Bed Head Panel Market

Bed Head Panel Market Share & Trends Analysis Report, By Configuration (Vertical Panels, Horizontal Panels), By Specialty Type (ICU, Surgical, Other Specialties (e.g., emergency, general wards, pediatrics)), By Material/Panel Type (Upholstered, Hardboard, Metal, Glass, Plastic), By Attachment Type (Wall‑Mounted, Free‑Standing, Headboard with Storage), By End‑User (Hospitals, Clinics, Other End‑Users (e.g., nursing homes, ambulatory centers))–Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

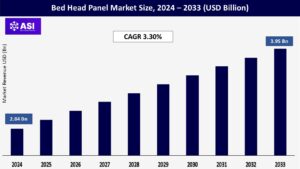

CAGR: 3.30%

Last Updated : December 16, 2025

The global bed head panel market size was valued at approximately USD 2.84 billion in 2024 and is projected to reach USD 3.95 billion by 2033, growing at a CAGR of 3.30% during the forecast period (2025–2033).

The bed head panel market refers to the segment of the healthcare infrastructure industry that deals with wall-mounted medical panels installed near hospital beds. These panels integrate multiple hospital services such as medical gas outlets (oxygen, air, and vacuum), nurse call systems, lighting, electrical sockets, and data communication points.

They are extensively used in intensive care units (ICUs), emergency departments, recovery rooms, and patient wards to streamline and centralize access to critical utilities. The key properties of bed head panels include durability, modularity, space-saving design, corrosion resistance, and ease of installation and maintenance. They help improve patient safety and clinical efficiency by minimizing clutter and ensuring immediate availability of life-supporting systems.

The increasing construction and renovation of hospitals and specialty clinics worldwide, particularly in emerging economies, are driving demand for advanced hospital equipment. Bed head panels are integral to patient rooms, ICUs, and emergency units, offering a centralized system for medical gases, power outlets, and communication ports.

As governments and private sectors invest heavily in hospital infrastructure to improve healthcare delivery, the installation of modern, modular bed head panels becomes a standard requirement.

Healthcare facilities are prioritizing equipment that improves operational workflow and minimizes hazards. Bed head panels help in organizing essential utilities and reduce cable clutter, thus lowering the risk of tripping, fire hazards, and delayed response times during emergencies. Their integration with nurse call systems and medical gas supply lines also enhances patient monitoring and safety, leading to increased adoption in both new and upgraded medical facilities.

One major restraint in the Bed Head Panel Market is the high initial cost of installation and customization, especially in small- to medium-sized healthcare facilities. These panels often need to be tailored to the specific infrastructure of each hospital, including integration with oxygen, vacuum, lighting, power supply, and communication systems.

The cost of materials such as aluminum, stainless steel, and antibacterial coatings further adds to the expense. Additionally, specialized labor is required for installation, increasing total project costs. For underfunded public hospitals or rural healthcare centers, these costs can be prohibitive, thus limiting widespread adoption, particularly in developing regions.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Configuration |

Vertical Panels Horizontal Panels |

| By Specialty Type |

ICU Surgical Other Specialties (e.g., emergency, general wards, pediatrics) |

| By Material/Panel Type |

Upholstered Hardboard Metal Glass Plastic |

| By Attachment Type |

Wall‑Mounted Free‑Standing Headboard with Storage |

| By End-User |

Hospitals Clinics Other End‑Users (e.g., nursing homes, ambulatory centers) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The bed head panel market is segmented by Configuration, Specialty Type, Material Type, Attachment Type and End User. Each factor plays a crucial role in modernizing hospital infrastructure, improving patient safety, and streamlining the delivery of critical care services. The integration of essential utilities into a single, modular unit enhances clinical efficiency, reduces response time in emergencies, and creates a safer and more organized treatment environment.

Vertical liposuction devices are compact systems designed for space efficiency, often featuring a tower-like structure with stacked components like suction motors, canisters, and infiltration systems. These are ideal for smaller clinics or ambulatory surgical centers with limited space.

Horizontal liposuction systems, in contrast, are typically used in larger surgical suites where extended work surfaces and easy access to multiple components (like tumescent fluid systems, cannula trays, and integrated ultrasound modules) are needed. These configurations often offer more ergonomic layouts for multi-step procedures and simultaneous use of dual operators.

ICU Liposuction devices are rarely used directly in ICUs, but in rare cases like necrotic fat removal or for managing severe lipodystrophy, ICU settings may employ compact, minimally invasive liposuction equipment for therapeutic interventions.

Surgical Units The primary users of liposuction systems, surgical departments—especially in plastic surgery, general surgery, and bariatrics—rely on these devices for procedures ranging from cosmetic body contouring to reconstructive fat transfer and lymphedema reduction.

Other Specialties In emergency units, liposuction tools might be used during trauma interventions involving hematoma evacuation. In pediatrics, highly specialized equipment is used in rare congenital or obesity-related fat deposit cases. The general wards are less involved in direct usage but support pre- and post-operative care for liposuction patients.

Metal Devices Most cannulas and durable core components (e.g., stainless steel aspirators) are made from medical-grade metals due to their strength and sterilizability. Plastic Many tubing systems and canisters are made from disposable or autoclavable plastic materials to ensure hygiene and reduce cross-contamination.

Glass Occasionally used in high-precision suction jars or for laser fiber tips in laser-assisted liposuction, though it’s less common due to fragility. Upholstered/Hardboard Not directly applicable to device function but may apply to the housing or console design in high-end clinic settings, where patient experience is prioritized.

Upholstered exteriors may be used on patient-supporting platforms in aesthetic centers. Composite Designs Many systems integrate multiple materials (metal framework, plastic interfaces, glass accessories) to balance performance, cost, and safety.

Wall-Mounted Systems Rare but used in fixed surgical rooms for integrated suction systems. These are often seen in teaching hospitals or high-end facilities with permanent setups. Free-Standing Devices The most common configuration.

These mobile systems are wheeled, compact, and allow for easy positioning during procedures, offering flexibility for use in multiple operating rooms. Integrated Units Some advanced systems are built into surgical chairs or treatment stations with built-in cannula holders, fluid containers, and infiltration systems, creating a streamlined, all-in-one surgical environment. These are popular in private cosmetic clinics.

Hospitals Utilize liposuction devices not only for cosmetic procedures but also for reconstructive, therapeutic, or post-traumatic interventions. Large-scale hospitals often invest in multi-functional systems. Clinics Aesthetic and dermatology clinics represent the largest market segment.

They prefer devices that are portable, efficient, and tailored for elective procedures with high patient throughput. Other End-Users Ambulatory surgical centers are increasingly investing in portable and cost-effective liposuction units to offer outpatient body contouring services. Nursing homes may rarely use liposuction in specific elderly care treatments, such as treating lipomas or severe edema, though this is uncommon.

Holds a significant share of the Bed Head Panel Market due to its advanced healthcare infrastructure, high investments in hospital renovation, and stringent patient safety regulations. The U.S. sees widespread adoption in ICU and emergency care settings, with increasing integration of smart panels with nurse call systems and monitoring tools.

Mature market driven by modernization of healthcare facilities and strong regulatory frameworks for hospital safety. Countries like Germany, France, and the UK are investing heavily in modular hospital setups, boosting the demand for customizable and corrosion-resistant bed head panels.

The fastest-growing region, fueled by rapid urbanization, growing hospital construction, and government healthcare expansion in countries such as China, India, and Japan. The increasing number of private hospitals and rising awareness about patient safety are accelerating market growth.

Witnessing moderate growth. Brazil and Mexico are key contributors, supported by improving healthcare access and investment in hospital infrastructure upgrades, although budget constraints in public healthcare may limit rapid adoption.

Experiencing gradual growth, led by rising investments in healthcare infrastructure in Gulf countries such as the UAE and Saudi Arabia. However, limited healthcare spending in some African nations poses challenges to wider adoption.

The bed head panel market was valued at USD 2.84 billion in 2024.

The bed head panel market is projected to grow at a CAGR of 3.30% from 2025 to 2033.

The Vertical Panels hold the largest bed head panel market share.

The North America region is expected to witness the highest growth rate.

The Major players include Dragerwerk AG & Co. KGaA, Hill-Rom Holdings, Inc. and Amico Group of Companies.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Bed Head Panel Market, By Configuration

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Bed Head Panel Market, By Specialty Type

5.3 Bed Head Panel Market, By Material/Panel Type

5.4 Bed Head Panel Market, By Attachment Type

5.5 Bed Head Panel Market, By End-Users

6.1 North America Bed Head Panel Market, By Country

6.1.1 Bed Head Panel Market, By Configuration

6.1.2 Bed Head Panel Market, By Modality Type

6.1.3 Bed Head Panel Market, By Material/Panel Type

6.1.4 Bed Head Panel Market, By Attachment Type

6.1.5 Bed Head Panel Market, By End User

6.2 U.S.

6.2.1 Bed Head Panel Market, By Configuration

6.2.2 Bed Head Panel Market, By Specialty Type

6.2.3 Bed Head Panel Market, By Material/Panel Type

6.2.4 Bed Head Panel Market, By Attachment Type

6.2.5 Bed Head Panel Market, By End-User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping