Bioelectric Medicine Market

Bioelectric Medicine Market Share & Trends Analysis Report By Product Type (Implantable Devices, Non-Implantable Devices) By Application (Neurological Disorders, Cardiological Disorders, Hearing Disorders, Musculoskeletal Disorders, Gastrointestinal and Urological Disorders,) By End Use(Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, Rehabilitation Centers, Home Care Settings, Academic & Research Institutes), By Technology (Neuromodulation, Electrical Stimulation, Electromagnetic Therapy, Bioelectronic Implants, Closed-loop Systems (AI-Integrated Devices) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 4.9%

Last Updated : January 21, 2026

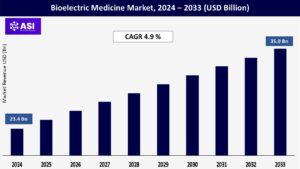

The global bioelectric medicine market size was valued at approximately USD 23.4 billion in 2024 and is projected to reach USD 35.0 billion by 2033, growing at a CAGR of 4.9 % during the forecast period (2025–2033).

Bioelectric medicine employs electrical impulses to modulate the body’s neural circuits for therapeutic purposes as a unique or complementary therapeutic option to drug therapy. Pacemakers, cochlear implants, spinal cord stimulators, and vagus nerve stimulators are some bioelectric devices that use targeted electrical stimulation to treat a health condition, e.g., arrhythmia (medically controlled heart rhythm), epilepsy, chronic pain, and Parkinson’s disease (movement). These bioelectric devices target specific neural circuits to modulate or modify biological functions that restore lost physiological activity.

Bioelectric therapies are increasingly accessible in addition to conventional therapeutics to achieve better clinical outcomes. The growing prevalence of chronic neurological and cardiovascular conditions, and advancements in neuromodulation technologies, and an increased need for non-invasive treatment options are expected to drive market growth. Increased investment in electroceutical research and healthcare expansion in emerging markets also continue to stimulate bioelectric medicine market development.

The rising incidence of global neurological disorders and chronic diseases including epilepsy, Parkinson’s disease, chronic pain, and depression contributes to the rapid growth of the bioelectric medicine market. According to the World Health Organization (WHO), neurological disorders are a leading cause of disability and death globally. Epilepsy impacts approximately 50 million people, while depression affects over 280 million people. Chronic pain is now estimated to affect 1 in 5 adults globally and is one of the most prevalent conditions reported.

Chronic pain often results in decreased mobility, worsening mental health, and increased use of healthcare resources. Pharmaceutical therapies are typically limited either by safety concerns and side effects, or by limited effectiveness, which has created a heightened focus on non-pharmacological options for neuromodulation therapy, supporting growth in the bioelectric medicine market size.

Bioelectric devices such as spinal cord stimulators, vagus nerve stimulators, and deep brain stimulators have been recognized as either alternatives to, or adjuncts to drugs. In 2023, the FDA in the U.S. approved LivaNova’s SenTiva DUO system, which is a next generation vagus nerve stimulator for treatment resistant epilepsy and depression, illustrating the shifting landscape of the joint bioelectric medicine market towards precision neuromodulation interventions. Moreover, a report by the International Neuromodulation Society released in 2024, showed a 17% increase from year to year in neuromodulation implantations worldwide, demonstrating increasing physician confidence and demand from patients.

As the incidence of these chronic and neurological diseases increases, the demand for bioelectric medicine technologies increases as well, not only within the aging population but especially within those that are more likely to suffer from these types of diseases.

The emergence of wireless, AI-capable, and small neuromodulation devices showcases the significant impact of technological innovation to grow the bioelectric medicine industry. Implementation of implantable bioelectronic devices strengthens the precision of medicines, improves battery time, and provides a patient with real-time feedback or even closed-loop control–all of which lengthen medicines’ efficacy and enhance comfort.

As an example, the Percept TM PC neurostimulator from Medtronic expected to become available in 2024 uses Brain Sense TM technology to store brain information and adapt stimulation accordingly to create more individualized and efficient treatment for individuals with movement disorders and Parkinson’s disease. Neuromodulation research and development have reportedly attracted USD 2.6 billion globally and continued investment in R&D for bioelectric medicine supports product development. According to a 2023 Evaluate MedTech report, worldwide investment in neuromodulation R&D exceeded USD 2.6 billion, with significant investment from both private equity and the public sector.

At the same time, with an estimated global health expenditure of USD 10.3 trillion in 2021 (World Economic Forum), access to these advanced therapies can extend beyond developed markets through health systems that expand specialized neurology and pain clinics. Additionally, the aging population is increasing demand for bioelectric therapies. According to the United Nations, there will be 2.1 billion people aged 60 or over globally by 2050, more than double the current figure today. Age is a risk factor for neurodegenerative diseases such as Alzheimer’s, Parkinson’s, the disabling effects of strokes in older populations, and many of these conditions can be treated through bioelectric devices.

As a result of these combined forces, both developed and developing markets are heavily investing in technologies designed to treat the clinical needs of aging populations, with bioelectric medicine emerging as key pillar in the management of chronic illness.

Though bioelectric medicine provides exciting new treatment options for neurological, cardiac, and inflammatory disorders, the chance of device-associated complications continue to be a significant barrier to the growth of the market. Many bioelectric devices, including deep brain stimulators (DBS), vagus nerve stimulators (VNS), and spinal cord stimulators (SCS) need to be surgically implanted which has its own risks which include the risks of an infection, device migration, nerve damage, or post-operative complications.

As mentioned in an article published by the Journal of Neurosurgery, hardware-related complications occur after DBS surgery in as many as 15% of patients and usually require surgical revision or explantation. Related rates can be aggravated by comorbidities, ineffective wound healing, or incorrect programming. Including the physical risks, implantable devices can have psychological risks, including anxiety, body image, or fear of adverse events, which can cause some patients to be reluctant to pursue this form of therapy.

Despite their therapeutic benefits, the risk of being invasive, harmful outcomes, and psychological implications will influence the decision-making of both patients and their doctors. Therefore, the ambiguities around surgical implantation safety and device reliability, can be a limitation to the use in the broader market, especially patients who are risk averse and/or don’t have access to appropriate care.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product Type |

Implantable Devices Non-Implantable Devices |

| By Application |

Neurological Disorders Cardiological Disorders Hearing Disorders Musculoskeletal Disorders Gastrointestinal and Urological Disorders |

| By End- Use |

Hospitals Ambulatory Surgical Centers (ASCs) Specialty Clinics Rehabilitation Centers Home Care Settings Academic & Research Institutes |

| By Technology |

Neuromodulation Electrical Stimulation Electromagnetic Therapy Bioelectronic Implants Closed-loop Systems (AI-Integrated Devices)

|

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Bioelectric medicine market is segmented by type, by application, by Technology, end-user. Each segment plays a crucial role in targeting specific nerve pathways or organs with precisely controlled electrical signals, rather than using pharmaceutical drugs.

Implantable Devices will dominate the bioelectric medicine market and maintain a substantial portion of the market share in 2024. These devices include cochlear implants, deep brain stimulators, spinal cord stimulators, cardiac pacemakers, etc. The benefit of many of these devices is the sustained availability of therapy for patients who suffer from chronic neurological and cardiovascular disorders.

Driven by the increasing prevalence of chronic diseases and the acceptance of neuromodulation therapies, there has been explosive market demand for implantable devices in bioelectric medicine. Non-Implantable devices are expected to report steady growth, but primarily in the areas of pain management and rehabilitation. There is growing momentum for transcutaneous electrical nerve stimulation (TENS) units and wearable neurostimulators for in-home care providers because they are non-invasive and easy to use. They are especially attractive to patients dealing with musculoskeletal pain or post-surgical pain.

Neurological Disorders are the largest segment by application, as there are increasing occurrences of disorders like Parkinson’s Disease, epilepsy, and chronic pain. We have been seeing an increase in the use of devices such as deep brain stimulators or vagus nerve stimulators in clinical practice are helpful to market expansion. Pacemakers and implantable cardioverter defibrillators (ICDs) help patients maintain regular heart rhythms or treat arrhythmias in patients so the share of cardiological disorders is a significant portion of bioelectronic therapy. The prevalence of cardiovascular diseases and the aging population greatly impact the market expansion of bioelectronic therapies for cardiological disorders.

There is a significant opportunity for growth in Hearing Disorders as the very high rate of successful application of cochlear implants leads to widespread acceptance of bioelectronic methods. The ongoing awareness and early detection of hearing impairment in children and adults will continue to lead to demand in this segment. There are advances in the use of TENS (transcutaneous electrical nerve stimulation) and EMS (Electrical Muscle Stimulation) for the treatment of chronic pain and in rehabilitation from surgery for Musculoskeletal Disorders.

There is an increasing source of demand for these devices as non-invasive electrotherapies are being used more extensively. Gastrointestinal Disorders and Urological Disorders are some new growing areas, where there are cases of bioelectronic like sacral nerve stimulation and gastric electrical stimulation being used to treat urinary incontinence and gastroparesis respectively, therefore expanding the application of bioelectronic medicine for various disorders.

In 2024, hospitals will continue to dominate the bioelectric device market, accounting for the largest amount of the market share because of their physical infrastructure for surgical implantation and device management. Hospitals can manage high levels of patient volume and have access to professional medical personnel that will provide excellent patient-centered care as they tackle a huge portion of the market for bioelectric devices – specifically procedures related to neuromodulation applications and providing implantable devices for cardiac patients.

Ambulatory Surgical Centers (ASCs) are growing quickly and, while they normally are looking for cost-effective solutions for treatments to be minimally invasive, one key factor is that patients expect to not have to stay in the hospital unless mandated for an inpatient procedure; perioperative patient care should be in the outpatient area. ASCs are utilizing increased levels of implant procedures, however, hospitals may lose a portion of “follow-on” care related to implanted devices such as spinal cord stimulators and neurostimulators where they also perform routine follow23up.

Specialty Clinics focused on Neurology and Pain Management capture similar types of services related to implantable and non-implantable devices. Specialty Clinics provide focused perioperative patient care that emphasize regimented protocols for treatment. The Rehabilitation Centre also utilizes non-invasive bioelectric therapy; other uses include EMC and TENS (based simulation therapy) which are often involved in physical therapy and musculoskeletal recovery programs.

Home Care Settings are important to the industry because there is a demand for portable device and user-friendly medications and other devices for patients to assist them in managing their chronic conditions. TENS units or wearable stimulators are common in the home care setting

Neuromodulation has the largest market share through its use for chronic pain, epilepsy, depression, and movement disorders. Technologies for deep brain and spinal cord stimulation drive growth in this segment. Electrical Stimulation is widely implemented in both implantable and non-implantable settings for cardiac, muscle, and nerve stimulation.

Since many forms of Electrical Stimulation can be used, it is a ubiquitous market technology. Stretching the idea of neuromodulation, Electromagnetic Therapy is prominent, especially for musculoskeletal disorders as well as psychiatric disorders like depression – including an increasing usage of repetitive transcranial magnetic stimulation (rTMS) for treatment-resistant depression. Bioelectronic Implants are an emerging next-generation technology that offers not only sensing capabilities, but also feedback capabilities.

This opens new doors to modulating neural circuits with precision. In this stage of adoption, devices are still being innovated and studied in clinical trials with significant market opportunity. Closed-loop Systems (AI-Managed Devices) represent the future of bioelectric medicine. The concept depends on the premise that AI can use real-time data and data collected via machine learning to adjust stimulation parameters, which should improve patient outcomes while reducing the need for manual reprogramming.

While this segment is only beginning to emerge, experts expect rapid increases in both clinical and commercial application as AI technologies are further developed.

North America holds the largest market share of 41.2% in 2024, driven by the region’s strong focus on innovation, robust reimbursement frameworks, and high adoption of implantable bioelectric devices. The U.S. leads the market due to its advanced healthcare infrastructure and strong presence of leading device manufacturers such as Medtronic and Boston Scientific. High prevalence of neurological and cardiac disorders, along with an aging population and strong investment in neuromodulation technologies, continue to bolster demand. Favorable FDA approvals and rapid integration of AI in closed-loop systems further contribute to the market’s dominance in this region.

Europe holds the second-largest share in the global bioelectric medicine market, accounting for xx% in 2024. Countries such as Germany, France, the UK, and the Netherlands are at the forefront of adopting advanced bioelectronic therapies, particularly for chronic pain, epilepsy, and cardiac conditions. The region’s aging population and government-funded healthcare systems support widespread usage of both implantable and non-implantable devices. Additionally, ongoing clinical trials and academic research from institutions across Scandinavia and Central Europe are accelerating innovation in bioelectronic medicine.

The Asia-Pacific region is projected to grow at the fastest CAGR of 8.1% during the forecast period. While the current market share stands at 18.5% in 2024, rapid urbanization, increasing healthcare expenditure, and growing awareness of neurostimulation therapies are driving strong market expansion. China and Japan are the largest markets in the region, with India showing rapid growth due to rising cases of neurological disorders and growing access to specialized care. Government initiatives to modernize healthcare systems and increased availability of wearable bioelectric devices are also contributing to the region’s momentum.

Latin America and the Middle East & Africa regions together hold a modest market share of xx% in 2024. Countries such as Brazil, Mexico, Saudi Arabia, and South Africa are showing increased interest in neuromodulation and electroceutical therapies. Growth is being driven by rising healthcare investments, growing burden of chronic diseases, and gradual improvements in medical infrastructure. However, market expansion in these regions is restrained by economic disparities, uneven access to advanced medical technologies, and limited specialist availability. Continued foreign investment and public-private healthcare partnerships are expected to stimulate future growth.

The bioelectric medicine market was valued at USD 23.4 billion in 2024.

The bioelectric medicine market is projected to grow at a CAGR of 4.9% from 2025 to 2033.

Implantable devices hold the largest bioelectric medicine market share.

The Asia-Pacific region is expected to witness the highest growth rate.

Major players include Teva Pharmaceutical Industries Ltd, Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Cochlear Ltd.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Bioelectric Medicine Market, By Product Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Bioelectric Medicine Market, By Application

5.3 Bioelectric Medicine Market, By End-User

5.4 Bioelectric Medicine Market, By Technology

6.1 North America Bioelectric medicine market, By Country

6.1.1 Bioelectric medicine market, By Product Type

6.1.2 Bioelectric medicine market, By Application

6.1.3 Bioelectric medicine market, By End-User

6.1.4 Bioelectric medicine market, By Technology

6.2 U.S.

6.2.1 Bioelectric medicine market, By Product Type

6.2.2 Bioelectric medicine market, By Application

6.2.3 Bioelectric medicine market, By End-User

6.2.4 Bioelectric medicine market, By Technology

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America