Predictive Automobile Technology Market

Predictive Automobile Technology Market Size, Share & Trends Analysis Report By Vehicle Type (Passenger Cars and Commercial Vehicles), By End-User (Insurers, and Other End-Users), By Component (Software and Hardware), By Application (ADAS, OBD, UBI), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

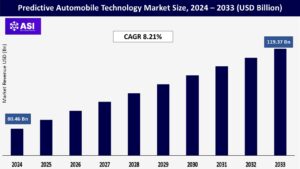

CAGR: 8.21%

Last Updated : June 5, 2026

The Predictive Automobile Technology Market size is estimated at USD 80.46 billion in 2025, and is expected to reach USD 119.37 billion by 2033, at a CAGR of 8.21% during the forecast period (2025-2033).

The automotive predictive technology market landscape is experiencing a transformative shift driven by an increasing emphasis on road safety and technological advancement.

According to the World Health Organization’s latest data, approximately 1.3 million people die annually due to road traffic crashes, with car-to-car side impacts presenting an 85% fatality risk at 65 km/h.

This sobering statistic has catalyzed the development of more sophisticated predictive safety systems, as demonstrated by recent technological breakthroughs like BMW’s early warning system that can predict critical situations seven seconds in advance with over 85% accuracy.

Due to the rapid development of technology in the automotive sector, consumers are willing to spend more money on the newest innovations that improve driving comfort and passenger and driver safety. The prediction capacities of vehicles in the automobile sector are strongly impacted by machine learning and predictive technologies.

By notifying the owner of any problems with the vehicle, these technologies improve the performance of the vehicles and are cost-effective because they decrease vehicle downtime. To draw in more customers by enhancing its users’ safety features and driving experience, several key market players are substantially investing in research and development and releasing the newest products.

The passenger car segment is anticipated to expand at a healthy rate throughout the projected period due to the trends and advancements stated above.

The demand for advanced driver assistance systems (ADAS) is expected to rise significantly during the forecast period, fueled mainly by regulatory reforms in safety applications that help protect drivers and reduce accidents.

Additionally, growing preface and awareness of potential life-saving and other comfort-based features also supported the growth of ADAS and other advanced systems in automotive, propelling the demand for wiring harness upgrades toward more sophisticated and higher-speed connections.

Governments and automakers are creating and promoting safe driving technologies, mainly passenger cars. Additionally, the majority of those technologies are anticipated to become crucial.

Protecting a semi or fully autonomous vehicle from hackers is of prime concern to federal and state governments, manufacturers, and service providers. Such disruptions could happen, as was shown by the expert hacking of a conventional vehicle.

Hackers could exploit more than a dozen portals, including entry points that appeared harmless, such as the airbag, the lighting system, and the tire pressure monitoring system, to get into even the electronic systems of a standard vehicle.

Vehicle makers formed the Automotive Information Sharing and Analysis Center (Auto-ISAC) to address cybersecurity issues, and the organization published a set of cybersecurity guidelines in 2016.

The Auto-ISAC is designated under DOT’s autonomous vehicle policy as a central clearinghouse for businesses to communicate with others in the automotive industry about any cybersecurity incidents, threats, or violations.

Apart from hackers, many government and private entities would like to access vehicle data, such as vehicle and component manufacturers, technology and sensors suppliers, urban planners, insurance companies, law enforcement, and first responders (in case of an accident).

Currently, no laws prohibit manufacturers and software providers from reselling individual vehicles and drivers’ data to third parties. Such factors hamper the market growth.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vehicle Type |

Passenger Cars Commercial Vehicles |

| By End-user Type |

Insurers Other End-users |

| By Hardware Type |

ADAS Onboard Diagnosis Other Hardware Types |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The passenger cars segment held the largest market share in 2024. The increasing popularity and demand for new-generation automobiles with advanced safety technologies are anticipated to boost the market growth.

The new generation passenger cars consist of sensors, telematics devices, stable connectivity, advanced safety features such as ADAS, predictive maintenance analysis, and predictive smart parking. Therefore, demand for predictive automobile technology in these vehicles is expected to influence market growth.

The commercial vehicles segment is anticipated to witness the fastest growth rate over the forecast period. Predictive technology in commercial vehicles assists fleet managers in reducing the cost of operations in the logistics and transportation industry.

Additionally, the real-time data on driver behavior and vehicle parameters tracked by sensors further assist fleet managers in improving fleet efficiency.

The Fleet Owners segment represents approximately 28% of the global automotive predictive technology market in 2024, establishing itself as the largest named segment. This dominant position is driven by the increasing adoption of predictive technology solutions that enhance operational efficiency and vehicle performance monitoring.

Fleet owners are increasingly leveraging these technologies to reduce vehicle downtime through proactive maintenance alerts and real-time monitoring of essential parameters. The segment’s growth is further supported by the rising demand for solutions that analyze driving behavior and minimize road accidents through timely driver alerts.

Advanced telematics solutions and AI-enabled video systems are becoming increasingly popular among fleet operators, allowing them to optimize their operations and improve overall fleet management efficiency. The integration of automotive predictive maintenance solutions is crucial for fleet owners to maintain operational excellence.

The other end-users segment held the largest market share in 2024. The surging demand for predictive technology in private passenger cars for safe, efficient, and comfortable driving is boosting the segment growth. Various ADAS functions, such as cruise control, utilize predictive technology to amend a vehicle’s speed and other parameters accordingly. Moreover, the development of autonomous vehicles is also supporting the surging demand for predictive automobile technology across private users.

The insurers segment is anticipated to witness the fastest growth rate over the forecast period. The rising popularity of UBI auto insurance in developed and emerging economies supports segment growth. UBI is a type of automotive insurance that tracks driving behavior and mileage by leveraging in-vehicle telematics devices and sensors that are either self-installed or already integrated into the vehicle.

The software segment dominated the market in 2024 and is likely to witness the fastest growth during the forecast period. Predictive automobile technology incorporates predictive analytics software to predict and correct future behavior, faults, and activities that may hamper the vehicle performance if not updated in real time.

Therefore, increasing demand for reliable predictive analytics software for various applications, including UBI, commercial fleet management, and safe driving is anticipated to drive the segment growth.

The hardware segment is anticipated to grow substantially in the upcoming years. The factors driving the segment growth include semiconductor shortage and the rising cost of sensors and automotive electronic components such as LiDAR, telematics devices, and others.

The ADAS segment held the largest market share in 2024. The increasing number of ADAS-equipped vehicle production and sales worldwide will fuel market growth. Additionally, the growing popularity of ADAS features among the populace for safe, efficient, and comfortable drive is expected to support the segment growth. Moreover, governments worldwide are taking initiatives to mandate ADAS systems to enhance road safety, which is expected to generate lucrative opportunities for the segment growth.

The UBI segment is expected to grow at the fastest pace over the projected years. UBI offers insurance premiums based on vehicle use, and driver behavior data tracked and analyzed by predictive automobile technology provides a low premium. Therefore, consumer preference to opt for UBIs for low auto insurance premiums will likely accelerate the market growth over the forecast period.

OBD and predictive maintenance segments are also anticipated to witness significant growth as they minimize the vehicle’s maintenance cost by predicting system maintenance requirements, further reducing the chances of critical system failure.

On-Board Diagnosis systems play a vital role in monitoring and reporting various vehicle parameters including emissions, mileage, faults, vehicle and engine speed, engine temperature, fluid levels, and battery status. These systems are essential for preventive maintenance and ensuring optimal vehicle performance.

The Other Hardware Types segment encompasses various components such as semiconductors, microcontrollers, and other electronic components used in telematics, fleet management devices, and modem-based connected devices.

Both segments continue to evolve with advancements in semiconductor technology, artificial intelligence, and connectivity solutions, contributing to the overall growth of the automotive predictive technology market.

The Asia-Pacific region represents a dynamic market for the automotive predictive technology sector, with China leading the regional market, followed by Japan, India, and South Korea. The region’s rapid automotive industry growth, coupled with increasing adoption of advanced technologies, creates significant opportunities for predictive technology implementation.

Countries across the region are investing heavily in smart transportation infrastructure and autonomous vehicle development, driving the demand for predictive automotive solutions.

Europe maintains a strong position in the global automotive predictive technology sector, driven by stringent safety regulations and high adoption of advanced automotive technologies. The region’s market is led by Germany, followed by France and the United Kingdom, with each country contributing significantly to technological innovations in predictive automotive solutions.

European automakers are at the forefront of implementing predictive maintenance systems and advanced driver assistance features, supported by robust research and development infrastructure.

North American automotive predictive technology sector, holding approximately 33% share of the global market in 2024. The country’s leadership position is strengthened by the presence of major automotive manufacturers and technology companies investing heavily in autonomous driving technologies.

The US market is characterized by strong consumer demand for advanced safety features and predictive maintenance solutions, supported by a well-developed infrastructure for connected vehicles. The country’s automotive sector continues to drive innovation through partnerships between traditional automakers and technology companies, particularly in developing AI-driven predictive solutions for vehicle performance and safety.

The market is expected to grow CAGR of 8.21% from 2025 to 2033.

The current market size is USD 80.46 Millions in 2025.

Asia Pacific currently holds the largest market shares.

The rapid incorporation of vehicle connectivity and cloud technology is enabling innovations and developments in the field of vehicle diagnostics and prognostics. Device integration features in connected vehicles are considered as the main enabler for predictive vehicle technology.

Some of the top prominent players in the market are Valeo SA, Robert Bosch GmbH, Verizon, Infineon Technologies AG.,Infiniti unveiled, Software Republique, Marelli.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Predictive Automobile Technology Market, By Vehicle Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Predictive Automobile Technology Market, By End-user Type

5.3 Predictive Automobile Technology Market, By Hardware Type

6.1 North America Predictive Automobile Technology Market , By Country

6.1.1 Predictive Automobile Technology Market, By Vehicle Type

6.1.2 Predictive Automobile Technology Market, By End-user Type

6.1.3 Predictive Automobile Technology Market, By Hardware Type

6.2 U.S.

6.2.1 Predictive Automobile Technology Market, By Vehicle Type

6.2.2 Predictive Automobile Technology Market, By End-user Type

6.2.3 Predictive Automobile Technology Market, By Hardware Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping