Wireless Electric Vehicle Charging Market

Wireless Electric Vehicle Charging Market Size, Share & Trends Analysis Report, By Power Source (3–<11 kW, 11–50 kW), By Installation (Home, Commercial), By Vehicle Type (Battery Electric Vehicles (BEV), Commercial EV), By Charging Method (Capacitive Wireless Power Transfer (CWPT), Inductive Power Transfer (IPT)), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

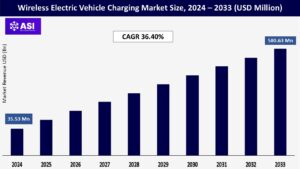

CAGR: 36.40%

Last Updated : June 4, 2026

The global Wireless Electric Vehicle Charging Market size was valued at USD 35.53 million in 2024 and is expected to grow from USD 48.46 billion in 2025 to reach USD 580.63 million by 2033, growing at a CAGR of 36.40% during the forecast period (2025-2033).

The wireless electric vehicle charging industry is based on transmitting energy without wires or cables from a power source to a consumer device. It is a dependable, practical, and secure technology to run and recharge electric cars.

Doing away with physical connectors and cords also offers advantages over conventional charging systems that are effective, affordable, and safe. The demand for charging stations is anticipated to rise dramatically in the near future as electric vehicle usage increases.

Moreover, there is an increased demand for wireless connected devices and low maintenance vehicles among the consumers. This in turn increases awareness about electric vehicles. Rise in awareness and surge in demand for electric cars leads to an increase in the production of electric vehicles.

For instance, according to a report by the IEA organization, electric car sales valued for 14 million in 2024, 95% of which were in China, Europe, and the U.S. Therefore, rise in production of electric vehicles supports the growth of the wireless electric vehicle charging market during the forecast period.

Slower charging rates and costlier integration of technology as compared to traditional cable chargers act as the key restraints to the growth of the wireless electric vehicle charging market. For instance, Robert Bosch GmbH wireless charging for electric vehicle technology costs $3000-$4000, which gives 3.6 KW power.

In addition, wireless charging devices have a distance limitation. RF energy technology fails when energy is to be transferred over a long distance. In electric vehicles, the charging time required is more and it varies in accordance with the vehicle battery capacity. Devices take longer to charge when the power supplied is of the same amount.

Furthermore, technology is more expensive, as inductive charging requires electronics and coils in both devices and chargers, thus, it increases the complexity and cost of manufacturing. However, newer approaches and advancements in technology are anticipated to reduce transfer losses and improve speed.

The main barriers preventing the market for wireless electric car charging from expanding are the slower charging rate and the more expensive integration of technology compared to conventional cable chargers.

Wireless charging equipment also has a range restriction. When energy must be delivered over a great distance, RF energy technology fails. The time needed to charge an electric car fully varies depending on the battery size. Even with the same power supply, devices take longer to charge.

Additionally, the method is more expensive because inductive charging necessitates drive electronics and coils in both the device and the charger, increasing manufacturing complexity and expense. However, it is hoped that new methods and technological developments would lessen transfer losses and boost speed.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Power Source Type |

3–<11 kW 11–50 kW >50 kW |

| By Installation Type |

Home Commercial |

| By Vehicle Type |

Battery Electric Vehicles (BEV) Commercial EV |

| By Charging Method |

Capacitive Wireless Power Transfer (CWPT) Inductive Power Transfer (IPT) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

For small and mid-sized battery-powered electric vehicles, wireless charging systems with a capacity of 3–11 kW are employed. The wireless charging system can be designed compact and light enough to fit anywhere at this power level. As a result, it is excellent for charging at both home and work.

Plugless Power Inc. has released a 3.3 kW wireless charger for the Nissan Leaf and Chevrolet Volt. WiTricity and Prodrive Technologies introduced a wireless charging system in 2023 that can charge a vehicle up to 11 kW more efficiently than cable charging solutions.

The 11–50 kW segment was the highest contributor to the market and is estimated to grow at a CAGR of 36.4% during the forecast period. 11–50 kW chargers have enhanced efficiency and require much less charging time than the 3≤11 kW.

These power source chargers have the maximum potential, as they are used in homes and commercial/public outlets. These chargers are costlier as compared to 3–<11 kW power source wireless chargers.

11–50 kW chargers provide a faster-charging option, as they can be easily installed for on-the-go charging, home charging solutions, and commercial applications Key players offering The aftermarket segment wireless solutions can target the 11–50 kW power source chargers, as they show maximum potential in different verticals.

The >50 kW range, designed for rapid charging in commercial and industrial settings, also holds a smaller portion of the market. While it supports fast charging for vehicles requiring quick turnaround times, such as buses and fleet vehicles, the higher costs associated with this technology and the more intensive infrastructure demands limit its widespread adoption in the current market landscape.

The IPT segment was the highest contributor to the market and is estimated to grow at a CAGR of 37.3% during the forecast period. In the inductive power transfer method, the system uses the coupling between the two circuits as the basis of its operation. The IPS system can be considered a two-part transformer.

The primary transformer is integrated within the power sourcing element, and the secondary transformer is in the vehicle to charge the onboard batteries. Generally, the primary and the secondary coupled circuits are in the form of coils to increase the magnetic field of the circuits.

Magnetic Power Transfer and Capacitive Power Transfer accounted for smaller segments of the market. Magnetic Power Transfer, similar in principle to inductive systems but typically designed for higher power applications, has not yet seen widespread commercial adoption due to its nascent stage of development and higher costs.

Capacitive Power Transfer, employing electric fields for wireless power transmission and known for its potential in high-frequency applications, also remains less common due to technical challenges and limited infrastructure.

The home segment accounted for the largest share in 2024, primarily driven by the widespread adoption of satellite-based services for direct-to-home (DTH) television, high-speed internet, and home automation systems. Increasing consumer demand for uninterrupted entertainment and connectivity, especially in remote and rural areas, has significantly contributed to the growth of this segment.

Advancements in satellite technology, such as high-throughput satellites (HTS) and low Earth orbit (LEO) constellations, have improved service quality and accessibility for home users. Additionally, the growing popularity of smart home devices and streaming platforms has further boosted the demand for reliable satellite services in residential settings.

The commercial segment was the highest contributor to the market and is estimated to grow at a CAGR of 36.2% during the forecast period. With the trend of autonomous electric vehicles rising, the possibility of using these vehicles for ride-sharing is expected to increase considerably.

Thus, wireless charging stations are expected to be in high demand to meet the rising trend. Moreover, commercial outlets have huge potential due to the surge in need for charging public transits. The growth of the wireless electric vehicle charging market is driven by increased commercial EV sales and demand for safer, convenient, and faster wireless charging systems.

An increase in R&D activities by leading automotive giants such as BMW, Nissan, and Chevrolet is further expected to boost the market’s growth.

Passenger Car segment held a dominant market position in the “By Vehicle Type” segment of the Wireless Electric Vehicle Charging Market, capturing more than a 70% share. This significant market dominance is primarily attributed to the escalating demand for electric passenger cars among consumers seeking sustainable and innovative transportation solutions.

The convenience offered by wireless charging systems, which eliminate the need for manual cable connections, has particularly enhanced the appeal of electric passenger cars, making them a preferred choice for daily commutes and personal use.

The commercial EV segment was the highest contributor to the market and is estimated to grow at a CAGR of 34.7% during the forecast period. Commercial electric vehicles include buses and trucks, which are now transformed into electric vehicles. Manufacturers like Tesla have introduced the Tesla Semi, an electric truck.

Several countries, such as China, are heavily investing in electric buses for their public transits, which is expected to drive the demand for wireless electric vehicle charging systems, thereby boosting the market growth.

Asia-Pacific is the second largest region. It is estimated to reach an expected value of USD 55 million by 2033, registering a CAGR of 38%. Asia-Pacific possesses high growth potential, owing to the rapid upsurge in the number of electric vehicles in countries such as China and Japan.

Several government initiatives to develop electric vehicle charging infrastructure are expected to boost the growth of the EV chargers market in this region. For instance, the Automotive Research Association of India (ARAI) planned to deploy more than 200 EV charging stations across India. All these factors together are anticipated to drive the market’s growth significantly.

Europe was the highest revenue contributor, accounting, and is estimated to grow at a CAGR of 35.9%. The European market is analyzed across the UK, Germany, France, Italy, and the rest of Europe. Europe is anticipated to witness a high growth rate during the forecast period due to technological advancements in wireless charging devices across the region.

The pace of development in the European electronics market is high due to the rise in demand for fuel-efficient and durable charging systems for electronic products such as power tools and portable gadgets.

An increase in EV sales in Germany, the Netherlands, France, Denmark, Sweden, and countries with above-average growth is expected to supplement the market growth.

North America is the third largest region. North America includes the U.S., Canada, and Mexico. The market for wireless electric car charging in this region has expanded due to rising demand for portable and wireless gadgets and technical developments in the entire economy.

North America is projected to witness an increase in demand for wireless charging systems, primarily driven by the expansion of the electronics market and the rise in EV sales. Furthermore, the rise in environmental awareness in the North American automotive market has increased EV sales utilizing fuel-efficient and eco-friendly wireless charging devices.

The market is expected to grow CAGR of 36.4% from 2025 to 2033.

The current market size is USD 48.46 Millions in 2025.

Europe currently holds the largest market shares.

The commercial EV segment was the highest contributor to the market and is estimated to grow at a CAGR of 34.7% during the forecast period.

Some of the top prominent players in the market are, Continental AG, Robert Bosch GmbH, Qualcomm Inc., Toyota Motor Corporation, Powermat Technologies Ltd, Texas Instruments Inc., Witricity Corporation., Toshiba Corporation., Elix Wireless, Evatran Group Inc., EVATRAN GROUP (plug less power), etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Wireless Electric Vehicle Charging Market, By Power Source Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Wireless Electric Vehicle Charging Market, By Installation Type

5.3 Wireless Electric Vehicle Charging Market, By Vehicle Type

5.4 Wireless Electric Vehicle Charging Market, By Charging Method

6.1 North America Wireless Electric Vehicle Charging Market, By Country

6.1.1 Wireless Electric Vehicle Charging Market, By Power Source Type

6.1.2 Wireless Electric Vehicle Charging Market, By Installation Type

6.1.3 Wireless Electric Vehicle Charging Market, By Vehicle Type

6.1.4 Wireless Electric Vehicle Charging Market, By Charging Method

6.2 U.S.

6.2.1 Wireless Electric Vehicle Charging Market, By Power Source Type

6.2.2 Wireless Electric Vehicle Charging Market, By Vehicle Type

6.2.3 Wireless Electric Vehicle Charging Market, By Installation

6.2.4 Wireless Electric Vehicle Charging Market, By Charging Method

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping