3D Printed Medical Device Market

3D Printed Medical Device Market Share & Trends Analysis Report, By Product Type (Orthopedic implants, dental implants, cranio-maxillofacial implants, spinal implants, prosthetics, surgical guides, surgical instruments, tissue-engineered products, hearing aids, and wearable medical devices), By Material Type (Metal (titanium, stainless steel), polymers, ceramics, composites, plastics (thermoplastics, photopolymers), biomaterial inks, paper, and wax), By Technology Type (Laser Beam Melting (DMLS, SLS, SLM, LaserCUSING), Photopolymerization (DLP, Stereolithography, Two-photon Polymerization, PolyJet), Droplet Deposition/Extrusion-based Technologies, Electron Beam Melting (EBM), Fused Deposition Modeling, and Laminated Object Manufacturing), By End-User (Hospitals and surgical centers, dental and orthopedic clinics, academic institutions and research laboratories, pharma-biotech and medical device companies, and clinical research organizations) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

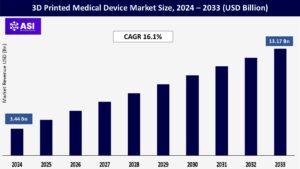

CAGR: 16.1%

Last Updated : March 7, 2026

The worldwide market for 3D Printed Medical Device was valued at approximately USD 3.44 billion in 2024 and is projected to reach USD 13.17 billion by 2033, demonstrating a compound annual growth rate (CAGR) of 16.1% during the forecast period of 2025–2033.

The 3D Printed Medical Device Market 2024–2033 report offers a clear and accessible look at one of the healthcare industry’s most rapidly advancing sectors. It doesn’t just lay out facts and figures—it helps readers truly understand the current state of the market, what’s driving its growth, and where it’s likely headed over the next decade. Whether you’re an investor looking for emerging opportunities, a manufacturer planning your next move, a healthcare provider considering new treatment options, or a policymaker shaping the future of medical technology, this report is designed to be an essential guide to navigating the exciting, transformative world of 3D-printed medical devices.

A key driver of this market is the ability of 3D printing to produce implants, prosthetics, and surgical guides that are custom-made for each patient. By precisely matching a person’s unique anatomy, these tailored solutions help improve treatment outcomes and make healthcare more personalized than ever.

One of the major forces driving the growth of 3D printing in healthcare is the constant wave of innovation in both technology and materials. Advances such as higher-resolution printers and faster printing speeds are making it easier and more efficient to produce complex medical devices with incredible precision. At the same time, researchers and manufacturers are developing a new generation of biocompatible materials that are safe for use inside the human body. These materials are opening the door to more advanced applicationsfrom patient-specific implants to custom surgical tools—broadening the scope of what 3D printing can achieve in medicine. As a result, more hospitals, clinics, and manufacturers are embracing this technology, recognizing its potential to transform patient care and streamline treatment processes.

Despite its growing potential, one of the key challenges facing the 3D printed medical device market is the high initial cost of adoption. Advanced 3D printers designed specifically for medical use, along with the specialized biocompatible materials they require, often come with a hefty price tag. For large healthcare institutions or well-funded companies, this investment might be manageable.

However, for smaller medical facilities, startups, or clinics operating on tight budgets, the cost can be a significant hurdle. These organizations may struggle to justify or afford the upfront expense, even if the long-term benefits are promising. As a result, access to cutting-edge 3D printing technology in healthcare may remain uneven, potentially slowing down broader adoption across the industry.

Another important challenge for the 3D printed medical device market is the shortage of skilled professionals who have the specific expertise needed to make the technology work effectively in healthcare settings. Operating and maintaining advanced 3D printers isn’t as simple as pushing a button—it requires a deep understanding of materials science to select the right biocompatible materials, knowledge of biomedical engineering to design safe and effective devices, and familiarity with strict regulatory standards that govern medical products.

Unfortunately, there simply aren’t enough trained specialists who can bridge these areas of expertise. This talent gap can make it difficult for hospitals, clinics, and manufacturers to fully embrace 3D printing, slowing the rollout of new solutions and limiting the potential benefits for patients. Expanding training programs and developing a skilled workforce will be critical to overcoming this barrier and unlocking the technology’s full promise in healthcare.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Orthopedic implants dental implants cranio-maxillofacial implants spinal implants prosthetics surgical guides surgical instruments tissue-engineered products hearing aids wearable medical devices |

| By Material Type |

Metal (titanium, stainless steel) Polymers Ceramics Composites plastics (thermoplastics, photopolymers) biomaterial inks paper wax |

| By Technology Type |

Laser Beam Melting (DMLS, SLS, SLM, LaserCUSING) Photopolymerization (DLP, Stereolithography, Two-photon Polymerization, PolyJet) Droplet Deposition/Extrusion-based Technologies Electron Beam Melting (EBM) Fused Deposition Modeling Laminated Object Manufacturing |

| By End-User |

Hospitals and surgical centers dental and orthopedic clinics academic institutions and research laboratories pharma-biotech and medical device companies clinical research organizations |

| Key Players |

3D Systems Corporation Materialise NV Stratasys Ltd. EOS GmbH Electro Optical Systems EnvisionTEC (now part of Desktop Metal) Renishaw plc Arcam AB (a GE Additive company) Concept Laser GmbH (a GE Additive company) Prodways Group SLM Solutions Group AG Carbon, Inc. Formlabs Organovo Holdings Inc. Cyfuse Biomedical K.K. 3T Additive Manufacturing Ltd. (formerly 3T RPD Ltd.) General Electric (GE Additive) Proto Labs Anatomics Pty Ltd. Biomedical Modeling Inc. Dentsply Sirona HP Inc. Oxford Performance Materials Axial3D Siemens Healthineers Fathom Manufacturing DWS Systems SRL RegenHU FIT AG Triastek, Inc. FabRx Aprecia Pharmaceuticals Fluicell Gesim Inventia Align Technology Medtronic Johnson & Johnson Berkshire Hathaway Stryker Orthopaedic Innovation Centre Zimmer Biomet Holdings 3M WS Audiology |

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The 3D Printed Medical Device Market is categorized by product type, by technology, by application and by end-user. Each segment is rapidly evolving, with different areas of the industry growing at their own pace and shifting in how much of the market they represent. Each segment provide a comprehensive understanding of its dynamics and growth opportunities. The 3D Printed Medical Device Market is typically segmented across several key dimensions to provide a detailed understanding of its structure and opportunities.

The market can be divided into different segments based on the types of medical devices being produced and their specific uses. Implants make up a large part of this landscape. For example, orthopedic implants are a leading segment, covering customized hip, knee, and spinal implants, along with components for joint replacements and fracture repairs. These are in high demand due to the widespread prevalence of musculoskeletal conditions and the need for solutions tailored to each patient.

Dental implants include crowns, bridges, dentures, and surgical guides that allow for highly precise and personalized treatments for individual patient anatomies. Then there are cranio-maxillofacial (CMF) implants, which are custom-made for reconstructing facial and skull structures, commonly used after trauma, cancer surgeries, or to correct congenital deformities.

Beyond implants, 3D printing is revolutionizing prosthetics and orthotics by enabling the creation of external limbs, braces, and supports designed for a perfect fit and optimal function for each user. Surgical guides and instruments also benefit, with 3D printing producing models for pre-surgical planning, training replicas, and patient-specific cutting or drilling guides that improve surgical precision. An especially exciting and rapidly advancing area is bioprinted tissues and organs, which involves printing living cells and biomaterials to create functional tissues and eventually entire organs for transplantation and research.

Finally, there’s a category for other applications, such as custom-made hearing aids, wearable medical devices, and other specialized solutions that serve niche medical needs. Overall, this segmentation highlights the incredible versatility of 3D printing in delivering personalized, high-quality care across many areas of medicine.

This part of the market breaks things down by the types of materials used in the 3D printing process, each chosen for its unique properties and suitability for medical applications. Metals and alloys are a key category. For example, titanium and its alloys are especially popular because they’re highly biocompatible, strong yet lightweight, and resistant to corrosion—qualities that make them perfect for orthopedic and dental implants. Stainless steel is another staple, often used for manufacturing medical instruments and certain types of implants.

Polymers are equally important in medical 3D printing. Among them, thermoplastics like PEEK (Polyether Ether Ketone) stand out for their strength, stability, and radiolucency, making them well-suited for spinal and cranio-maxillofacial implants. Photopolymers and resins, used in technologies like SLA (stereolithography) and DLP (digital light processing), are common for creating highly detailed dental models, surgical guides, and some types of prosthetics.

Ceramics are chosen for specific dental applications and bone substitutes because of their hardness and excellent biocompatibility. Meanwhile, composites combine different materials to deliver tailored properties for specialized uses. Finally, there’s the highly innovative area of biomaterial inks, which are vital for bioprinting.

These include hydrogels and bio-inks that can contain living cells and biodegradable materials, enabling the creation of functional tissues for research and, potentially, future transplants. Overall, the diverse range of materials highlights the flexibility of 3D printing technology to meet many different medical needs.

This part of the market is categorized based on the different 3D printing technologies used, each offering unique advantages for medical applications. Laser-based technologies are among the most advanced. For example, Selective Laser Sintering (SLS) uses a laser to fuse powdered polymer materials layer by layer, creating durable and detailed parts. Selective Laser Melting (SLM) is similar but designed for metals, fully melting metal powder to produce strong, precise components.

Direct Metal Laser Sintering (DMLS) is another metal-focused process that sinters metal powder to build complex medical parts, such as implants, with excellent accuracy. Photopolymerization technologies are also widely used in healthcare. Stereolithography (SLA) employs a UV laser to cure layers of liquid resin into solid parts, delivering incredibly fine detail—perfect for dental models and surgical guides. Digital Light Processing (DLP) works much like SLA but uses a digital projector to cure entire layers at once, making it faster while maintaining high precision.

PolyJet technology resembles inkjet printing: it jets layers of liquid photopolymer and instantly cures them with UV light, allowing for smooth, multi-material, and multi-color medical models. Extrusion-based technologies add further versatility.

Fused Deposition Modeling (FDM) is one of the most accessible methods, melting and extruding thermoplastic filament layer by layer to create durable, cost-effective medical parts and prototypes. Finally, there’s Electron Beam Melting (EBM), which uses an electron beam in a vacuum to melt metal powder, typically titanium, making it ideal for producing high-quality, biocompatible implants with complex geometries. Altogether, these varied technologies allow for a wide range of medical applications, from affordable prototypes to patient-specific implants and surgical tools.

This part of the market is organized by where 3D printed medical devices are most commonly used, highlighting how different settings take advantage of the technology’s strengths. Hospitals and surgical centers make up one of the largest groups of end users. They rely on 3D printing for things like pre-surgical planning models that help surgeons visualize complex procedures, patient-specific implants designed for a perfect fit, and custom surgical instruments that improve precision in the operating room.

Dental and orthopedic clinics are another important segment, using 3D printing to produce highly customized dental prosthetics, aligners, crowns, and specialized orthopedic devices tailored to each patient’s needs. Academic and research institutions also play a critical role. They’re at the forefront of exploring new applications, developing innovative materials, and pushing the boundaries of what 3D printing can do in medicine. Their work helps lay the foundation for future clinical use. Medical device companies are equally important, as they scale up production to design, manufacture, and distribute 3D printed devices to a wider market, making advanced solutions accessible to more healthcare providers.

Finally, pharmaceutical and biotechnology companies are beginning to harness 3D printing for cutting-edge uses like personalized drug dosage forms, rapid prototyping in drug development, and creating realistic tissue models for testing. Together, these diverse settings showcase just how widely 3D printing is being adopted to improve healthcare and patient outcomes.

The regional analysis of the 3D printed medical device market reveals some clear trends about where the technology is thriving and where it’s poised for rapid growth. North America currently leads the market, thanks to its advanced healthcare infrastructure, widespread technological adoption, and strong support for innovation.

Hospitals, research institutions, and medical device companies across the region have the resources and expertise to invest in cutting-edge 3D printing solutions, helping drive early adoption and market maturity. Meanwhile, the Asia-Pacific is emerging as the fastest-growing region. Improvements in healthcare access, rising demand for high-quality medical care, and increasing investments from both public and private sectors are fueling a surge in adoption.

Countries across the region are rapidly building up their capabilities, making it a hotspot for future growth. Europe, for its part, maintains a solid and influential position in the global market. With its well-established healthcare systems, strong regulatory frameworks, and significant investment in research and development, Europe continues to advance new applications and ensure high-quality standards. Together, these regional dynamics illustrate how 3D printing in medicine is spreading worldwide, with mature markets setting the pace and fast-growing regions expanding the technology’s reach to more patients than ever.

North America stands out as the dominant market for 3D printed medical devices, consistently holding the largest share worldwide. This leadership is largely thanks to the region’s highly developed healthcare infrastructure and significant spending on healthcare overall. Several factors reinforce its strong position. The region is home to many leading companies and boasts a robust ecosystem for research and development, making it a natural hub for innovation. There’s also a growing demand for customized, patient-specific medical devices produced through additive manufacturing, as healthcare providers and patients alike recognize the benefits of personalized care.

Favorable funding initiatives, both public and private, are supporting the adoption of 3D printing in healthcare, while hospitals and research institutions across North America have been quick to embrace these technologies in their daily practice. Another big advantage is the clean regulatory environment, with the FDA providing well-defined guidelines that give manufacturers confidence to develop and market new products.

Within North America, the United States leads by a wide margin. It acts as the region’s powerhouse for technological innovation and early adoption, with hospitals, research centers, and companies using 3D printing for everything from patient-specific anatomical models to surgical planning tools and customized implants. Recently, there’s been particular interest in advanced polymers for biocompatible applications, such as 3D-printed, patient-specific PEEK implants, highlighting the region’s ongoing commitment to pushing the boundaries of what’s possible in personalized medicine.

Europe holds a significant share of the global 3D printed medical device market and is often highlighted as one of the fastest-growing regions in this space. Several factors contribute to its strong position. For one, Europe benefits from a large and diverse patient base, along with favorable healthcare strategies that often include broad coverage under national health services—for example, the NHS in the UK—making advanced treatments more accessible. The availability and adoption of 3D-printed solutions are steadily increasing, supported by healthcare providers who recognize the value of customized, patient-specific care.

Demand is also fueled by the rising number of surgical procedures, whether it’s treating kidney stones, trauma from auto accidents, or other conditions that require precision-made implants or surgical guides. Public and private sectors across Europe continue to invest in research and development, further advancing 3D printing technologies. One area of particular progress is metal 3D printing, which has become increasingly important for manufacturing high-quality implants and dental products.

Within the region, Germany often leads the way, followed by the UK, thanks to their advanced healthcare systems, well-established infrastructures, and strong commitment to adopting innovative technologies. Recent trends also point to growth in the production of custom prosthetics and implants, driven by investor interest and the emergence of new medical device companies eager to meet the demand for more personalized healthcare solutions.

The Asia-Pacific (APAC) region is poised to be the fastest-growing market for 3D printed medical devices, with forecasts projecting the highest compound annual growth rate (CAGR) during the coming years. This rapid expansion is being driven by several key factors. Across the region, healthcare spending is on the rise, and medical infrastructure is steadily improving, making advanced treatments more accessible to a larger population. There’s also a growing number of patients in need of orthopedic procedures, such as hip and knee surgeries, fueling demand for customized implants and surgical tools. Governments in countries like Japan, China, and India are actively supporting the sector through favorable initiatives and by investing in research and development, helping to advance local expertise and innovation.

At the same time, there’s a strong appetite for personalized and cost-effective medical solutions that 3D printing is well-suited to deliver. Rapid technological improvements are expanding the range of applications, from prosthetics and implants to surgical planning models and even tissue engineering. Japan often leads the APAC market thanks to its strong culture of innovation in both medical and pharmaceutical 3D printing applications, while China and India are also seeing significant growth as their healthcare systems modernize and embrace new technologies.

However, despite this impressive momentum, the region still faces some challenges, such as the high initial costs of adopting advanced 3D printing equipment and limited reimbursement support in certain developing economies. Overcoming these barriers will be crucial to unlocking the full potential of 3D printing in transforming healthcare across the Asia-Pacific.

Emerging markets represent a promising frontier for the growth of 3D printed medical devices, with strong potential to expand in the coming years. In many of these regions, the use of 3D printing is gaining popularity, especially in specialized areas like dental work and craniomaxillofacial surgeries, where customized, patient-specific solutions can make a significant difference in outcomes.

Governments are also recognizing the technology’s potential and are launching initiatives aimed at encouraging its adoption within healthcare systems. Alongside this, more medical device companies are entering these markets, and investments in healthcare infrastructure are on the rise, laying the groundwork for broader access to advanced medical care.

However, these markets still face some important challenges. The high costs of acquiring and maintaining advanced 3D printing equipment can be a significant barrier for many hospitals and clinics, particularly in regions with limited healthcare budgets. Regulatory frameworks may also be less developed or more difficult to navigate, creating uncertainty for companies looking to introduce new products.

Additionally, there can be a shortage of skilled professionals with the specialized expertise needed to operate 3D printing equipment and design patient-specific solutions. Overcoming these obstacles will be crucial to ensuring that the benefits of 3D printed medical devices can reach patients in emerging markets just as effectively as in more developed regions.

The market was valued at USD 3.44 billion in 2024.

The market is projected to grow at a CAGR of 16.1% from 2025 to 2033.

The residential segment holds the largest market share.

Asia-Pacific region is expected to witness the highest growth rate.

Major players include 3D Systems Corporation, Stratasys Ltd., Materialise NV, EOS GmbH, and Renishaw plc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 3D Printed Medical Device Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 3D Printed Medical Device Market, By Material Type

5.3 3D Printed Medical Device Market, By Technology Type

5.4 3D Printed Medical Device Market, By End-Users

6.1 North America 3D Printed Medical Device Market , By Country

6.1.1 3D Printed Medical Device Market, By Product Type

6.1.2 3D Printed Medical Device Market, By Material Type

6.1.3 3D Printed Medical Device Market, By Technology Type

6.1.4 3D Printed Medical Device Market, By End-Users

6.2 U.S.

6.2.1 3D Printed Medical Device Market, By Product Type

6.2.2 3D Printed Medical Device Market, By Material Type

6.2.3 3D Printed Medical Device Market, By Technology Type

6.2.4 3D Printed Medical Device Market, By End-Users

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping