In-vehicle Infotainment Market

In-vehicle Infotainment Market Share & Trends Analysis Report, By Component (Infotainment Unit,Head-Up Display), Application (Navigation, VPA,) By Vehicle (Paseenger Car, Light Commercial Vehicle,) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

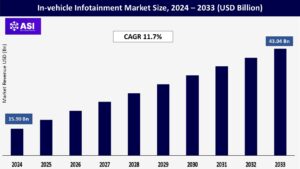

CAGR: 11.7%

Last Updated : June 15, 2026

The global In-Vehicle Infotainment Market size was worth USD 15.90 Billion in 2024. The market is forecast to reach USD 43.04 Billion by 2033, growing at a compound annual growth rate (CAGR) of 11.7% during the forecast period 2025-2033.

The report offers a comprehensive analysis of the market, highlighting the factors that will determine growth, potential challenges, and opportunities that could emerge in the In-Vehicle Infotainment industry over the next decade.

One of the notable factors behind the growth of the market is technological advancement in the smartphone and cloud technology. As the penetration of smartphones increased, many in vehicle infotainment system manufacturers started offering systems that have smartphone connectivity.

In addition, as the concept of the cloud technology emerged in vehicle infotainment software companies started using cloud technology to provide customized features and services. Thus, owing to technological evolution in the in-vehicle infotainment the demand of the in-vehicle infotainment increased globally.

As the demand of the autonomous vehicles is increasing rapidly, the in vehicle infotainment systems are evolving simultaneously. In addition, the number of screens in a passenger cars also increasing as the demand for entertainment and autonomy is increasing. Thus, many automotive industry players are focusing on integrating the artificial intelligence in their cars as an assistant to the driver.

Currently, interactive information and entertainment systems are installed in vehicles for entertainment and navigational reasons. The touchscreen infotainment, on the other hand, might distract drivers and raise the risk of an accident.

To change the music, change the channel, set up the next navigation, or turn on/off the radio, the system does not require the driver to look away from the road and at the screen. During the expected term, these issues would restrain the market for automobile infotainment systems.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application Type |

Navigation VPA |

| By Vehicle Type |

Passenger Cars Commercial Vehicles |

| By Component Type |

Infotainment Units Heads-up Display |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The passenger car segment is the highest contributor to the market and is expected to grow at a CAGR of 9.7% during the forecast period. The increased use of luxury vehicles by consumers, mostly in developing countries, is responsible for a larger share of the passenger car segment.

Luxury vehicles have more technology and safety features, and their luxurious interiors necessitate cutting-edge infotainment systems. The Commercial Vehicle segment holds over 67% of the market, reflecting the rising adoption of infotainment for fleet management, driver communication, and navigation.

The commercial vehicle segment is expected to grow at a significant rate. The segment is anticipated to grow as a result of rising demand from the logistics industry for commercial vehicles and increased attention from the auto industry on using vehicles in fleet management.

Navigation is the most used service in the in-vehicle infotainment systems market 2024. Navigation services help to provide real-time traffic information, route guidance, and point-of-interest recommendations, which help to navigate efficiently.

Further, mapping technology advancements have improved navigation systems’ accuracy and reliability, providing users with precise and up-to-date information.

Integrating navigation services with other infotainment features, such as entertainment and connectivity, enhances the overall user experience and is offered by service providers as a bundled service at an affordable price.

The virtual private assistant (VPA) has emerged as the powerhouse behind the widespread adoption of embedded systems in-vehicle infotainment. This application encompasses intelligent voice recognition, natural language processing, and contextual understanding capabilities, enabling users to perform a plethora of tasks hands-free while on the road.

From setting up navigation routes to playing music, making calls, sending messages, and even controlling various vehicle functionalities, VPAs have become an indispensable part of the modern-day driving experience.

The display/infotainment unit’s size typically ranges from 2 to 20 inches. The basic car display unit is between three and five inches. The average screen size of mid-segment vehicles is 7 inches.

A simple touch screen and occasionally audio-video interfaces are used to provide clients with access to safety features, navigation, vehicle diagnostics, and other entertainment services. Also, the size of infotainment system screens is increasing with each new model launch as it adds a premium element to the car and is now a key factor to take into account when buying a new car.

A head-up display (HUD) is a display that allows the user to see displayed data without looking away from the outside world. A display technology that superimposes images onto the inside of the windshield to enable drivers to view the information while keeping their eyes on the road.

Heads-up displays (HUDs) are also used in goggles and helmets. The scope of the report covers details on the latest trends, developments, and technologies.

Asia-Pacific In-Vehicle infotainment market accounts for the second-largest market share due to a rise in local consumers’ disposable money, a considerable demand for automobile infotainment systems.

Effectiveness and augmented reality technology-based solutions are preferred by customers which is one of the factors, which is driving the market growth. A majority of the world’s vehicles are produced in nations like China, South Korea, India, and Japan.

The Europe In-Vehicle infotainment Market is expected to grow at the fastest CAGR from 2025 to 2033. the widespread presence of top manufacturers and in-car entertainment companies.

The region is the biggest market for premium vehicles and well-known automakers. Additionally, there is a significant need for in-car infotainment systems due to the region’s enormous consumer base. The market also gains from R&D initiatives taken by significant automakers.

North America is the most significant shareholder in the global In-Vehicle Infotainment market and is expected to grow at a CAGR of 9.9% during the forecast period. The skyrocketing consumer demand for premium vehicles in the U.S. is the key determinant snowballing the regional market growth. The demand for local companies will increase as voice recognition, and driver distraction systems gain popularity.

End-user preference for high-definition in-gauss screens is another noteworthy trend in the local in-vehicle entertainment systems industry. According to reports, Emergency Safety Solutions, Inc. (E.S.S.), the company behind the Hazard Enhanced Location Protocol (H.E.L.P.), will collaborate with Tesla to implement a new vehicle hazard warning system.

The growing popularity of premium cars and growing consumer demands for intelligent in-car features are driving the automotive infotainment industry in the Middle East and Africa.

High-end cars with cutting-edge infotainment systems are highly preferred in wealthy markets like the United Arab Emirates and Saudi Arabia. Adoption of entertainment systems is also being aided by the popularity of electric and hybrid cars, especially in the Gulf Cooperation Council (GCC) nations.

The market is expected to grow CAGR of 11.7% from 2025 to 2033.

The current market size is USD 15.90 Billions in 2024.

Asia -Pacific currently holds the largest market shares.

Consumer demand for in car entertainment, smartphone integration, and 5G expansion.

Key players include Panasonic, Harman (Samsung), Bosch, Continental AG.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 In-vehicle Infotainment Market, By Application Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 In-vehicle Infotainment Market, By Vehicle Type

5.3 In-vehicle Infotainment Market, By Component Type

6.1 North America In-vehicle Infotainment Market , By Country

6.1.1 In-vehicle Infotainment Market, By Application Type

6.1.2 In-vehicle Infotainment Market, By Vehicle Type

6.1.3 In-vehicle Infotainment Market, By Component Type

6.2 U.S.

6.2.1 In-vehicle Infotainment Market, By Application Type

6.2.2 In-vehicle Infotainment Market, By Vehicle Type

6.2.3 In-vehicle Infotainment Market, By Component Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping