Dental Radiography Market

Dental Radiography Market Share & Trends Analysis Report, By Product Type (Intraoral Radiography Systems, Extraoral Radiography Systems) By Application (Diagnostic Applications, Cosmetic Dentistry, Forensic Applications, Therapeutic Applications) By End User (Dental Hospitals & Clinics, Dental Diagnostic Centers, Academic & Research Institutes) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

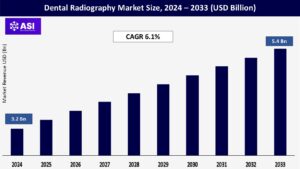

CAGR: 6.1%

Last Updated : February 25, 2026

The global Dental Radiography Market was valued at approximately USD 3.2 billion in 2024 and is projected to reach USD 5.4 billion by 2033, growing at a CAGR of 6.1% during the forecast period (2025–2033).

Dental radiography consists of imaging options that use imaging to assess health to obtain images of teeth, bone, and surrounding soft tissues. These imaging tools – intraoral, extraoral, and cone-beam computed tomography (CBCT) systems. These imaging tools assist in the identification of tooth decay, bone loss, abscesses, and impacted teeth. Dental radiographs are an important part of treatment planning in orthodontics (and before treatment begins), implants, and endodontic procedures, and this category is expected to increase as the population ages.

The increase of this market is driven by the increase in the incidence of dental disorders and disease, increased demand for cosmetic and preventive medicine, advances in digital imaging technology, and increased number of (global) diagnostic centers / dental clinics. In addition, government initiatives to focus on oral health, and increased adoption of 3D imaging via CBCT systems is driving demand in this market area.

The rise in dental conditions, such as tooth decay, periodontal disease, impacted teeth, and dental abscesses among populations on a global scale, is impacting and fuelling the growth of the dental radiography market. According to the Global Burden of Disease Study 2019, oral diseases affect nearly 3.5 billion people globally, and the most prevalent condition in the world is untreated dental caries (tooth decay), in permanent teeth.

Population growth and ageing, particularly in low- and middle-income countries, has led to increased prevalence of oral disease, often associated with high sugar diets and poor oral hygiene, which in turn has resulted in a substantial movement towards preventive dental care, as timely and accurate diagnosis is essential. Dental radiography tools, especially digital intraoral and cone beam computed tomography (CBCT) providing dental imaging, assist in early identification of cavities, bone loss, tumors and other abnormalities that may not present during a clinical clinical examination.

As an example, in April 2023, the Indian Dental Association announced a national campaign encouraging stakeholders to implement digital dental checkups, in turn increasing the rate of adoption of radiography tools into routine care. Similarly, private chain dental clinics, such as Aspen Dental (U.S.) and Clove Dental (India), are also directing access to diagnostic imaging during preventative care that will be packaged together with other products/services. The increasing focus on preventative oral health and wellness monitoring is driving the demand for dental radiography systems substantially.

Technological advances are continuing to unfold in the field of dental radiography. We have experienced a strong shift in radiographic technique from analog to digital imaging. Digital radiography provides enhanced imaging, less radiation, and faster imaging results. Digital intraoral sensors, portable X-ray units, and cone-beam computed tomography (CBCT) have changed the way clinicians visualize anatomy in dentistry and the use of 3D images for diagnosis and treatment planning.

One of the examples, Planmeca’s Viso CBCT takes it to the next level with its ultra-low-dose imaging and uniquely integrates artificial intelligence-based reconstruction algorithms that allow clinicians to produce ana-tomically correct diagnostic images of the patient with the lowest possible radiation doses.

Most recently, Dentsply Sirona has introduced to the market DS Core, a cloud-based artificial intelligence (AI) platform that works with Dentslpy Sirona’s digital radiography solutions to automatically analyze their dental images, identify potential issues, and house patient data in secure storage. All imaging solutions not only streamline diagnostic efficiency but also enhance effective communication with patients and increase rate of case acceptance.

One major barrier limiting the growth of the dental radiography market is the expense of more sophisticated imaging systems, especially the digital and 3D Cone-Beam Computational Tomography (CBCT) systems. Even though these systems provide better image quality with better radiation mitigation, and better diagnostic capabilities, the burden of needing to invest the majority of a year’s income of a middle-class person upfront (depending on the US dollar value from $30,000 to $100,000 for even one); then these systems require many yearly recurring costs as well for software upgrades, routine maintenance, staff training, and data storage continuing to add operational costs.

Now some of this purchasing model can be mitigated through banking systems, however, this high investment cost and associated expense for the majority is a limiting factor for many dental practitioners from purchasing. According to a report from the World Dental Federation (FDI) published in 2023, over 40% of clinics in developing countries still use analog X-ray systems primarily due to cost, and only being offered insufficient financial or support from the government in terms of wanting to digitize.

Moreover, not all advanced radiographic services are reimbursed in several public health care systems, making it difficult for defendants to convince themselves that it is worthwhile to purchase a new high end device designed to improve their practice.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Intraoral Radiography Systems Extraoral Radiography Systems |

| By Application |

Diagnostic Applications Cosmetic Dentistry Forensic Applications Therapeutic Applications |

| By End User |

Dental Hospitals & Clinics Dental Diagnostic Centers Academic & Research Institutes |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The largest market share in 2024 was represented by Intraoral Radiography Systems, which included the mounting usage of guided development for caries detection, bone level determination, and monitoring the condition of oral health overall. When considering intraoral types, the bitewing or periapical X-ray represents the most commonly detected form during typical dental exams and periodontal assessments.

As a result, they are directly influencing the overall revenue for intraoral radiography as an extensive portion of day-to-day practice involves bitewings, making them standard in general dentistry due to quick imaging times and lower radiation. The fastest-growing market segment is emitted by Cone-Beam Computed Tomography (CBCT) in detecting complex anatomical structures which will likely drive the adoption of 3D imaging in implant planning, endodontics and orthodontics.

The superior visualization of anatomical structures available using CBCT will refine the use of dental imaging in technically difficult procedures. For instance, dental implant surgery worldwide is on the rise which is likely to increase the demand for CBCT systems that can deliver the speed and precision afforded by dental imaging systems while targeting the areas of surgical exposure. Panoramic and cephalometric radiography systems will continue to grow steadily along with the added value of full mouth or full skeletal imaging necessary for orthodontics or maxillofacial surgery when determining comprehensive diagnosis and treatment plans.

Diagnostic applications are leading, with the market’s attention focusing on earlier detection of dental conditions, such as caries, periodontal issues, and impacted teeth. Most dental diagnostic appointments will have at least a bitewing and panoramic image taken for diagnosis of the teeth and surrounding anatomy.

Cosmetic dentistry is also emerging as a significant growth area, aided by increased consumer awareness and disposable income. Radiography is an important component of preprocedural planning for veneers, aligners, and whitening procedures. Forensic and therapeutic applications are small but growing steady segments of the dental imaging market, with dental imaging increasingly being incorporated into forensic investigations and post-surgical monitoring of patient healing.

Dental hospitals & clinics comprise more than 60% of the market in 2024, as they account for the largest number of participants in need of diagnostic imaging. More chain dental clinics have begun opening and investment in digital infrastructure has helped to increase adoption. Dental diagnostic centers are also on the rise, largely in urban areas, where stand-alone imaging centers predominantly offer specific services such as CBCT scans and cephalometric analyses, which is unique to orthodontists and oral surgeons.

Although the contribution of academic & research institutes to the market isn’t as substantial, they continue to play an essential role in developing new techniques/products, and educating dental professionals, which will likely lead to innovation and growth in the coming years.

With around 38 – 5 percent share of the market in 2024, North America is predicted to have the largest market. Increasing experience with the advances in the dental care infrastructure, the presence of early adopters of digital radiography, and the impetus of preventive oral healthcare have all contributed to its position. In North America, the United States leads with the use of digital intraoral sensors, CBCT systems, and real-world, AI-enabled diagnostics by a wide exposure and adoption in the private and public dental practice environment.

Based on a recent assessment by the American Dental Association (ADA), there are now over 85 percent of dental practices in the United States using digital X-ray systems. Factors such as insurance coverage for diagnostic imaging, increases in demand for cosmetic dentistry, and a larger elderly population with more complex dental needs are only a few of the attributes causing the market to grow.

Europe holds a major market share, with solid contributions from Germany, France, the UK, and Italy. The region benefits from strong public health care systems and a high level of awareness for oral health, particularly in the aging population. In Germany, for example, over 80% of adults receive dental checkups once a year, most often including some type of radiographic procedure.

European Union-funded programs that promote early detection of oral cancer and detection of dental caries are further denoting the advancement of imaging technologies. The market is witnessing a progressive acceptance of CBCT systems and panoramic techniques in both Western and Eastern Europe within the prosthetic implantology and orthodontic imaging industries, with an increasing number of installations reported in Poland and Czech Republic.

The Asia-Pacific region is expected to see the highest growth rate, with a CAGR of 7.9% during the forecast period (2025–2033), due to an increasing pace of urbanization, rising levels of disposable income, and increasing availability of dental care. China, India, Japan, and South Korea are countries that are steadily investing in healthcare infrastructure including digital diagnostic equipment.

In India, for example, the number of dental clinics providing CBCT scans has more than doubled in the last five years, mainly due to increased awareness, and affordability. In Japan and South Korea, an aging population and government-subsidized government-supported screening programs are increasing the use of regular radiographic diagnostics. Lastly, the region has the potential to become a low-cost manufacturing center for dental imaging equipment.

The dental radiography market in Latin America and Middle East & Africa (MEA) is exhibiting moderate growth, driven by improved health-care delivery and a broader understanding of oral health. Demand for intraoral and panoramic radiography in Brazil and Mexico is being aided by government public campaigns round oral hygiene and the growth of private dental chains.

The Middle East represents another significant opportunity where countries like Saudi Arabia and the UAE have been rapidly investing in modern dental clinics with extensive imaging systems as part of curated treatment plans.

A lack of access to digital radiography still persist in many parts of Africa and rural Latin America – due to the high cost of equipment, limited insurance coverage and insufficiencies in number of trained dental professionals – can challenge deeper market penetration despite growing burdens of dental disease.

The Dental Radiography market was valued at USD 3.2 billion in 2024.

The market is projected to grow at a CAGR of 6.1% from 2025 to 2033.

The digital dental radiography hold the largest market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Dentsply Sirona, Planmeca Oy and Carestream Health, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 The Dental Radiography Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 The Dental Radiography Market, By Application

5.3 The Dental Radiography Market, By End User

6.1 The Dental Radiography Market, By Country

6.1.1 The Dental Radiography Market, By Product Type

6.1.2 The Dental Radiography Market, By Application

6.1.3 The Dental Radiography Market, By End User

6.2 U.S.

6.2.1 The Dental Radiography Market, By Product Type

6.2.2 The Dental Radiography Market, By Application

6.2.3 The Dental Radiography Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping