Medical Affairs Outsourcing Market

Medical Affairs Outsourcing Market Share & Trends Analysis Report, By Service Type (Medical Writing & Publishing, Medical Monitoring, Medical Science Liaisons (MSLs), Medical Information, Other Services), By Industry (Pharmaceutical, Biopharmaceutical, Medical Devices (Therapeutic & Diagnostic)), By Indication / Focus Area (Oncology, Neurology, Cardiology, Immunology, Rare Diseases, Others), By Product Lifecycle Stage (Pre‑clinical, Clinical, Post‑Market Authorization)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

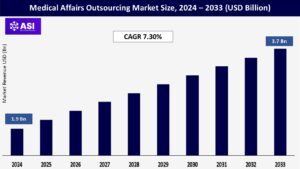

CAGR: 7.30%

Last Updated : November 22, 2025

The global medical affairs outsourcing market size was valued at approximately USD 1.9 billion in 2024 and is projected to reach USD 3.7 billion by 2033, growing at a CAGR of 7.30% during the forecast period (2025–2033).

The Medical Affairs Outsourcing Market involves the delegation of essential medical and scientific functions by pharmaceutical, biotechnology, and medical device companies to specialized third-party service providers. These outsourced functions typically include medical writing, medical information management, medical science liaison (MSL) services, regulatory support, and post-marketing surveillance.

The core purpose of medical affairs is to bridge the gap between clinical development and commercial activities while ensuring scientific integrity and regulatory compliance. Outsourcing these functions enables organizations to reduce operational costs, increase flexibility, and access expert knowledge without building large in-house teams.

It is particularly valuable during product launches, global expansions, or periods of rapid growth when internal resources may be stretched. The key properties that define this market include high scientific accuracy, strong regulatory knowledge, confidentiality, and therapeutic expertise.

Service providers must operate under stringent quality standards, such as Good Clinical Practice (GCP), and remain up-to-date with evolving regulations from authorities like the FDA and EMA. As the life sciences sector faces increasing R&D costs and regulatory complexity, medical affairs outsourcing has become a strategic choice for achieving operational efficiency and maintaining scientific excellence.

One of the most significant drivers for the medical affairs outsourcing market is the growing complexity of global regulatory frameworks. With health authorities like the U.S. FDA, EMA, PMDA (Japan), and others tightening regulations around clinical trials, promotional activities, and post-marketing surveillance, companies face mounting pressure to ensure compliance across multiple geographies.

Medical affairs teams must now generate and manage real-world evidence (RWE), health economics and outcomes research (HEOR), and regulatory documents that meet both local and international standards.

This complexity necessitates the support of specialized external partners with deep regulatory knowledge, accelerating the demand for outsourcing to ensure compliance, avoid penalties, and expedite product approvals.

Pharmaceutical and biotechnology companies are under increasing pressure to reduce operational costs while maintaining scientific excellence and regulatory compliance. Outsourcing medical affairs functions allows companies to access specialized expertise without the long-term investment required for building in-house teams.

It also enables better scalability during product launches, pipeline expansions, or sudden increases in workload. By outsourcing, organizations can reallocate internal resources toward core functions such as R&D and strategic commercialization while leveraging external partners for medical writing, KOL engagement, and medical information management. This strategic outsourcing improves efficiency, enhances flexibility, and supports faster time-to-market.

A major restraint in the Medical Affairs Outsourcing Market is the heightened concern around data security, confidentiality, and compliance with data protection regulations. Medical affairs functions often involve handling sensitive clinical data, unpublished research findings, patient information, and proprietary product knowledge.

When these services are outsourced, especially to providers in different geographical locations, there is a significant risk of data breaches, intellectual property (IP) theft, and non-compliance with region-specific privacy regulations like the EU’s General Data Protection Regulation (GDPR), HIPAA (USA), and others.

Pharmaceutical and biotech companies are often hesitant to share critical information with third-party vendors unless robust safeguards are in place, such as secure IT infrastructures, data encryption, and legal protection through non-disclosure agreements (NDAs).

Even with these measures, reputational damage or regulatory penalties from data mishandling can be severe. This concern acts as a deterrent for some firms, especially smaller companies without in-house legal and compliance expertise, thereby limiting the full potential of the outsourcing market.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Service Type |

Medical Writing & Publishing Medical Monitoring Medical Science Liaisons (MSLs) Medical Information Other Services |

| By Industry |

Pharmaceutical Biopharmaceutical Medical Devices (Therapeutic & Diagnostic) |

| By Indication / Focus Area |

Oncology Neurology Cardiology Immunology Rare Diseases Others |

| By Product Lifecycle Stage |

Pre‑clinical Clinical Post‑Market Authorization |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Medical Affairs Outsourcing Market is segmented by Service type, Industry, Indication / Focus Area and Product Lifecycle Stage. Each factor driving the medical affairs outsourcing market plays a crucial role in improving operational efficiency, enhancing scientific credibility, and accelerating time-to-market for new therapies.

The growing complexity of medical regulations, combined with the need for real-world evidence and expert communication with healthcare professionals, is increasing the demand for specialized external support.

The medical affairs outsourcing market is segmented into Medical Writing & Publishing, Medical Monitoring, Medical Science Liaisons (MSLs), Medical Information, and Other Services. Among these, Medical Writing & Publishing holds a significant share due to increasing regulatory requirements for clear, compliant documentation during clinical trials and drug approvals.

This includes the preparation of clinical study reports, investigator brochures, and scientific publications. Medical Monitoring is gaining traction as it supports clinical trial oversight and safety assessments, particularly in complex, global trials.

The demand for Medical Science Liaisons (MSLs) is also growing, as companies seek to build credible scientific engagement with healthcare providers and Key Opinion Leaders (KOLs). Medical Information services—covering drug inquiries, adverse event reporting, and literature surveillance—are increasingly outsourced to ensure 24/7 compliance and accurate dissemination of product knowledge.

Based on industry, the market is segmented into Pharmaceutical, Biopharmaceutical, and Medical Devices (Therapeutic & Diagnostic). The pharmaceutical sector dominates due to its extensive drug development pipelines and global commercialization efforts, which require robust medical affairs infrastructure.

Biopharmaceutical companies, particularly those focused on biologics and biosimilars, are rapidly increasing their outsourcing needs due to the complex nature of their products and the demand for scientific support during and after approval.

The medical devices sector, including both therapeutic and diagnostic segments, is also increasingly adopting outsourced medical affairs services. These firms rely on external partners to navigate regulatory complexity, provide clinical evidence, and support market access efforts, especially for high-risk or innovative devices.

By therapeutic area, the market includes Oncology, Neurology, Cardiology, Immunology, Rare Diseases, and Others. Oncology remains the largest segment due to the high number of clinical trials, complex treatment protocols, and the urgent need for precise scientific communication in cancer care.

Neurology and Cardiology are also growing focus areas, driven by the global rise in neurological disorders and cardiovascular diseases, both of which require long-term treatments and robust safety monitoring.

Immunology is expanding due to the increase in autoimmune disorders and advancements in immunotherapy. The rare diseases segment, though smaller in patient population, demands high medical engagement and education, pushing companies to outsource specialized medical affairs support.

The market is further segmented by product development phase into Pre-clinical, Clinical, and Post-Market Authorization stages. The clinical stage holds the largest share, as most medical affairs activities—including medical writing, scientific communication, and clinical trial support—are concentrated here to ensure regulatory compliance and trial efficiency.

In the pre-clinical phase, outsourcing is limited but growing, particularly in scientific literature review and publication planning. The post-market authorization stage is becoming increasingly important due to the growing emphasis on pharmacovigilance, real-world evidence generation, medical education, and lifecycle management of approved products.

Companies are relying on outsourced partners to handle medical inquiries, adverse event reporting, and KOL engagement even after a product is commercialized.

North America, particularly the United States, dominates the medical affairs outsourcing market due to the presence of leading pharmaceutical and biotechnology companies, a well-established clinical research infrastructure, and stringent regulatory frameworks enforced by the FDA.

The high cost of in-house operations and growing demand for real-world evidence and medical writing services are pushing companies toward outsourcing. Additionally, the region has a large pool of highly skilled professionals and global CROs (Contract Research Organizations) offering specialized services.

Europe is a mature and significant market for medical affairs outsourcing, driven by strict regulatory standards (e.g., EMA requirements) and a strong life sciences sector, particularly in countries like Germany, the UK, France, and Switzerland.

The region is seeing increased outsourcing of functions such as pharmacovigilance, medical monitoring, and KOL engagement to meet evolving compliance demands. The rise in biosimilars, cross-border clinical trials, and multilingual medical content requirements also supports the growth of outsourcing in this region.

Asia Pacific is the fastest-growing market, propelled by a booming pharmaceutical industry, lower operational costs, and a rapidly expanding clinical trials ecosystem, especially in countries like India, China, South Korea, and Singapore.

Global pharma firms are increasingly outsourcing medical affairs functions to Asia Pacific due to cost efficiency and growing expertise in regulatory documentation and post-marketing surveillance. Local CROs are also maturing and aligning with international quality standards, further attracting outsourcing opportunities.

Latin America is an emerging market for medical affairs outsourcing, with Brazil and Mexico leading in clinical research activity. The region benefits from a diverse patient population, increasing government support for clinical trials, and the growing presence of multinational pharmaceutical firms. However, regulatory variability and limited infrastructure in some countries can slow down market adoption compared to more developed regions.

The Middle East & Africa region is at a nascent stage in medical affairs outsourcing, but is showing potential due to healthcare infrastructure development and increased pharmaceutical investment.

Countries like the UAE, Saudi Arabia, and South Africa are investing in biotechnology and research sectors, which may open opportunities for medical affairs outsourcing in the future. However, market penetration remains limited due to a lack of standardized regulatory frameworks and skilled personnel.

The medical affairs outsourcing market was valued at USD 1.9 billion in 2024.

The market is projected to grow at a CAGR of 7.30% from 2025 to 2033.

The Pharmaceutical hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include IQVIA, Syneos Health and ICON plc

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Medical Affairs Outsourcing Market, By Service Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Medical Affairs Outsourcing Market, By Industry

5.3 Medical Affairs Outsourcing Market, By Indication / Focus Area

5.4 Medical Affairs Outsourcing Market, By Product Lifecycle Stage

6.1 North America Medical Affairs Outsourcing Market, By Country

6.1.1 Medical Affairs Outsourcing Market, By Service Type

6.1.2 Medical Affairs Outsourcing Market, By Industry

6.1.3 Medical Affairs Outsourcing Market, By Indication / Focus Area

6.1.4 Medical Affairs Outsourcing Market, By Product Lifecycle Stage

6.2 U.S.

6.2.1 Medical Affairs Outsourcing Market, By Service Type

6.2.2 Medical Affairs Outsourcing Market, By Industry

6.2.3 Medical Affairs Outsourcing Market, By Indication / Focus Area

6.2.4 Medical Affairs Outsourcing Market, By Product Lifecycle Stage

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping