Staple Fibres Market

Staple Fibres Market Share & Trends Analysis Report, By Fibre Type (Synthetic, Cellulose, Regenerated), By Application (Apparel, Home Textiles, Automotive, Filtration, Hygiene, Construction, Others), By End User (Textile Industry, Automotive, Personal Care, Construction, Others) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 5.0%

Last Updated : November 29, 2025

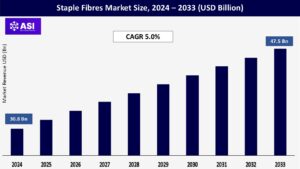

The global market for staple fibres was approximately valued at USD 30.8 billion in 2024 and is anticipated to reach USD 47.5 billion by 2033, with a compound annual growth rate (CAGR) of 5.0% expected during the forecast period from 2025 to 2033.

Staple fibres are defined as short-length textile fibres that can be combined to create yarns. These fibres are extensively utilized in various textile applications due to their adaptability, durability, and ease of blending. They are classified into three categories: natural, synthetic, and regenerated fibres, with synthetic staple fibres—such as polyester and acrylic—being the foremost due to their strength, moisture resistance, and cost-effectiveness. Staple fibres find widespread use in clothing, home furnishings, automotive textiles, industrial filtration, hygiene products, and insulation materials.

The growth of the market is mainly fueled by rising textile demand, population growth, increasing disposable income, and advancements in fibre engineering. Sustainable options like recycled and bio-based staple fibres are becoming increasingly popular, driven by heightened environmental concerns and supportive regulatory initiatives.

The staple fibres market is primarily propelled by the expansion of the worldwide textile and apparel sector, known for being one of the most fiber-demanding industries. Growing disposable incomes, rapid urbanization, and shifting fashion trends—particularly in Asia-Pacific, Latin America, and Africa—are driving the need for affordable, durable, and comfortable fabrics.

Synthetic staple fibres such as polyester and acrylic are prevalent because of their low price, strength, and ease of processing. The rising trend of blended fabrics for casualwear, activewear, and innerwear is also enhancing the usage of both synthetic and natural staple fibres.

Additionally, the emergence of fast fashion and global e-commerce platforms is speeding up production cycles, which in turn increases the global consumption of staple fibres.

Staple fibres play a crucial role in nonwoven fabrics, which are increasingly utilized in hygiene items, medical textiles, automotive parts, and filtration systems. Following the COVID-19 pandemic, there has been a surge in global demand for disposable products such as wipes, masks, gowns, and sanitary supplies, which has boosted the application of staple fibres in personal care and healthcare sectors.

Moreover, the significance of technical textiles in construction, automotive interiors, and geotextiles is rising, driven by urban development and environmental needs. These varied applications are broadening the market beyond conventional clothing, making staple fibres vital for both industrial and consumer uses.

A major limitation in the staple fibres market, especially for synthetic types like polyester and acrylic, is the increasing awareness regarding their environmental effects. These fibres are made from petroleum-based materials, are not biodegradable, and contribute to microplastic pollution in bodies of water and soil, raising concerns among both regulators and consumers.

Governments in various regions, particularly in Europe and North America, are implementing stringent environmental regulations aimed at minimizing plastic waste and carbon emissions within the textile sector.

Consequently, manufacturers are facing pressure to shift towards environmentally friendly alternatives, such as recycled or bio-based fibres, which tend to be pricier and less readily accessible.

Moreover, the recycling infrastructure for synthetic fibres remains underdeveloped in numerous areas, further hindering sustainability initiatives. These elements not only elevate production expenses but also complicate the ability of synthetic staple fibres to compete in a marketplace increasingly oriented towards environmentally responsible options.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Fibre Type |

Synthetic Cellulose Regenerated |

| By Application |

Apparel Home Textiles Automotive Filtration Hygiene Construction Others |

| By End User |

Textile Industry Automotive Personal Care Construction Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The staple fibres industry is categorized by fibre type (synthetic, cellulose, regenerated), application (apparel, home textiles, automotive, filtration, hygiene, construction), and end user (textile, automotive, personal care, construction). Synthetic fibres and apparel are at the forefront because of their cost-effectiveness, longevity, and increasing worldwide demand for textiles.

Synthetic fibers like polyester, polypropylene, and acrylic lead the market. These fibers are favored for their cost-effectiveness, strength, durability, and moisture-resistant properties, making them perfect for clothing, nonwoven products, and industrial uses.

Polyester staple fiber (PSF) commands the largest market share because of its versatility and ability to be recycled. Natural fibers, such as cotton and flax, fall under the category of cellulose fibers and are valued for their breathability, softness, and biodegradability.

They are primarily used in premium apparel, home textiles, and medical products. While they tend to be pricier than synthetic alternatives, their environmental benefits are driving increased demand for sustainable offerings.

Regenerated fibers, including viscose, modal, and lyocell, are created from natural cellulose through chemical methods. They offer a combination of comfort, sheen, and moisture-wicking capabilities, making them ideal for fashion, personal care, and home textiles. As the market shifts towards biodegradable options, the popularity of regenerated fibers is on the rise.

Apparel This is the largest segment, fueled by the worldwide demand for casual clothing, athletic wear, and trendy garments. Home Textiles Comprises items such as carpets, curtains, upholstery, and bed linens, incorporating both synthetic and natural fibers.

Automotive Utilized for seat coverings, sound insulation, and trunk linings, providing a lightweight, noise-dampening, and durable solution. Filtration Staple fibers are integral to air and liquid filtration systems utilized in industrial, medical, and environmental applications.

Hygiene Products: Crucial in the production of diapers, wipes, sanitary napkins, and face masks, especially in the aftermath of the pandemic. Construction Used in insulation materials, roofing felts, and geotextiles to offer reinforcement and protective functions.

Textile Sector The major user, employing staple fibers in textiles, clothing, and fabrics. Automotive Industry Utilizes functional fibers for interior components and safety features. Personal Care Sector Relies on nonwoven materials for hygiene products and medical supplies.

Construction Field Gradually incorporates fiber-reinforced materials for infrastructure projects and eco-friendly buildings. Other Industries Encompasses agriculture, packaging, and industrial textile applications.

North America constitutes a mature yet progressively changing market for staple fibres, primarily led by the United States and Canada. The demand in this region is spurred by the textile, personal care, and automotive industries, where staple fibres find extensive applications in nonwoven hygiene products, filtration systems, insulation materials, and interior components.

Growing awareness regarding sustainability and circular economy objectives is promoting a transition from virgin synthetic fibres to recycled and bio-based options.

The U.S. is experiencing significant growth in the utilization of staple fibres in eco-friendly clothing, automotive textiles, and medical disposables, bolstered by investments in recycling infrastructure and sustainable fashion initiatives. Nevertheless, high production expenses and dependence on imports from Asia pose challenges to domestic competitiveness.

Europe has a long-standing market for staple fibers that emphasizes quality, sustainability, and innovation. Leading countries like Germany, France, Italy, and the UK are pioneers in incorporating staple fibers into technical textiles, nonwoven hygiene items, and fashion fabrics.

The European Union’s ambitious Green Deal, targets for waste reduction, and bans on plastics are encouraging the use of regenerated and natural fibers in place of traditional synthetics. There is a growing acceptance of recycled polyester and cellulosic fibers in both industrial and consumer markets.

Additionally, the region benefits from a highly integrated textile manufacturing network and advanced research and development in fiber blending, dyeing, and eco-friendly processing technologies. Demand in sectors such as construction, filtration, and automotive is increasing due to regulatory compliance and growth driven by innovation.

The staple fibres market is heavily dominated by the Asia-Pacific region in terms of both production and consumption. Prominent countries such as China, India, Bangladesh, Vietnam, and Indonesia are significant players in global textile manufacturing and major exporters of products made from staple fibres.

China, in particular, plays a crucial role in worldwide synthetic fibre production, with polyester being the primary focus. On the other hand, India is experiencing rapid growth in both natural and regenerated fibres, bolstered by initiatives like the Production-Linked Incentive (PLI) Scheme for textiles.

The increasing population, rising disposable incomes, and heightened demand for clothing, hygiene goods, and automotive textiles are driving market expansion. Furthermore, Asia-Pacific’s strong market position is supported by low labor costs, plenty of raw materials, and growing investments in nonwoven and technical textile production facilities.

Latin America is a developing market for staple fibers, primarily driven by Brazil, Mexico, Argentina, and Colombia. The region’s textile and garment sectors are growing gradually, bolstered by increasing domestic demand and regional trade dynamics.

Staple fibers play a role in apparel, home textiles, and hygiene products, with a rising interest in environmentally friendly options. Nevertheless, growth is tempered by economic fluctuations, limited local production abilities, and reliance on imports.

Despite these obstacles, there is potential for future growth in the region, particularly as infrastructure advances and sustainable practices become more prevalent in fashion and nonwoven sectors.

The Middle East and Africa (MEA) represent an emerging yet expanding market for staple fibres. Nations like South Africa, Egypt, the UAE, and Saudi Arabia are experiencing rising demand in sectors such as construction, personal care, and automotive.

Staple fibres are increasingly utilized in applications like insulation, geotextiles, wipes, and nonwoven fabrics, fueled by urbanization and population increases. Initiatives aimed at localizing textile production, decreasing reliance on imports, and embracing sustainable building materials are contributing to market growth.

Nevertheless, limited production capabilities and supply chain challenges continue to pose significant obstacles to swift advancement.

In 2024, the market was worth USD 76.4 billion.

From 2025 to 2033, the market is anticipated to expand at a compound annual growth rate (CAGR) of 6.5%.

The largest market share is held by the Synthetic Fibres segment.

The region with the highest growth rate is anticipated to be Asia-Pacific.

Grasim Industries, Lenzing AG, Reliance Industries, Toray Industries, and Indorama Ventures are some of the major participants.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Staple Fibres Market, By Fibre Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Staple Fibres Market, By Application

5.3 Staple Fibres Market, By End User

6.1 North America Staple Fibres Market , By Country

6.1.1 Staple Fibres Market, By Fibre Type

6.1.2 Staple Fibres Market, By Application

6.1.3 Staple Fibres Market, By End User

6.2 U.S.

6.2.1 Staple Fibres Market, By Fibre Type

6.2.2 Staple Fibres Market, By Application

6.2.3 Staple Fibres Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping