Automotive Electronics Market

Automotive Electronics Market Share & Trends Analysis Report, By Component (ECUs, Sensors, Microcontrollers, Power Electronics, Displays), By Application (ADAS, Infotainment, Powertrain, Safety, Body Electronics), By Vehicle Type (Passenger Cars, Commercial Vehicles, Electric Vehicles) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

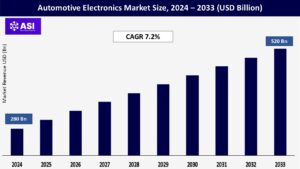

CAGR: 7.2%

Last Updated : May 25, 2026

The global Automotive Electronics Market size was valued at around USD 280 billion in 2024 and is anticipated to reach USD 520 billion by 2033, with a CAGR of 7.2% throughout the forecast period from 2025 to 2033.

The automotive electronics market pertains to the incorporation of sophisticated electronic systems and semiconductors into vehicles to improve safety, comfort, performance, and connectivity.

These electronic components encompass microcontrollers, sensors, ECUs (Electronic Control Units), power modules, and infotainment systems, all of which are essential for the operation of modern vehicles—particularly electric vehicles (EVs), autonomous vehicles, and connected cars.

The sector is experiencing rapid changes driven by the growing electrification of vehicles, the rising demand for digital experiences within cars, and regulatory requirements for safety and emissions control.

As research and development in semiconductor technology continues to progress—particularly in power electronics and AI-driven processing—automotive electronics are becoming increasingly energy-efficient, compact, and intelligent, promoting their adoption across all vehicle segments.

One of the key factors propelling the automotive electronics industry is the increasing incorporation of ADAS and semi-autonomous functionalities in contemporary vehicles.

Due to heightened concerns regarding road safety, governments in various regions have implemented strict safety regulations that require technologies such as lane departure warning, adaptive cruise control, blind spot detection, and automatic emergency braking.

These systems depend significantly on an array of electronics, which includes radars, cameras, LiDAR, ultrasonic sensors, and sophisticated electronic control units (ECUs).

The drive towards autonomous driving is spurring advancements in high-performance automotive semiconductors and embedded systems, which are crucial for real-time data processing, vehicle-to-everything (V2X) communication, and decision-making in autonomous vehicles.

The worldwide transition to electrified mobility serves as a critical driver for the demand for automotive electronics. Electric vehicles (EVs) necessitate a sophisticated range of electronic components, including battery management systems (BMS), inverters, onboard chargers, and thermal management systems.

As the acceptance of EVs grows, the requirement for power electronics like IGBTs, MOSFETs, and SiC-based semiconductors increases, facilitating efficient energy conversion and enhancing battery performance.

Government initiatives providing incentives for EVs and targets for reducing CO₂ emissions are motivating original equipment manufacturers (OEMs) to accelerate electronic innovation, thereby significantly broadening the role of automotive electronics in both powertrain and vehicle intelligence systems.

One of the primary limitations in the automotive electronics sector is the significant expense and complexity involved in incorporating advanced electronic systems into vehicles.

As car manufacturers embrace features such as ADAS, infotainment systems, and electric vehicle power management, the demand for advanced electronic components like sensors, ECUs, microcontrollers, and power electronics has increased dramatically.

These systems are required to adhere to strict automotive-grade standards for reliability, safety, and interoperability, which lengthens development times and raises costs. Moreover, the ongoing global semiconductor chip shortage, caused by supply chain interruptions and geopolitical conflicts, has greatly affected production schedules, resulting in manufacturing delays and higher component prices.

A number of original equipment manufacturers (OEMs), especially those in emerging markets, struggle to adapt to the quickly changing electronics landscape while keeping their products affordable.

These challenges, along with the limited availability of skilled labor and integration tools, pose significant obstacles—particularly for small and medium-sized automotive manufacturers aiming to expand their smart vehicle offerings effectively.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Component |

ECUs Sensors Microcontrollers Power Electronics Displays |

| By Application |

ADAS Infotainment Powertrain Safety Body Electronics |

| By Vehicle Type |

Passenger Cars Commercial Vehicles Electric Vehicles |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Automotive Electronics sector is categorized by components (such as ECUs, sensors, microcontrollers, power electronics, and displays), applications (including ADAS, infotainment, powertrain, safety, and body electronics), and types of vehicles (passenger cars, commercial vehicles, and electric vehicles), with significant growth fueled by the rise of EV adoption and a growing need for safety and connectivity features.

The automotive electronics industry comprises a diverse array of components, each playing vital roles Electronic Control Units (ECUs) These function as the hub of vehicle electronics, overseeing operations in areas such as powertrain, advanced driver-assistance systems (ADAS), entertainment, and safety measures.

With the progression towards more connected and autonomous driving, the quantity of ECUs in each vehicle is on the rise Sensors Key for gathering data in functionalities like ADAS, climate control, and engine oversight.

They encompass radar, LiDAR, ultrasonic, temperature, and pressure sensors Microcontrollers (MCUs) These drive embedded systems that manage vehicle functions including braking, illumination, climate control, and electronic steering.

Power Electronics They facilitate the effective transmission and transformation of electrical energy, particularly essential in electric and hybrid vehicles for managing batteries and controlling motors. Displays Present in digital instrument clusters, infotainment screens, and head-up displays, they align with the increasing trend towards digital dashboards.

Advanced Driver Assistance Systems (ADAS) Comprises technologies such as lane departure alerts, adaptive cruise control, and collision prevention. The increasing safety regulations and the movement toward autonomous vehicles are propelling its adoption. Infotainment & Connectivity Encompasses touchscreens, audio systems, navigation, and smartphone connectivity.

There is a growing consumer expectation for seamless digital experiences in vehicles. Powertrain Electronics Involves control systems for internal combustion engines, hybrid setups, and electric driving units. Effective power distribution and energy management are crucial, particularly in electric vehicles.

Safety Systems Include airbags, anti-lock braking systems (ABS), electronic stability control, and automated braking essential for the protection of vehicle occupants. Body Electronics Consist of lighting systems, seat adjustments, climate control, and remote keyless entry, enhancing both comfort and convenience for the driver.

Passenger Cars This segment is the largest, driven by strong consumer interest in comfort, safety, and digital technology. Commercial Vehicles There is a rising adoption of telematics, fleet management, and safety-related electronics in both light and heavy-duty vehicles. Electric Vehicles (EVs) The quickest expanding segment, where electronics are crucial for propulsion, battery systems, and vehicle intelligence.

North America occupies a significant portion of the global automotive electronics market, with the United States and Canada leading the way. This area hosts numerous automotive OEMs and prominent semiconductor companies, encouraging technological advancement.

A heightened emphasis on vehicle safety, self-driving capabilities, and electric mobility is driving the need for sophisticated electronics such as ADAS modules, infotainment systems, and power electronics.

The U.S. is leading the charge in the development of connected vehicle and autonomous driving technology, backed by governmental investments and private research and development financing.

Furthermore, the presence of major technology companies and partnerships between automotive and electronics industries foster rapid innovation in in-vehicle connectivity, AI-based sensors, and vehicle-to-everything (V2X) communication.

The growing adoption of electric vehicles, particularly in California and other forward-thinking states, is also increasing the demand for battery management systems and electric drive control electronics.

Europe stands out as a region with advanced technological capabilities in the automotive industry, fueled by stringent environmental regulations and a fiercely competitive market.

Nations such as Germany, France, and the UK are pioneering advancements in safety, fuel efficiency, and emissions management through the implementation of advanced electronic components.

The EU’s requirements regarding Euro 6/7 standards, electric vehicle adoption goals, and advanced driver-assistance systems (ADAS) have made the integration of electronics essential in vehicle production.

Particularly, Germany serves as a center for Tier-1 suppliers and high-end automotive brands, excelling in the creation of high-performance electronic control units (ECUs), infotainment systems, and electronic powertrain technologies.

Moreover, European manufacturers are significantly investing in partnerships with semiconductor companies and developing their own chip production to lessen dependence on supply chains from Asia.

The Asia-Pacific region represents the largest and the quickest expanding market for automotive electronics, with China, Japan, South Korea, and India at the forefront. China leads in both vehicle manufacturing and usage, supported by robust policies aimed at promoting electric vehicles and smart mobility solutions.

The government’s backing for electric vehicle subsidies, smart city projects, and 5G infrastructure for automotive applications has increased the demand for advanced electronics such as chips for autonomous driving, state-of-the-art infotainment systems, and control units for electric vehicles.

Japan and South Korea excel globally in producing automotive semiconductors and high-precision electronics, whereas India is rising as an economical production center with a growing need for connected and electrified vehicles.

The rapid growth of urban areas, the rise of the middle class, and a notable increase in consumers who are tech-savvy are all contributing to the rising adoption of electronics in both mainstream and luxury vehicles.

Latin America offers moderate growth potential, particularly thanks to countries like Brazil and Mexico, which have developed automotive manufacturing sectors. The rise of automotive electronics in this area is mainly fueled by increased vehicle production and a growing consumer demand for infotainment and safety features.

Mexico’s closeness to the United States and its trade agreements have established it as an important supplier of vehicles and components. Nevertheless, the region continues to face obstacles such as inadequate EV infrastructure, economic volatility, and a lower integration of electronics in budget vehicle categories.

The automotive electronics market in the MEA region is still in its early phases, with growth driven by increasing vehicle ownership, infrastructure enhancements, and a slow but growing interest in electric vehicles. Nations such as the UAE, Saudi Arabia, and South Africa are making investments in smart transportation and testing autonomous mobility.

Nevertheless, challenges such as limited local manufacturing, a heavy dependence on imports, and cost sensitivity impede broader acceptance. Over time, it is anticipated that demand will grow as digitization increases and sales of luxury vehicles rise.

The market was valued at USD 345.7 billion in 2024.

The market is projected to grow at a CAGR of 7.2% from 2025 to 2033.

Passenger Vehicles dominate in terms of vehicle type, while ECUs lead the component category.

The Asia-Pacific region is expected to witness the highest growth rate.

Key companies include Bosch, Denso, Continental, Aptiv, NXP, and Infineon.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Electronics Market, By Component

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Electronics Market, By Application

5.3 Automotive Electronics Market, By Vehicle Type

6.1 North America Automotive Electronics Market , By Country

6.1.1 Automotive Electronics, By Component

6.1.2 Automotive Electronics, By Application

6.1.3 Automotive Electronics, By Vehicle Type

6.2 U.S.

6.2.1 Automotive Electronics, By Component

6.2.2 Automotive Electronics, By Application

6.2.3 Automotive Electronics, By Vehicle Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping