Bone Grafts and Substitutes Market

Bone Grafts and Substitutes Market Share & Trends Analysis Report, By Material Type (Allograft (e.g., demineralized bone matrix), Synthetic (ceramics, polymers, bone morphogenetic proteins), Xenograft, Autograft), By Application (Spinal Fusion, Dental, Joint Reconstruction, Craniomaxillofacial, Foot & Ankle, Long Bone/Trauma), By End User (Hospitals, Specialty Clinics (orthopedic, dental, spine), Others)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

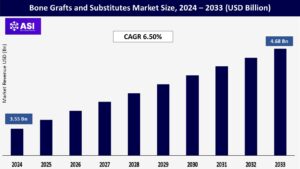

CAGR: 6.50%

Last Updated : December 16, 2025

The global Bone Grafts and Substitutes Market size was valued at approximately USD 3.55 billion in 2024 and is projected to reach USD 4.68 billion by 2033, growing at a CAGR of 6.50% during the forecast period (2025–2033).

The Bone Grafts and Substitutes Market refers to a specialized segment within the medical field that focuses on materials used to replace, repair, or regenerate damaged or missing bone tissue. These materials may be natural, such as autografts (taken from the patient’s own body), allografts (from human donors), or xenografts (from animal sources), as well as synthetic substitutes like ceramics, bioactive glass, and polymer-based composites.

Bone grafts are widely used in orthopedic surgeries, spinal fusions, dental implant procedures, trauma cases, and reconstructive surgeries to facilitate bone healing and regeneration. The most important properties of bone grafts include osteoconductivity (serving as a scaffold for bone growth), osteoinductivity (stimulating immature cells to develop into bone cells), and osteogenesis (contributing living bone-forming cells, especially in autografts).

These materials must be biocompatible to avoid rejection or immune response, mechanically stable to support bone structure, and in some cases, biodegradable so they can be naturally replaced by new bone tissue over time. Safety, sterility, and compatibility with the body are critical in all bone graft materials.

The rise in orthopedic procedures due to aging, sports injuries, and road traffic accidents is a major driver for the bone grafts and substitutes market. Surgeries like spinal fusion, hip replacement, fracture repair, and dental implants often require bone grafts to ensure structural support and bone regeneration.

Advancements in surgical techniques and the availability of specialized bone grafting products are further propelling this demand across hospitals and surgical centers.

Rapid innovation in synthetic and biologically engineered bone substitutes is transforming the market. New materials offer enhanced osteoconductivity, osteoinductivity, and resorption characteristics that mimic natural bone.

The emergence of biomaterials such as demineralized bone matrix (DBM), calcium phosphate ceramics, and recombinant human bone morphogenetic proteins (rhBMPs) has improved graft performance and patient outcomes, reducing the need for autografts and minimizing surgical complications. These technological improvements are driving adoption in both developed and emerging healthcare systems.

A major challenge in the bone grafts and substitutes market especially in the use of biological grafts like allografts (from human donors) and xenografts (from animals) is the risk of disease transmission and immune rejection.

Despite sterilization and rigorous donor screening, there remains a residual fear of transmitting infectious agents such as viruses or prions. Additionally, the body’s immune response can sometimes reject donor tissue, leading to inflammation, graft failure, or complications that require additional surgeries.

These concerns contribute to hesitancy among patients and surgeons in using allografts or xenografts and limit their acceptance in favor of autografts or synthetic substitutes. This restraint is particularly prominent in regions with stringent regulatory guidelines or limited access to advanced processing facilities.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material Type |

Allograft (e.g., demineralized bone matrix) Synthetic (ceramics, polymers, bone morphogenetic proteins) Xenograft Autograft |

| By Application |

Spinal Fusion Dental Joint Reconstruction Craniomaxillofacial Foot & Ankle Long Bone/Trauma |

| By End User |

Hospitals Specialty Clinics (orthopedic, dental, spine) Others |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Bone Grafts and Substitutes Market is segmented by Material Type, Application and End User. The increasing demand for minimally invasive orthopedic procedures, advancements in biomaterials, and the growing burden of bone-related disorders all contribute to accelerating innovation and clinical adoption in the bone grafts and substitutes market.

Each factor supports the development of safer, more biocompatible, and regenerative solutions, thereby improving surgical outcomes and enhancing patient recovery in both trauma and elective procedures.

Allografts, particularly those processed into demineralized bone matrix (DBM), hold a significant share due to their ready availability, standardized processing, and avoidance of donor site morbidity. DBMs are widely used in orthopedic and spinal procedures, offering osteoconductive and osteoinductive properties.

The synthetic segment, comprising ceramics (e.g., hydroxyapatite, tricalcium phosphate), polymers, and bone morphogenetic proteins (BMPs), is experiencing rapid growth. These materials offer controlled resorption rates, lower risk of disease transmission, and are ideal for patients where autografts or allografts are not viable.

Synthetic substitutes are favored in both high-volume and minimally invasive procedures. Xenografts, derived from animal sources (typically bovine), are used in cases where human grafts are limited, particularly in dental and orthopedic applications, though concerns around immune rejection and disease transmission slightly limit their use.

Autografts, considered the gold standard due to their osteogenic properties, remain in use, particularly in complex or high-risk surgeries, although their usage is declining due to issues like donor site morbidity and limited availability.

The market is segmented into Spinal Fusion, Dental, Joint Reconstruction, Craniomaxillofacial, Foot & Ankle, and Long Bone/Trauma. Spinal fusion remains the largest application segment, driven by the high global prevalence of degenerative disc diseases, spinal deformities, and vertebral fractures.

Bone grafts are essential in achieving vertebral stability and promoting bone fusion. The dental application segment is growing steadily with increasing demand for dental implants, especially in cosmetic and restorative dentistry. Grafts are commonly used to augment bone mass in the jaw before implant procedures.

Joint reconstruction, particularly hip and knee replacements, benefits from grafts that help repair bone defects and enhance implant fixation. Craniomaxillofacial surgeries, including reconstructive and trauma-related procedures, require high-precision bone substitutes that are often patient-specific, with growing demand for synthetic and biocompatible grafts.

The foot and ankle segment benefits from the rising number of sports-related injuries and deformity corrections. Similarly, long bone and trauma applications are driven by road accidents and complex fractures, requiring strong, bioactive graft materials for effective healing and structural restoration.

The market is divided into Hospitals, Specialty Clinics (orthopedic, dental, spine), and Others. Hospitals dominate the market due to the high volume of complex surgical procedures performed, including trauma cases and spinal reconstructions.

Their access to surgical infrastructure and specialized personnel makes them primary consumers of bone graft products. Specialty clinics, including orthopedic, dental, and spine-focused centers, are gaining market share with the increasing preference for specialized and outpatient care.

These clinics often adopt innovative and minimally invasive grafting solutions. The others category, which includes ambulatory surgical centers (ASCs) and research institutions, is growing as same-day surgery and regenerative medicine applications expand globally.

Holds the largest share of the bone grafts and substitutes market, owing to a high volume of orthopedic and spinal surgeries, early adoption of advanced biomaterials, and strong regulatory support for bone regeneration technologies. The U.S. is the primary contributor due to the presence of top-tier healthcare facilities and favorable reimbursement systems.

Also a key market, with countries like Germany, France, and the UK leading in dental and orthopedic procedures. The region benefits from strong research infrastructure, regulatory approvals for innovative biomaterials, and an aging population requiring joint replacements and trauma repairs.

Witnessing significant growth fueled by rising incidences of trauma injuries, road accidents, and degenerative diseases. Increasing healthcare investments, rising awareness of bone regenerative therapies, and growing medical tourism in India, China, and Southeast Asia are contributing to this expansion.

Shows moderate growth with rising orthopedic care demand, especially in Brazil and Mexico, though public healthcare constraints and limited access to advanced graft technologies hinder broader adoption.

The market is at a nascent stage but is gradually developing due to expanding orthopedic services, better surgical infrastructure, and increasing prevalence of bone-related conditions linked to aging and lifestyle changes.

The market was valued at USD 3.55 billion in 2024.

The market is projected to grow at a CAGR of 6.50% from 2025 to 2033.

Allograft hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Medtronic plc, Stryker Corporation and Zimmer Biomet Holdings, Inc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Bone Grafts and Substitutes Market, By Material Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Bone Grafts and Substitutes Market, By Application

5.3 Bone Grafts and Substitutes Market, By End User

6.1 North America Bone Grafts and Substitutes Market , By Country

6.1.1 Bone Grafts and Substitutes Market, By Material Type

6.1.2 Bone Grafts and Substitutes Market, By Application

6.1.3 Bone Grafts and Substitutes Market, By End User

6.2 U.S.

6.2.1 Bone Grafts and Substitutes Market, By Material Type

6.2.2 Bone Grafts and Substitutes Market, By Application

6.2.3 Bone Grafts and Substitutes Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America