Peer-To-Peer Electric Vehicle Charging Market

Peer-To-Peer Electric Vehicle Charging Market Size, Share & Trends Analysis Report By Application (Residential, Private Homes, Apartments, Commercial, Destination Charging Station, Fleet Charging Station, Workplace Charging Station, Others), By Level Type (Level 1, Level 2) Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

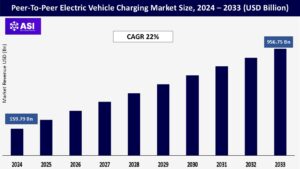

CAGR: 22%

Last Updated : June 11, 2026

The global Peer-To-Peer Electric Vehicle Charging Market Size was valued at USD 159.79 million in 2024 and is expected to grow from USD 159.79 million in 2025 to reach USD 956.75 million by 2033, growing at a CAGR of 22% during the forecast period (2025-2033).

Peer-to-peer electric vehicle charging equipment comprises several components, including couplers, cords, conductors, power outlets, and other accessories, devices, and apparatus. Manufacturers of peer-to-peer electric vehicle charging equipment obtain these components from the relevant suppliers.

Although manufacturers tend to strike supply agreements with suppliers to ensure a smooth and uninterrupted supply of components, they may also resort to spot contracts depending on the situation.

Many metropolitan cities have been facing smog and air quality issues, which have caused respiratory diseases. Such conditions are making it difficult to survive in the existing environment. In Europe, air pollution is responsible for the death of around 450,000 people every year.

In 2016, the European Commission approved new rules (National Emissions Ceilings (NEC) Directive) for its member states to reduce air pollution levels. All these factors propel the need for an eco-friendly and low-residual mode of transportation, thus, promoting the adoption of electric vehicles and increasing the need for supportive peer-to-peer electric vehicle charging stations.

According to the data published by the Global Carbon Project (GCP), China accounts for a significant share of the global CO2 emissions and is driven by an increase in coal, natural gas, and crude oil consumption, increased industrial production, and reduced hydroelectric energy generation.

There has been a significant reduction in the emission share of the US and Europe over the last seven years due to stringent regulatory policies and government initiatives. Hence, the reduction in consumption of fossil fuels and the increased adoption of electric vehicles are expected to reduce global CO2 emissions.

Advances in battery and charging technologies are expected to transform the global automotive industry. While the evolving battery technology has increased the traveling range of electric vehicles per charge, innovative chargers being introduced in the market are capable of charging batteries faster than before, thereby encouraging more consumers to opt for electric vehicles and triggering the demand for peer-to-peer electric vehicle charging units.

The growing emphasis on autonomous vehicles and shared mobility, culminating in the growing adoption of electric vehicles, also bodes well for the peer-to-peer electric vehicle charging market.

Over the past few years, interest in electric cars has grown. As a result, there has been an increase in demand for charging infrastructure. Over the projection period, it is anticipated that the fast-evolving electric vehicle charging landscape and the surge in public charging stations will challenge market growth.

Customers all over the world are concentrating on adopting battery-only electric vehicles, which is boosting the use of public charging stations. Automakers across the globe are focusing on manufacturing electric vehicles. Moreover, businesses are also focusing on adding charging stations for public use.

For instance, in August 2020, General Motors, in partnership with EVgo Services LLC, an electric vehicle charging station supplier, announced its plans to add approximately 700 fast-charging stations over the next five years. This will challenge the growth of the peer-to-peer electric vehicle charging market over the forecast period.

Moreover, fast-charging stations have greater kilowatt capacity than residential electric vehicle chargers. These fast-charging stations enable drivers to quickly recharge their vehicle batteries to travel more than 300 miles on a single charge.

The increasing number of electric vehicles is encouraging automakers to focus on deploying fast-charging stations. As a result, the rise in public charging stations is expected to hamper the peer-to-peer electric vehicle charging market growth over the forecast period.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application Type |

Residential Private Homes Apartments Commercial |

| By Level Type |

Level 1 Level 2 |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The commercial segment accounted for the largest market share and is estimated to grow at a CAGR of 22.8% during the forecast period. According to the statistics provided by the International Energy Agency, in 2017, there were 430,000 publicly accessible chargers worldwide.

Additionally, the number of private chargers at workplaces and homes was 3 million worldwide. To address the limitation of public chargers, various companies are making efforts to provide peer-to-peer EV charging solutions backed by the latest and advanced technologies, such as blockchain.

For instance, Innogy, a provider of electric charging solutions, uses blockchain technology for peer-to-peer charging. In July 2017, Innogy partnered with eMotorWerks, an electric vehicle infrastructure company.

The partnership allowed the residential and commercial owners of eMotorWerk’s electric vehicle charging stations to rent charging time to EV drivers in a peer-to-peer network powered by Innogy’s Share&Charge platform.

The residential segment led the market and accounted for more than 61.0% share of the global revenue in 2024. The segment growth can be attributed to the increase in emphasis of Original Equipment Manufacturers (OEMs) on the expansion of residential chargers specific to peer-to-peer networks.

For instance, in October 2020, Enel X announced the launch of JuiceBox, an electric vehicle charger that can be used in parking spaces at homes. JuiceBox can be remotely managed through the Enel X JuicePass app.

Private Homes dominated the residential application segment. Homeowners with installed EV chargers are increasingly opening their chargers for public use during daytime hours or while away from home.

Platforms like EVmatch have seen strong growth among homeowners willing to share their charging stations for extra income. In urban neighborhoods where public charging stations are scarce, private home-based P2P chargers offer a convenient and often cheaper alternative.

Apartments are the fastest-growing residential sub-segment. With EV adoption rising among renters, demand for accessible apartment-based chargers is soaring. Property managers and tenants are installing shared or private chargers and listing them on P2P platforms. In January 2024, a leading U.S. apartment complex operator partnered with a P2P charging network to monetize underused charging spaces, creating a new revenue stream.

Level 1 chargers are still growing, especially in certain markets. Although slower, Level 1 chargers (using standard 120V outlets) are widely available in North America and are suitable for drivers needing overnight charging or top-ups at destinations like Airbnb rentals.

As awareness grows and affordability remains critical, Level 1 P2P networks will continue expanding, especially in suburban and rural areas where long-term parking is common.

Level 2 chargers dominated the charger type segment in 2024. Level 2 chargers offer a good balance between cost, speed, and accessibility, making them ideal for P2P models where overnight or several-hour stays are common.

Private homes, apartments, and workplaces typically install Level 2 chargers, providing enough charge for daily driving needs. Hosts offering Level 2 chargers can cater to a broader audience without requiring expensive infrastructure upgrades.

The Asia Pacific is the second largest region. It is estimated to reach an expected value of USD 220 million by 2033, registering a CAGR of 23.4%. Countries are working to increase the sales of electric cars, opening up new market expansion potential.

Chinese government agencies offer incentives to increase the country’s sales of electric vehicles. For instance, the Chinese city of Guangzhou offered a USD 1,552.94 subsidy for automobiles purchased between March 2020 and the end of December 2020.

The state-level incentive for new energy cars was also extended until 2022 at the same time. Thus, it is anticipated that possibilities for market expansion will arise in the years to come as government initiatives to promote the sales of electric vehicles in the nation increase.

Europe is the fastest-growing region. The European Green Deal, aggressive decarbonization targets, and government support for EV infrastructure are propelling rapid growth. Countries like the Netherlands, Germany, France, and the UK are seeing a surge in P2P charger listings.

In February 2024, the European Union launched a pilot grant program supporting decentralized EV charging initiatives, encouraging peer-to-peer platforms to expand their operations across multiple member states.

North America dominated the peer-to-peer EV charging market in 2024. The U.S., in particular, benefits from high EV adoption rates, widespread home charger ownership, and entrepreneurial ecosystems promoting shared economy models.

California leads the charge, with robust incentives for residential chargers and strong urban demand for flexible charging solutions. Platforms like PlugShare and EVmatch have established solid user bases, reflecting the region’s maturity.

The market is expected to grow CAGR of 22 % from 2025 to 2033.

The current market size is USD 159.79 Millions in 2024.

Asia Pacific currently holds the largest market shares.

Some of the top prominent players in market are, Chargepoint Inc, ClipperCreek, Inc, EVBox, Greenlots, Enel X, Webasto Thermo & Comfort, Power Hero, Innogy, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Peer-To-Peer Electric Vehicle Charging Market, By Application Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Peer-To-Peer Electric Vehicle Charging Market, By Level Type

6.1 North America Peer-To-Peer Electric Vehicle Charging Market, By Country

6.1.1 Peer-To-Peer Electric Vehicle Charging Market, By Application Type

6.1.2 Peer-To-Peer Electric Vehicle Charging Market, By Level Type

6.2 U.S.

6.2.1 Peer-To-Peer Electric Vehicle Charging Market, By Application Type

6.2.2 Peer-To-Peer Electric Vehicle Charging Market, By Level Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping