDs, which release progestin continuously to thicken cervical mucus and inhibit ovulation, and copper IUCDs, which induce an inflammatory response harmful to sperm. Both are extremely effective (>99%), long-lasting (3–10 years), and reversible with no daily user involvement. Hormonal IUCDs such as Mirena are also used to treat heavy menstrual bleeding, endometriosis, and uterine fibroids.

Healthcare professionals – such as gynecologists, family doctors, and trained nurses – insert IUCDs in outpatient facilities such as clinics or hospitals during short procedures. Their popularity is due to low maintenance, long-term cost-effectiveness, and appropriateness for a wide range of populations, including adolescents and postpartum women. Growing worldwide emphasis on women’s reproductive autonomy and government-supported family planning programs further make IUCDs essential tools in contemporary healthcare systems.

The worldwide uptick in demand for long-acting reversible contraceptives (LARCs) such as IUCDs is transforming reproductive healthcare. They offer 3–10 years of pregnancy avoidance with more than 99% effectiveness, removing daily user effort imposed by pills or patches. Their “fit-and-forget” style radically reduces unintended pregnancies, particularly among teenagers and childless women. Leading medical organizations, such as the American College of Obstetricians and Gynecologists, now approve IUCDs as first-line contraception for teenagers, accelerating uptake in North America and Europe.

Post-pandemic, postponed pregnancies and limited clinic access pushed demand higher. In the US, use surged to 10.3% of reproductive-age women in 2018. Analogous patterns appeared in the UK and Australia, where public health programs endorse LARCs as frugal options. In poorer countries, organizations such as MSI Reproductive Choices promote demand through provider training in inserting IUCDs. The adaptability of the devices controlling heavy bleeding while avoiding pregnancy increases their popularity worldwide. As the model of health care shifts toward cost-effective, low-tech practice, IUCDs emerge as stalwart implements in family planning programs from Brazil to India.

Government-sponsored family planning programs globally are promoting IUCD use at an accelerated rate. International bodies such as UNFPA alert that 47 million women almost lost access to contraceptives in the time of COVID-19, at risk for 7 million unwanted pregnancies calling for immediate policy intervention. Subsidized IUCD programs in developing economies address population growth and maternal deaths. India’s National Family Welfare Programme provides free insertion in 20,000 government hospitals, reaching 8 million women every year. Brazil’s “SUS” healthcare system offers hormonal IUCDs at no cost in urban health centers.

Wealthy nations employ insurance schemes: America’s Medicaid insures 15 million low-income women for IUCDs, while France pays 100% of expenses. Global partnerships such as FP2020 invest in IUCD training for Nigerian and Pakistani nurses, where device usage increased 40% since 2020. Campaigns also overcome cultural barriers Bangladesh’s “National IUCD Week” teaches rural villages through mobile clinics. These interventions fill key gaps: In the 24% of women in sub-Saharan Africa not using modern contraception, Ghana’s free distribution of IUCDs in 900 facilities raised use by 31% in 2023. Such efforts make IUCDs a key tool in UN Sustainable Development Goals for reproductive health.

The high initial cost of IUCDs greatly restricts access, especially in poorer areas. Hormonal IUCDs have price tags of $500–$1,300 in the United States for the device and insertion a barrier for uninsured women. Even copper IUCDs ($50–$200) are out of reach for millions in developing economies. These economic barriers converge with long-standing cultural myths. Misinformation perpetually associates IUCDs with infertility, pelvic infection, or abortion, when decades of clinical experience have established their safety. In conservative communities, religious beliefs often clash with contraceptive use, while poor sexual education fuels fear.

For example, across sub-Saharan Africa where 24% of women lack access to modern contraception rumors suggest IUCDs “migrate to the heart” or cause cancer. In rural India, providers indicate women removing devices prematurely because family members pressure them as “unnatural.” Healthcare deserts exacerbate the issue: 60% of Nigerian districts have no trained IUCD insertion personnel. Conquering these challenges requires multi-faceted solutions: tiered pricing (such as Medicines360’s sliding-scale model), training community health workers, and myth-busting campaigns co-designed with local leaders. Unless cost and culture are addressed, universal access to contraceptives eludes us.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Technology |

Hormonal IUCDs Copper IUCDs Emerging Technologies

|

| By Application |

Contraception Therapeutic Applications Emergency Contraception

|

| By End User |

Hospitals Gynecology Clinics Community Health Centers

|

| Key Players |

Bayer AG CooperSurgical Inc. Medicines360 Teva Pharmaceuticals AbbVie Inc. (via Allergan) Merck & Co. Eurogine S.L. HLL Lifecare Limited Pregna International Limited Ocon Medical Ltd. |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The intrauterine contraceptive devices market segments mainly into hormonal and copper-based technologies, both catering to different patient requirements. Hormonal IUCDs deliver controlled doses of progestin in order to inhibit ovulation and thicken cervical mucus, providing two-in-one benefits for contraception and menstrual disorder control. The devices minimize heavy bleeding and cramping, and hence are favored for women with gynecological conditions. Copper IUCDs initiate a localized inflammatory reaction that immobilizes sperm, giving hormone-free pregnancy protection.

Although cheaper, copper counterparts experience adoption hurdles through possible side effects such as heightened cramping. New developments overcome past constraints: frameless configurations reduce expulsion risk for active users, and bioresorbable materials dispense with removal surgery. New smart technologies couple health monitoring sensors to monitor physiological changes. Developed economies increasingly favor hormonal solutions for their therapeutic benefits, while copper technology remains applicable to cost-conscious areas. Material technology improvements continue to increase biocompatibility and patient comfort in both segments.

Contraception is the leading application worldwide, fueled by need for effective, long-term birth control measures. Therapeutic uses outside pregnancy prevention show strong growth, especially in mature health systems. Hormonal IUCDs treat conditions such as menorrhagia well by cutting menstrual blood loss significantly in months following insertion. They are also first-line therapies for pain caused by endometriosis and uterine fibroids, reducing lesion size and enhancing quality of life.

Copper types occupy a valuable niche as emergency contraception when inserted shortly after unprotected sex, providing better efficacy than oral options. Developing countries focus on core contraceptive function owing to family planning policies, whereas developed countries increasingly use non-contraceptive effects for symptom relief during perimenopause. Expanded indications are now reflected in regulatory approvals, such as endometrial protection with estrogen therapy. Diversification of the indications increases clinical utility throughout reproductive life, making IUCDs general-purpose tools in women’s health rather than single-purpose contraceptives.

Hospitals form the largest end-user segment, conducting most first-time insertions owing to surgical capabilities, emergency care capacity, and insurance coordination services. Obstetrics gynecology clinics receive patients undergoing expert consultation for complicated cases, such as nulliparous patients and those in need of therapeutic applications, with individualized follow-up treatment. Community health centers are essential access points in underserved areas through partnerships with NGOs and government initiatives, although availability issues with devices persist.

Post-pandemic integration of telemedicine simplifies pre-insertion consultations in all settings, decreasing waiting times and enhancing patient education. Gaps remain critical where skilled providers are limited, especially in rural South Asia and Africa. Task-shifting programs—educating nurses and midwives to conduct insertions—prove successful in increasing coverage where physician access is limited. Urban clinics increasingly integrate IUCD services into primary care, with mobile health units bringing access to distant populations. Each setting faces distinct operational hurdles, from hospital reimbursement complexities to clinic supply chain limitations and community center staffing shortages.

Demand is strong, spearheaded by widespread awareness and health-polite support. Medicaid coverage facilitates greater access across the income spectrum, as clinical guidelines also actively recommend IUCDs for younger generations. Regional adoption is led by the United States through managed reproductive care programs. Canada continues to have its challenges from healthcare backlogs but is demonstrating steady recovery in urban areas. Professional medical organizations continue to recommend long-acting devices as first-line contraception, supporting market maturity.

Strong public health systems and active family planning structures maintain leadership. Germany and France lead the adoption through streamlined reimbursement channels and doctor training programs. Population trends towards later conception and reduced family sizes increase the demand. Investments are directed towards tomorrow’s generation biocompatible design to reduce side effects. Harmonization of regulation within the EU allows similar access, though Eastern Europe is behind in terms of service infrastructure.

Growth accelerates, sustained by Indian and Chinese government-subsidized programs for improving maternal health. Japan’s aging population increasingly deploys therapeutic uses in managing perimenopausal care. Demographic changes towards postponed marriages and urbanization fuel contraceptive acceptance. Grassroots educational campaigns slowly eliminate traditional stigmas, though outreach is irregular in rural areas. Regional producers increasingly design cost-optimized devices for regional markets.

Brazil and South Africa are growth centers by urban clinic networks, but religious and cultural barriers impede wider adoption. Acute shortages of trained providers and stable supply chains make sub-Saharan Africa increasingly vulnerable to unmet needs. Mobile health programs are promising in Kenya and Ghana. Traditional beliefs frequently trump clinical evidence, requiring education at the community level. Restrictive healthcare budgets place emphasis on basic care at the expense of contraceptive services.

The global intrauterine contraceptive devices market was valued at USD 4.7 billion in 2024.

The intrauterine contraceptive devices market is projected to grow at a CAGR of 3.87 % from 2025 to 2033.

The Hormonal IUCDs hold the largest intrauterine contraceptive devices market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Bayer AG, CooperSurgical Inc., Medicines360, Teva Pharmaceuticals, AbbVie Inc., Merck & Co., Eurogine S.L., HLL Lifecare Limited, Pregna International Limited, and Ocon Medical Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Intrauterine Contraceptive Devices Market, By Technology

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Intrauterine Contraceptive Devices Market, By Application

5.3 Intrauterine Contraceptive Devices Market, By End User

6.1 North America Intrauterine Contraceptive Devices Market, By Country

6.1.1 Intrauterine Contraceptive Devices Market, By Technology

6.1.2 Intrauterine Contraceptive Devices Market, By Application

6.1.3 Intrauterine Contraceptive Devices Market, By End User

6.2 U.S.

6.2.1 Intrauterine Contraceptive Devices Market, By Technology

6.2.2 Intrauterine Contraceptive Devices Market, By Application

6.2.3 Intrauterine Contraceptive Devices Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping