Antiepileptic Drugs (AED) Market

Antiepileptic Drugs (AED) Market Share & Trends Analysis Report, By Drug Generation (First Gen AEDs, Second Gen AEDs, Third Gen AEDs), By Route of Administration (Oral, Intravenous, Intramuscular), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Drug Stores), By Seizure Type (Focal Seizures, Generalized Seizures, Non-Epileptic Seizures), By End-User (Hospitals, Clinics, Ambulatory Care Centers, Home Setting)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

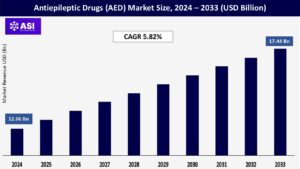

CAGR: 5.82%

Last Updated : December 16, 2025

The global Antiepileptic Drugs (AED) Market size was valued at approximately USD 12.06 billion in 2024 and is projected to reach USD 17.44 billion by 2033, growing at a CAGR of 5.82% during the forecast period (2025–2033).

The Antiepileptic Drugs (AED) Market refers to the global industry involved in the research, development, production, and distribution of medications used to manage and treat epilepsy and other seizure-related neurological disorders. These drugs are designed to stabilize neuronal activity in the brain by altering neurotransmitter levels or blocking ion channels that cause hyperexcitability, thus preventing or reducing the frequency and intensity of seizures.

Antiepileptic drugs are used for various forms of epilepsy, including generalized and focal seizures, as well as for off-label uses such as mood stabilization, neuropathic pain management, and migraine prevention. Key properties of AEDs include their mechanism of action (such as GABA enhancement or sodium/calcium channel blockade), pharmacokinetics, tolerability, safety profile, and potential for drug-drug interactions. The market is driven by the rising prevalence of epilepsy, increasing awareness, the introduction of novel therapies, and ongoing research in neuropharmacology. However, it also faces challenges such as high treatment costs, side effects like drowsiness or cognitive impairment, and the need for personalized medication regimens.

One of the primary drivers of the AED market is the increasing global incidence and prevalence of epilepsy and other seizure-related neurological conditions. According to the World Health Organization (WHO), approximately 50 million people worldwide suffer from epilepsy, making it one of the most common neurological diseases.

The condition is more prevalent in low- and middle-income countries due to factors such as perinatal injury, infections, and limited access to healthcare. The growing patient population is creating a sustained demand for effective antiepileptic therapies, pushing pharmaceutical companies to develop improved drugs with better efficacy and fewer side effects.

Ongoing innovation in neuropharmacology and biotechnology is driving the development of next-generation AEDs with targeted mechanisms of action, improved safety profiles, and extended release formulations.

Drug approvals by regulatory bodies like the FDA and EMA for novel compounds such as cenobamate, brivaracetam, and cannabidiol-based medications (e.g., Epidiolex) have expanded treatment options, particularly for drug-resistant epilepsy. This trend of introducing innovative treatments, including precision medicine and gene-targeted therapies, is fueling market growth by addressing unmet clinical needs.

A major restraint in the Antiepileptic Drugs market is the high incidence of adverse effects and the challenge of drug resistance, particularly among patients with refractory or drug-resistant epilepsy. Many AEDs are associated with significant side effects such as dizziness, fatigue, weight gain, cognitive impairment, mood changes, and even serious allergic reactions or liver toxicity.

These side effects often lead to poor patient compliance and discontinuation of therapy. Additionally, about 20–30% of epilepsy patients do not respond adequately to current medications, leading to treatment-resistant epilepsy, which severely limits the efficacy of existing drugs. The lack of highly effective and well-tolerated treatments for all patient populations hampers overall market growth and highlights the need for more personalized and innovative therapeutic solutions.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Drug Generation |

First Gen AEDs Second Gen AEDs Third Gen AEDs |

| By Route of Administration |

Oral Intravenous Intramuscular |

| By Distribution Channel |

Hospital Pharmacies Retail Pharmacies Online Pharmacies Drug Stores |

| By Seizure Type |

Focal Seizures Generalized Seizures Non-Epileptic Seizures |

| By End-User |

Hospitals Clinics Ambulatory Care Centers Home Setting |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Antiepileptic Drugs (AED) Market is segmented by Drug Generation, Route of administration, Distribution Channels, Seizure Type and End User. Each factor rising disease prevalence, advances in drug innovation, and increased awareness plays a crucial role in improving treatment outcomes, enhancing patient quality of life, and promoting the development and accessibility of safer, more effective antiepileptic therapies.

These dynamics are collectively driving the expansion of the AED market while addressing the unmet needs in the management of epilepsy and seizure-related neurological disorders.

The market is categorized into First-Generation AEDs, such as phenytoin and valproate, which are widely used but often associated with significant side effects and drug interactions; Second-Generation AEDs, including lamotrigine and levetiracetam, which offer improved safety profiles and fewer interactions; and Third-Generation AEDs, such as lacosamide and brivaracetam, which are more recent innovations designed to treat refractory epilepsy with better precision and tolerability.

Segment is dominated by the oral route, preferred for its convenience and long-term use in chronic epilepsy management. Intravenous (IV) and intramuscular (IM) routes are used in acute care settings, particularly during seizures or for patients unable to take oral medication.

Hospital pharmacies lead due to the critical nature of seizure treatment and the need for immediate drug availability, especially in emergency departments. Retail pharmacies and drug stores cater to outpatient and chronic care needs, while online pharmacies are witnessing rapid growth due to convenience and increased access to medications in remote areas.

In terms of Seizure Type, focal seizures account for a large market share, as they are more commonly diagnosed and treated. Generalized seizures, which affect both hemispheres of the brain, also represent a significant segment, often requiring long-term therapy. Non-epileptic seizures, though less common, are increasingly recognized and treated with AEDs in complex neurological cases.

Hospitals dominate the market due to their role in initial diagnosis and emergency seizure management. Clinics and ambulatory care centers provide follow-up and outpatient services, while the home setting is gaining traction with the rise of chronic epilepsy management through patient-friendly oral formulations and telehealth support.

Each of these segments plays a critical role in shaping the evolving landscape of the AED market, driven by a focus on precision treatment, patient-centric care, and enhanced drug accessibility.

North America holds the largest share of the Antiepileptic Drugs (AED) market, driven by a high prevalence of epilepsy, advanced healthcare infrastructure, and strong awareness about neurological disorders. The United States leads the region with significant investment in neurological research, supportive reimbursement policies, and a high rate of adoption of novel therapies such as cannabidiol-based AEDs.

Regulatory support from the FDA for orphan drugs and fast-track approval processes also accelerates the availability of advanced treatment options. In addition, the presence of leading pharmaceutical companies and extensive clinical trial activity contribute to North America’s dominance in this market.

Europe represents a mature and steadily growing AED market, supported by well-established healthcare systems and increasing diagnosis rates of epilepsy. Countries like Germany, the UK, and France are at the forefront, owing to robust medical infrastructure and proactive neurological care programs.

The European Medicines Agency (EMA) plays a key role in drug approvals, and there is growing interest in non-conventional therapies and combination treatments. However, budget constraints and varying drug reimbursement policies across EU nations sometimes pose challenges to market expansion. Increased focus on personalized medicine and public health campaigns to reduce epilepsy stigma further support regional growth.

The Asia-Pacific region is expected to exhibit the highest growth rate in the coming years due to a large patient pool, rising awareness of neurological disorders, and expanding healthcare access in emerging economies. Countries like China, India, and Japan are witnessing a surge in demand for antiepileptic medications due to increasing healthcare expenditures, urbanization, and improving diagnosis capabilities.

Japan stands out with its aging population and advanced medical systems, while China and India present immense market potential due to their large populations and government-led health initiatives. However, underdiagnosis and lack of specialist care in rural areas remain challenges.

Latin America’s AED market is growing steadily, driven by improvements in healthcare access and the rising burden of neurological disorders. Brazil and Mexico are the major contributors due to better hospital infrastructure and a growing middle-class population seeking specialized care.

However, access to newer and branded antiepileptic drugs is still limited by affordability and regulatory hurdles. Efforts by public health agencies and NGOs to raise epilepsy awareness are helping to reduce the social stigma associated with the condition and are gradually increasing treatment rates across the region.

The Middle East & Africa region holds a relatively smaller share of the global AED market, primarily due to limited healthcare infrastructure, lower diagnosis rates, and social stigma around neurological disorders.

However, countries like Saudi Arabia, the UAE, and South Africa are investing more in healthcare modernization and are expanding access to neurological care. Increasing government initiatives, partnerships with global pharmaceutical firms, and better availability of generic drugs are supporting growth. Nonetheless, significant disparities in care and limited specialist availability in rural and underdeveloped areas continue to restrain full market potential.

The market was valued at USD 12.06 billion in 2024.

The market is projected to grow at a CAGR of 5.82% from 2025 to 2033.

First Gen AEDs hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Pfizer Inc., UCB Pharma and GlaxoSmithKline plc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Antiepileptic Drugs (AED) Market, By Drug Generation

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Antiepileptic Drugs (AED) Market, By Route of Administration

5.3 Antiepileptic Drugs (AED) Market, By Distribution Channel

5.4 Antiepileptic Drugs (AED) Market, By Seizure Type

5.5 Antiepileptic Drugs (AED) Market, By End-User

6.1 North America Antiepileptic Drugs (AED) Market , By Country

6.1.1 Antiepileptic Drugs (AED) Market, By Drug Generation

6.1.2 Antiepileptic Drugs (AED) Market, By Route of Administration

6.1.3 Antiepileptic Drugs (AED) Market, By Distribution Channel

6.1.4 Antiepileptic Drugs (AED) Market, By Seizure Type

6.1.5 Antiepileptic Drugs (AED) Market, By End-User

6.2 U.S.

6.2.1 Antiepileptic Drugs (AED) Market, By Drug Generation

6.2.2 Antiepileptic Drugs (AED) Market, By Route of Administration

6.2.3 Antiepileptic Drugs (AED) Market, By Distribution Channel

6.2.4 Antiepileptic Drugs (AED) Market, By Seizure Type

6.2.5 Antiepileptic Drugs (AED) Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping