Pharmaceutical Filtration Market

Pharmaceutical Filtration Market Share & Trends Analysis Report, By Product (Membrane Filters, Prefilters & Depth Media, Single‑Use Systems, Cartridges & Capsules, Filter Holders, Filtration Accessories, Others), By Technique (Microfiltration, Ultrafiltration, Nanofiltration, Crossflow Filtration, Sterile Filtration), By Scale of Operation (Manufacturing, Pilot‑Scale, R&D), By Application (Final Product Processing, Raw Material Filtration, Bioburden Testing, Cell Separation, Water & Air Purification), By End User (Pharmaceutical Manufacturers, Biotech Companies, CMOs, Research Labs)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

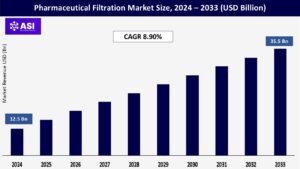

CAGR: 8.90%

Last Updated : December 15, 2025

The global Pharmaceutical Filtration Market size was valued at approximately USD 12.5 billion in 2024 and is projected to reach USD 35.5 billion by 2033, growing at a CAGR of 8.90% during the forecast period (2025–2033).

The pharmaceutical filtration market refers to the use of filtration technologies during various stages of pharmaceutical manufacturing to ensure product safety, sterility, and purity. Filtration is essential in removing particulate matter, bacteria, endotoxins, and other contaminants from drug formulations, particularly in sterile products like injectables, vaccines, and biologics.

These filtration systems are used for applications such as sterile filtration, gas filtration, clarification, viral removal, and pre-filtration. Key properties of pharmaceutical filtration systems include high efficiency in particle retention, chemical compatibility with drug ingredients, thermal and pressure resistance for sterilization processes, and biocompatibility to ensure that no toxic substances leach into the final product.

Common filter materials include PTFE, PVDF, PES, and nylon, and they are available in various formats such as membrane filters, cartridge filters, and syringe filters. As pharmaceutical manufacturing standards tighten and biologics rise in prominence, the demand for high-performance, scalable filtration solutions continues to grow.

The growing prevalence of chronic diseases such as cancer, autoimmune disorders, and diabetes has driven the demand for biologic therapies and sterile injectable drugs. These products require stringent contamination control and sterile processing, significantly increasing the use of high-performance filtration systems in production.

Regulatory authorities like the FDA, EMA, and WHO impose strict quality and sterility requirements on pharmaceutical products. Compliance with Good Manufacturing Practices (GMP) mandates robust filtration systems for particulate removal, microbial control, and viral clearance, thereby boosting the adoption of advanced pharmaceutical filtration technologies.

One significant restraint in the pharmaceutical filtration market is the high cost associated with advanced filtration systems and consumables. High-performance filters made from specialized materials such as PTFE, PES, or PVDF are expensive, especially when designed for sterile and virus-removal applications.

Additionally, the filtration units used in biopharmaceutical manufacturing must comply with strict validation, regulatory, and documentation requirements, further increasing operational and capital expenditures.

For small and mid-sized pharmaceutical manufacturers, the cost burden of installing, maintaining, and validating filtration infrastructure can be prohibitive, especially when scaling up production. This limits adoption in cost-sensitive regions and slows down innovation among smaller firms.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Product |

Membrane Filters Prefilters & Depth Media Single‑Use Systems Cartridges & Capsules Filter Holders Filtration Accessories Others |

| By Technique |

Microfiltration Ultrafiltration Nanofiltration Crossflow Filtration Sterile Filtration |

| By Scale of Operation |

Manufacturing Pilot‑Scale R&D |

| By Application |

Final Product Processing Raw Material Filtration Bioburden Testing Cell Separation Water & Air Purification |

| By End User |

Pharmaceutical Manufacturers Biotech Companies CMOs Research Labs |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Pharmaceutical Filtration Market is segmented by Product, Technique, Scale of Operation, Application and End User. Each factor plays a crucial role in ensuring drug purity, enhancing sterility assurance, and supporting the large-scale production of safe and effective pharmaceutical products particularly biologics, injectables, and vaccines.

The growing adoption of pharmaceutical filtration systems helps minimize contamination risks, improve regulatory compliance, and accelerate time-to-market for innovative therapies, ultimately contributing to greater patient safety and treatment reliability.

The market includes membrane filters, prefilters and depth media, single-use systems, cartridges and capsules, filter holders, filtration accessories, and others. Among these, membrane filters hold the largest share due to their high efficiency in removing bacteria and particulates in sterile applications.

Single-use systems are gaining rapid traction for their ability to reduce cross-contamination risks and increase operational efficiency in biopharma production.

The market is categorized into microfiltration, ultrafiltration, nanofiltration, crossflow filtration, and sterile filtration. Microfiltration and sterile filtration dominate due to their extensive use in final product sterilization and microbial removal.

Ultrafiltration and nanofiltration are increasingly used in biologics and protein purification, where molecule separation at specific pore sizes is crucial.

The market is divided into manufacturing, pilot-scale, and research & development (R&D). The manufacturing segment leads the market, driven by the demand for scalable, validated filtration systems in large-scale pharmaceutical production.

However, R&D and pilot-scale operations are essential for innovation, especially in early-stage biologic and biosimilar development.

The market spans final product processing, raw material filtration, bioburden testing, cell separation, and water and air purification. Final product processing accounts for the largest share, given the critical importance of sterility and clarity in injectable and parenteral drug products. Meanwhile, cell separation and bioburden testing are increasingly important in biologics and gene therapy workflows.

The market is segmented into pharmaceutical manufacturers, biotechnology companies, contract manufacturing organizations (CMOs), and research laboratories.

Pharmaceutical manufacturers constitute the largest end-user group due to their volume-intensive requirements and regulatory obligations. However, biotech firms and CMOs are rapidly increasing their market share, driven by the rise in outsourcing and the growing pipeline of complex biologic products.

North America dominates the pharmaceutical filtration market, driven by its well-established pharmaceutical and biopharmaceutical industries, particularly in the United States. The region benefits from strong regulatory oversight by agencies such as the FDA, which mandates stringent quality and sterility requirements for drug manufacturing.

The high volume of biologic and biosimilar production, coupled with continuous R&D in vaccine development, contributes to the high demand for advanced filtration systems.

Additionally, the presence of major filtration solution providers and the growing adoption of single-use filtration technologies in biologics manufacturing are key growth factors. Canada also contributes with its expanding clinical trial activities and investments in domestic biomanufacturing.

Europe holds the second-largest share in the global pharmaceutical filtration market. Countries like Germany, Switzerland, France, and the UK lead in pharmaceutical production and innovation, supported by strict EMA regulations and GMP guidelines.

The region emphasizes sustainability and high-quality sterile drug manufacturing, which drives the demand for energy-efficient and robust filtration systems. Europe is also a major hub for biosimilars and vaccine production, with strong public-private partnerships and government funding for advanced manufacturing technologies.

Additionally, increasing pharmaceutical exports from Europe further encourage investment in large-scale, validated filtration systems to meet international quality standards.

The Asia-Pacific region is the fastest-growing pharmaceutical filtration market, fueled by the rapid expansion of pharmaceutical manufacturing in countries such as China, India, Japan, and South Korea. These countries are investing heavily in biopharma infrastructure, driven by rising healthcare needs, supportive government policies, and growing demand for generics and biosimilars.

India and China, in particular, are becoming global outsourcing hubs for pharmaceutical production, requiring scalable and cost-effective filtration solutions to meet international regulatory standards.

Japan and South Korea are also advancing in innovative drug development, further boosting demand for high-performance filtration systems. The region’s growth is supported by the increasing adoption of single-use systems and modular cleanroom technologies.

Latin America is an emerging market with moderate growth in pharmaceutical filtration, led by countries like Brazil, Mexico, and Argentina. The region is expanding its pharmaceutical manufacturing capabilities to meet local healthcare demands and reduce dependency on imports.

However, limited regulatory enforcement and infrastructure challenges may hinder rapid adoption of advanced filtration technologies.

Nonetheless, increasing government support, foreign investments, and improvements in healthcare access are encouraging domestic production of vaccines and sterile injectables, gradually boosting the need for high-quality filtration systems. Multinational companies are also entering partnerships with local players to introduce reliable filtration solutions.

The Middle East & Africa region represents a nascent but promising market for pharmaceutical filtration. Countries such as Saudi Arabia, UAE, Egypt, and South Africa are taking initiatives to develop local pharmaceutical and biopharmaceutical industries, primarily for vaccine production and essential medicines.

Government-led health transformation programs and partnerships with international pharma companies are supporting infrastructure development. However, the region still faces challenges such as limited technical expertise, regulatory gaps, and lower healthcare spending in several parts of sub-Saharan Africa.

As the need for sterile and high-quality drug products increases, especially in response to infectious disease outbreaks, the demand for pharmaceutical filtration solutions is expected to rise steadily.

The market was valued at USD 12.5 billion in 2024.

The market is projected to grow at a CAGR of 8.90% from 2025 to 2033.

Membrane Filters hold the largest market share.

The North America region is expected to witness the highest growth rate.

Major players include Merck KGaA, Sartorius AG and Pall Corporation.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Pharmaceutical Filtration Market, By Product

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Pharmaceutical Filtration Market, By Technique

5.3 Pharmaceutical Filtration Market, By Scale of Operation

5.4 Pharmaceutical Filtration Market, By Application

5.5 Pharmaceutical Filtration Market, By End User

6.1 North America Pharmaceutical Filtration Market , By Country

6.1.1 Pharmaceutical Filtration Market, By Product

6.1.2 Pharmaceutical Filtration Market, By Technique

6.1.3 Pharmaceutical Filtration Market, By Scale of Operation

6.1.4 Pharmaceutical Filtration Market, By Application

6.1.5 Pharmaceutical Filtration Market, By End User

6.2 U.S.

6.2.1 Pharmaceutical Filtration Market, By Product

6.2.2 Pharmaceutical Filtration Market, By Technique

6.2.3 Pharmaceutical Filtration Market, By Scale of Operation

6.2.4 Pharmaceutical Filtration Market, By Application

6.2.5 Pharmaceutical Filtration Market, By End User

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping