Anticoagulation Market

Anticoagulation Market Share & Trends Analysis Report, By Drug Class (Direct Oral Anticoagulants (DOACs), Heparin & Low Molecular Weight Heparin (LMWH), Vitamin K Antagonists), By Route of Administration (Oral, Injectable), By Application (Atrial Fibrillation, Deep Vein Thrombosis, Pulmonary Embolism, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End User (Hospitals, Clinics, Homecare, Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

CAGR: 8.30%

Last Updated : November 15, 2025

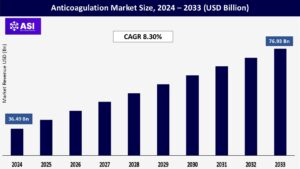

The global anticoagulation market size was valued at approximately USD 36.49 billion in 2024 and is projected to reach USD 76.93 billion by 2033, growing at a CAGR of 8.30% during the forecast period (2025–2033).

The anticoagulation market involves a worldwide industry focused on medications that prevent and treat blood clots. Commonly known as blood thinners, these drugs are used to reduce the risk of serious health issues such as strokes, deep vein thrombosis (DVT), and pulmonary embolism (PE). They are particularly beneficial for individuals with conditions like atrial fibrillation (an irregular heartbeat), mechanical heart valves, or a past history of clotting problems.

Anticoagulants work by reducing the blood’s tendency to clot too much either by blocking certain clotting substances or by stopping platelets from clumping together. These medications support healthy blood flow while still allowing the body to form necessary clots when injured. Available in various forms, including tablets and injections, they differ in how long they remain active in the body. The market for these drugs continues to grow, driven by an increase in cardiovascular diseases, aging populations, and the development of newer options like direct oral anticoagulants (DOACs), which offer greater safety and ease of use compared to older treatments such as warfarin.

Cardiovascular diseases (CVDs) such as atrial fibrillation, heart attacks, strokes, and venous thromboembolism (VTE), including deep vein thrombosis (DVT) and pulmonary embolism (PE), are on the rise globally due to unhealthy diets, sedentary lifestyles, smoking, and stress.

These conditions significantly increase the risk of dangerous blood clots. Anticoagulants are a cornerstone in preventing and managing these diseases by reducing clot formation and lowering the chances of complications like stroke or sudden death. As the global burden of CVDs continues to grow, the demand for anticoagulant therapies increases, driving market expansion.

The elderly are at a much higher risk of developing blood clot-related conditions due to age-related changes in blood circulation, decreased physical activity, and a higher likelihood of having comorbidities such as hypertension, diabetes, and heart disease.

As the global population ages, especially in developed countries, there is a growing patient base in need of long-term anticoagulant therapy. This demographic trend is a major driver of market growth, as older adults often require regular anticoagulation to prevent stroke, DVT, and other serious complications, contributing to the sustained demand for both traditional and newer anticoagulant drugs.

The significant market restraint for the anticoagulation market is the risk of bleeding complications associated with anticoagulant therapy. While anticoagulants are effective in preventing harmful blood clots, they also increase the risk of excessive bleeding, which can range from minor bruising to life-threatening hemorrhages, including gastrointestinal or intracranial bleeding.

This risk often causes hesitation among physicians and patients, particularly in elderly populations or those with underlying health issues. Managing the balance between preventing clots and avoiding bleeding is complex and requires close monitoring, especially with traditional anticoagulants like warfarin, which need regular blood tests and dose adjustments.

Even newer anticoagulants, such as DOACs, though considered safer, still carry bleeding risks and may not be suitable for all patients. This safety concern limits widespread use and adoption, particularly in patients with a high bleeding risk or those taking multiple medications, thereby restraining the overall growth of the anticoagulation market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Class |

Direct Oral Anticoagulants (DOACs) Heparin & Low Molecular Weight Heparin (LMWH) Vitamin K Antagonists |

| By Route of Administration |

Oral Injectable |

| By Application |

Atrial Fibrillation Deep Vein Thrombosis Pulmonary Embolism Others |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies |

| By End User |

Hospitals Clinics Homecare Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Anticoagulation Market is segmented by Drug class, Route of administration, Application, Distribution Channels and End User. Each factor plays a crucial role in enhancing patient safety, increasing the adoption of anticoagulant therapies, and supporting the development of more effective and convenient treatment options in the management of thromboembolic and cardiovascular conditions.

Direct Oral Anticoagulants (DOACs) DOACs, such as apixaban, rivaroxaban, dabigatran, and edoxaban, have rapidly gained market share due to their fixed dosing, minimal need for monitoring, and lower risk of major bleeding compared to traditional drugs. These medications are often preferred for stroke prevention in atrial fibrillation and for treating or preventing venous thromboembolism. Heparin & Low Molecular Weight Heparin (LMWH) These are injectable anticoagulants commonly used in hospital settings for short-term treatment or surgical prophylaxis.

LMWH, such as enoxaparin, offers more predictable pharmacokinetics and lower bleeding risk compared to unfractionated heparin. Vitamin K Antagonists (VKAs) Warfarin is the most widely used VKA. Though effective, it requires regular INR monitoring and has dietary and drug interaction issues. Its use is declining due to the rise of DOACs, but it remains essential for certain conditions like mechanical heart valves.

Oral anticoagulants, especially DOACs and warfarin, dominate outpatient and long-term therapy. They are preferred due to ease of administration, better compliance, and fewer hospital visits. Injectable anticoagulants, including heparin and LMWH, are widely used in acute care, surgical settings, and initial treatment phases. They offer rapid onset and are often used when oral therapy is not feasible.

Atrial Fibrillation (AF) One of the largest application areas, as AF significantly increases stroke risk. Long-term anticoagulation is a standard treatment to prevent thromboembolic events in AF patients. Deep Vein Thrombosis (DVT) Anticoagulants are critical in preventing and treating DVT, especially in post-surgical and immobile patients.

Early treatment reduces the risk of clot extension and pulmonary embolism. Pulmonary Embolism (PE) PE is a serious condition often resulting from untreated DVT. Anticoagulants play a key role in both acute management and secondary prevention of PE recurrence. Others Includes prevention of clotting during dialysis, management of clotting disorders like antiphospholipid syndrome, and use in orthopedic surgeries.

Hospital Pharmacies A major distribution channel for injectable anticoagulants and medications used during inpatient care. Hospitals are the primary sites for acute treatment initiation. Retail Pharmacies Account for a large share of oral anticoagulant distribution, especially for patients on long-term treatment. Accessibility and convenience drive this segment. Online Pharmacies A growing channel, especially in developed regions, due to increased digital adoption and home delivery services. Useful for chronic users of oral anticoagulants.

Hospitals The primary setting for initiating anticoagulant therapy, especially injectables. Hospitals also handle emergency cases like PE or stroke where rapid anticoagulation is critical. Clinics Used for ongoing patient management, monitoring, and follow-ups. DOACs have increased clinic-based treatment options due to reduced monitoring needs.

Homecare An expanding area, driven by the shift to outpatient care and the use of oral anticoagulants that don’t require regular monitoring or injections. Others Includes diagnostic centers, rehabilitation centers, and nursing homes where anticoagulant therapy may be managed as part of broader care services.

North America holds the largest share of the global anticoagulant market, primarily driven by the high prevalence of cardiovascular diseases, well-established healthcare infrastructure, and the widespread adoption of advanced therapies like Direct Oral Anticoagulants (DOACs).

The U.S. is the leading country in this region due to strong regulatory support, rising awareness about stroke prevention in atrial fibrillation, and high healthcare spending. Additionally, the presence of key market players and ongoing R&D activities contribute to market growth. Increasing demand for minimally monitored anticoagulants also fuels the shift toward DOACs in outpatient care.

Europe is a significant market for anticoagulants, with countries like Germany, the UK, France, and Italy showing high demand. The region benefits from an aging population and a high incidence of thromboembolic disorders, especially among elderly patients.

Government-funded healthcare systems and broad insurance coverage support the adoption of both traditional and newer anticoagulants. Moreover, efforts to reduce stroke risk and improve post-operative care contribute to steady market growth. Regulatory agencies like the EMA (European Medicines Agency) promote the use of safer and more effective anticoagulant therapies, boosting innovation in this space.

The Asia-Pacific anticoagulant market is growing rapidly, driven by a large and aging population, rising incidence of cardiovascular and lifestyle-related diseases, and improving access to healthcare. Countries like China, India, Japan, and South Korea are witnessing increasing demand for anticoagulant therapy, especially DOACs, due to urbanization, increased health awareness, and economic development.

Government initiatives to enhance healthcare infrastructure and insurance coverage are also encouraging market growth. However, cost sensitivity and limited access in rural areas can pose challenges. Japan leads in innovation and early adoption, while India and China are significant in terms of patient volume.

In Latin America, the anticoagulant market is expanding steadily, with Brazil, Mexico, and Argentina being key contributors. The growing burden of non-communicable diseases, such as hypertension and diabetes, is increasing the risk of thrombotic events and driving the demand for anticoagulants.

While healthcare access and spending are more limited than in developed regions, public health programs and increased use of generics are helping to boost accessibility. The uptake of DOACs is slower due to cost concerns, but hospital use of traditional anticoagulants like heparin and warfarin remains common.

The Middle East & Africa region represents a smaller but growing segment of the anticoagulant market. Urbanization, changes in lifestyle, and an increasing incidence of heart diseases and stroke are raising the need for anticoagulant therapies. Countries like Saudi Arabia, the UAE, and South Africa are leading in adoption due to better healthcare infrastructure and rising health awareness.

However, challenges such as limited access in rural areas, cost barriers, and a shortage of trained healthcare professionals can hinder broader adoption. International aid and government initiatives to improve healthcare delivery are helping to drive market penetration.

The anticoagulation market was valued at USD 36.49 billion in 2024.

The anticoagulation market is projected to grow at a CAGR of 8.30% from 2025 to 2033.

The Direct Oral Anticoagulants (DOACs) hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Bristol-Myers Squibb Company, Pfizer Inc. and Bayer AG.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Anticoagulation Market, By Drug Class

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Anticoagulation Market, By Route of Administration

5.3 Anticoagulation Market, By Application

5.4 Anticoagulation Market, By Distribution Channel

5.5 Anticoagulation Market, By End User

6.1 North America Anticoagulation Market , By Country

6.1.1 Anticoagulation Market, By Drug Class

6.1.2 Anticoagulation Market, By Route of Administration

6.1.3 Anticoagulation Market, By Application

6.1.4 Anticoagulation Market, By Distribution Channel

6.1.5 Anticoagulation Market, By End User

6.2 U.S.

6.2.1 Anticoagulation Market, By Drug Class

6.2.2 Anticoagulation Market, By Route of Administration

6.2.3 Anticoagulation Market, By Application

6.2.4 Anticoagulation Market, By Distribution Channel

6.2.5 Anticoagulation Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping