Copper Clad Steel Wire Market

Copper Clad Steel Wire Market Share & Trends Analysis Report, By Type (Solid, Stranded), By Coating Type (Lightly Coated, Medium Coated, Heavy Coated), By Application (Telecommunication, Power Transmission, Grounding Systems, Automotive, Others), By End User (Utilities, Industrial, Construction, Electronics, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

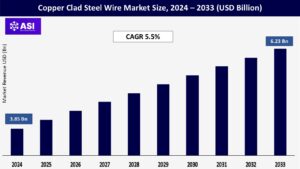

CAGR: 5.5%

Last Updated : February 3, 2026

The worldwide copper-clad steel wire market size was estimated at around USD 3.85 billion in 2024 and is anticipated to grow to USD 6.23 billion by 2033, with a compound annual growth rate (CAGR) of 5.5% during the period from 2025 to 2033.

Copper Clad Steel (CCS) wire is a bimetallic conductor that merges the high tensile strength of steel with the outstanding conductivity and corrosion resistance of copper. This wire is made up of a steel core encased in a concentric copper cladding that is bonded together through either mechanical or metallurgical methods. CCS wire is increasingly being utilized in electrical systems, grounding solutions, telecommunications, radio frequency applications, power transmission, and automotive parts due to its enhanced durability, cost-effectiveness, and lighter weight compared to pure copper wire.

The market for CCS wire is experiencing strong demand as various industries look for alternatives to conventional copper conductors to lower material expenses while preserving performance. With the global telecommunications infrastructure steadily expanding, especially for 5G networks, smart grids, and high-frequency signal transmission systems, the use of CCS wire continues to rise. Its resistance to corrosion and theft, alongside its adaptability in construction and power applications, positions it as a preferred option in both developed and emerging markets within the global copper clad steel wire industry.

One of the key contributors to the CCS wire market is the rising demand for copper clad steel in RF transmission lines, coaxial cables, and telecommunications infrastructure. CCS wire merges the high tensile strength of steel with the superior conductivity of copper, making it suitable for high-frequency signal transmission while minimizing attenuation.

As global data consumption continues to rise with the introduction of 5G, the popularity of streaming services, and the proliferation of IoT devices, there is an increasing demand for affordable and durable cabling solutions. In many cases, CCS wire is favored over pure copper due to its combination of performance and cost-effectiveness, particularly in extensive deployments such as broadband networks and antenna grounding applications. These trends are directly contributing to sustained copper clad steel wire market growth.

The fluctuations and increasing expenses of raw copper have led various industries to explore alternatives that provide comparable electrical characteristics at reduced prices. CCS wire addresses this issue by incorporating a steel core, significantly decreasing the amount of copper while still ensuring sufficient conductivity for numerous uses.

This financial benefit, along with its lighter weight and enhanced mechanical strength, makes CCS wire appealing for uses in grounding, power distribution, and industrial electrical work. As industries place greater emphasis on cost efficiency without sacrificing performance, CCS wire is becoming more popular as a practical replacement for solid copper conductors.

A significant limitation in the Copper Clad Steel (CCS) Wire market is its inferior electrical conductivity compared to solid copper wire. Although CCS wire provides cost efficiencies and enhanced tensile strength, it usually only achieves about 30% of the conductivity of pure copper.

This drawback renders it inappropriate for certain high-performance or high-current applications, like heavy power transmission or delicate electronic circuits, where reduced resistance and high conductivity are vital. Consequently, industries that demand ultra-low signal loss or exact electrical performance may choose pure copper, even at a higher price.

Additionally, a lack of technical understanding and compatibility concerns may impede acceptance in traditional sectors where copper remains the conventional choice. In scenarios where both mechanical and electrical qualities are critical, the compromise in conductivity poses a notable disadvantage, limiting CCS wire’s market penetration despite its advantages in cost-effectiveness and durability. Despite these limitations, cost efficiency and mechanical durability continue to support long-term prospects for the copper clad steel wire industry.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Type |

Solid Stranded |

| By Coating Type |

Lightly Coated Medium Coated Heavy Coated |

| By Application |

Telecommunication Power Transmission Grounding Systems Automotive Others |

| By End User |

Utilities Industrial Construction Electronics Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The market for copper clad steel wire is divided By Type (Solid, Stranded), By Coating Type (Lightly Coated, Medium Coated, Heavy Coated), By Application (Telecommunication, Power Transmission, Grounding Systems, Automotive, Others), By End User (Utilities, Industrial, Construction, Electronics, Others). Solid wires dominate grounding applications because of their superior strength and conductivity. The telecommunications and power transmission industries are the primary drivers of demand, accounting for a substantial copper clad steel wire market share.

The CCS wire market is divided by type into solid and stranded wires. Solid CCS wires are made up of a single steel core encased in a copper layer, providing high strength and durability. These wires are typically utilized in grounding and overhead applications because of their rigidity and structural integrity.

Stranded CCS wires, on the other hand, are formed from multiple smaller strands twisted together, offering increased flexibility and better conductivity distribution, which makes them ideal for applications that require bending, such as telecom and data transmission cables.

Copper Clad Steel wires come with varying thicknesses of coating and types of copper bonding. The coatings can be electroplated, hot-dipped, or created through pressure rolling, all of which influence conductivity and resistance to corrosion.

Furthermore, certain CCS wires may have a tin coating or polymer insulation to improve weather resistance and facilitate soldering, particularly in outdoor or electronic applications. The quality of the coating plays a crucial role in determining performance under high-frequency and corrosive conditions.

CCS wires are commonly utilized in telecommunications, power distribution, automotive applications, electrical grounding, and electronics. In the telecommunications sector, CCS wires play a crucial role in coaxial and drop cables due to their excellent signal transmission capabilities and cost-effectiveness.

Their tensile strength makes them suitable for grounding uses in long-lasting installations. In automotive wiring, they help decrease weight while still ensuring conductivity. The electronics sector employs CCS in components that need durability but can handle lower conductivity compared to pure copper.

Key consumers of CCS wire encompass telecom service providers, power utilities, construction firms, automotive manufacturers, and electronics OEMs. Telecommunications companies favor CCS for their broadband infrastructure needs.

Power utilities utilize it for their grounding and earthing systems. In the construction sector, CCS is preferred for lightning protection and earthing networks. Automotive and electronics manufacturers utilize CCS wire for affordable, lightweight options in wiring harnesses and component assembly.

North America plays a crucial role in the global CCS wire market, largely due to strong demand from sectors such as telecommunications, power infrastructure, and construction. The United States is at the forefront of this trend, driven by extensive broadband expansion and significant investments in 5G technologies.

CCS wire is increasingly utilized in coaxial cables for transmitting signals and in grounding systems for substations and buildings. Furthermore, the rising trend of lightweight automotive parts in North America enhances the need for CCS as a more economical alternative to pure copper. The presence of top CCS wire manufacturers and a strong emphasis on energy-efficient infrastructure also support the growth of the market in the region.

Europe is influenced by progress in renewable energy, building automation, and automotive electronics. Nations like Germany, France, and the UK are making investments in smart grid technologies, where CCS wire plays a role in grounding and transmission.

The region’s strong focus on environmental regulations and resource efficiency promotes the use of composite materials such as CCS wire instead of pure copper to decrease material expenses and environmental effects. Furthermore, Europe’s automotive industry utilizes CCS wire in lightweight wiring harnesses and electronic subsystems to comply with emission and fuel efficiency regulations.

The CCS wire market is experiencing the fastest growth in the Asia-Pacific region, propelled by swift industrial development, advancing urban infrastructure, and a rising need for high-speed connectivity. China and India are the primary contributors, with significant installations of CCS wire in telecommunications networks, particularly in fiber-to-the-home (FTTH) projects. The region’s budget-conscious market prefers CCS wire due to its more affordable price compared to solid copper.

Additionally, increasing investments in smart cities, modernization of electrical grids, and transportation infrastructure across ASEAN nations, Japan, and South Korea further enhance growth in the area. The strengthening market presence is also supported by local manufacturing capabilities and a rise in exports from China. These developments are expected to significantly increase the copper clad steel wire market size across the Asia-Pacific region.

Latin America represents a growing market for CCS wire, with consistent demand arising from the construction, energy, and telecommunications industries. Nations like Brazil, Mexico, and Argentina are allocating resources towards rural electrification and the expansion of telecommunications, especially in underserved regions.

CCS wire is utilized in economical grounding and signal transmission applications. Nevertheless, the market faces challenges due to limited industrial manufacturing capabilities and reliance on imports. Still, regional development initiatives and foreign investment are anticipated to gradually boost adoption rates. Regional development initiatives are expected to support steady copper clad steel wire market growth over the forecast period.

Middle East and Africa are still evolving but demonstrate significant potential. Nations like the UAE, Saudi Arabia, and South Africa are making investments in infrastructure, energy diversification, and telecommunications, where CCS wire provides a reliable and cost-effective solution for wiring and grounding.

The growing emphasis on renewable energy and smart infrastructure, such as solar projects and digital power grids, also boosts demand. However, political instability in certain African regions and a limited manufacturing base may hinder widespread adoption. Ongoing foreign investments and infrastructure collaborations are expected to enhance growth in critical markets. Such initiatives are likely to gradually improve the copper clad steel wire market size in key MEA economies.

The copper clad steel wire market was valued at USD 3.85 billion in 2024.

The copper clad steel wire market is expected to grow at a CAGR of 5.5% between 2025 and 2033.

Telecommunication applications hold the largest copper clad steel wire market share, driven by broadband and 5G expansion.

Asia-Pacific is the fastest-growing region, supported by infrastructure development and copper cost mitigation.

The global copper clad steel wire market key playes are include CommScope, AFL, Furukawa Electric, LEONI, and ZTT Group.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Copper Clad Steel Wire Market By Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Copper Clad Steel Wire Market By Coating Type

5.3 Copper Clad Steel Wire Market By Application

5.4 Copper Clad Steel Wire Market By End User

6.1 North America Copper Clad Steel Wire Market, By Country

6.1.1 Copper Clad Steel Wire Market, By Type

6.1.2 Copper Clad Steel Wire Market By Coating Type

6.1.3 Copper Clad Steel Wire Market By Application

6.1.4 Copper Clad Steel Wire Market By End User

6.2 U.S.

6.2.1 Copper Clad Steel Wire Market, By Type

6.2.2 Copper Clad Steel Wire Market By Coating Type

6.2.3 Copper Clad Steel Wire Market By Application

6.2.4 Copper Clad Steel Wire Market By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping