Electric Vehicle Charger (EVC) Market

Electric Vehicle Charger (EVC) Market Size, Share & Trends Analysis Report By Vehicle Type (Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV)), By Charging Type (Onboard Chargers, Off-board Chargers), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

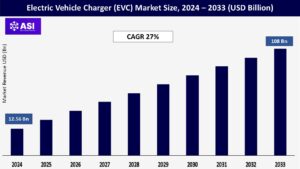

CAGR: 27%

Last Updated : December 23, 2025

The global electric vehicle charger (EVC) market size was valued at USD 12.56 billion in 2024 and is estimated to grow from USD 15.95 billion in 2025 to reach USD 108 billion by 2033, growing at a CAGR of 27% during the forecast period (2025-2033).

An electric vehicle (EV) charger charges electric vehicles with a battery and an electrical source that helps to charge the battery. Such vehicles can be charged through different levels of charging, that is, level 1, level 2, and level 3.

The cost, in addition to the maintenance cost of electric vehicles, is lower than conventional petrol/diesel cars. Implementing stringent government regulations regarding using electric vehicles to curb environmental pollution drives their demand.

This is because electric vehicles aid in reducing carbon emissions, which contain toxic gas particles, which, in turn, boost the need for EV chargers Furthermore, the surge in demand for electric vehicles fuels market growth. An increase in demand for luxury electric vehicles is expected to offer ample opportunities to key players operating in the market.

The conventional gas-powered vehicle uses an internal combustion engine to generate power. In an ideal scenario, the combustion system completely incinerates the fuel and emits carbon dioxide and water as waste; however, the combustion system generates various greenhouse gases, leading to environmental pollution.

On the contrary, an electric vehicle uses an electric motor powered via a continuous supply of current; hence, it does not lead to the emission of pollutants. U.S., Germany, France, and China have implemented stringent government regulations for vehicular emission, making it mandatory for automobile manufacturers to use advanced technologies to combat high vehicle emission levels.

In addition, a program launched by the California Air Resources Board (CARB) includes guidelines for manufacturers to produce and deliver zero-emission vehicles (ZEVs), substantially boosting the adoption of electric vehicles, which, in turn, augments the need for electric vehicle chargers.

Furthermore, several policies have been deployed by various governments across the globe to meet environmental conditions. For instance, Electric Vehicle Initiative (EVI), a multi-firm government policy forum established in 2009 under Clean Energy Ministerial (CEM), helped key players to accelerate the deployment of electric vehicles worldwide (as per IEA.org).

Because it is a fossil fuel, gasoline cannot be renewed as an energy source and will eventually run out. Creating and utilizing alternative fuel sources is crucial for promoting sustainable development. This entails using electric vehicles, which are more cost-effective than traditional automobiles and do not require gasoline.

Compared to gas-powered vehicles, which can only convert 17–21% of the energy stored in gasoline, electric vehicles can convert almost 50% of the electrical energy from the grid to power at the wheels, encouraging their use.

In addition, the recent increase in the price of gasoline and diesel has raised the demand for fuel-efficient vehicles. This is attributed to the depletion of fossil fuel reserves and an increase in the tendency of companies to gain maximum profit from these oil reserves.

Thus, these factors boost the need for advanced fuel-efficient technologies, leading to a surge in demand for electrically powered vehicles, and propelling the demand for electric vehicle chargers.

End customers’ desire for EV chargers is hampered by a lack of uniformity in the industry. Customers frequently hesitate to decide whether such EV chargers are appropriate for their automobiles.

Additionally, the vehicles require more adaptable charging systems to benefit from the fastest charging speeds when they become available. The lack of standard plugs makes charging much more challenging.

Although the network of chargers for Tesla vehicles is growing, they are made exclusively for Tesla automobiles. Tesla is an American electric vehicle and clean energy corporation headquartered in Palo Alto, California.

Additionally, the 120- and 240-volt plugs, which are typically used in houses, have been standardized by the automobile industry. However, the plugs or ports that may charge vehicles in 30 minutes or fewer have not yet been defined. Thus, all these factors together restrain the growth of the global market.

Another opportunity arises from the increasing interest in wireless and autonomous charging technologies. Wireless charging, which eliminates the need for physical cables, is a highly attractive option for the next generation of electric vehicles.

Companies such as Qualcomm and WiTricity are actively developing wireless charging technologies, which are expected to be a game-changer for the EVC market.

Additionally, autonomous vehicles, which will require sophisticated charging infrastructure, could further drive the demand for innovative charging solutions in the coming years. This evolving technology landscape is opening new avenues for growth in the EVC sector.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Vehicle Type |

Battery Electric Vehicle (BEV) Plug In Hybrid Electric Vehicle (PHEV) |

| By Charging Type |

Onboard Chargers Off-Board Chargers |

| By End-Use Type |

Residental Commercial |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

A plug-in hybrid electric vehicle (PHEV) combines a gasoline or diesel engine with an electric motor and a large rechargeable battery. These vehicles are integrated with an internal combustion engine and electric motor. They are powered by an alternative fuel or a conventional fuel, such as gasoline (petrol), and a battery, which is charged with electricity by plugging into an electrical outlet or charging station.

Two basic plug-in hybrid configurations are available in the market, which include series plug-in hybrids or extended range electric vehicles (EREVs) and parallel or blended plug-in hybrid electric vehicles. The miles per gallon on a plug-in hybrid (PHEV) are higher than on internal combustion engine (ICE) vehicles. In addition, PHEVs emit fewer gases than conventional ICE vehicles, as they have extra capacity to run a certain distance without burning a single drop of fuel, which drives the market’s growth.

The BEV segment is the second largest. A BEV does not require gasoline during operation and relies solely on pure electric battery power. Such vehicles are not equipped with an internal combustion engine or fuel tank and operate on a fully electric drivetrain powered by rechargeable batteries, which drives the market growth.

BEVs need to be plugged into a power source to charge, and depending on the vehicle, they have varying charging times and driving ranges. In addition, such vehicles have longer electric driving ranges than PHEVs, boosting market growth. Nissan Leaf and Tesla Model S are the key examples of battery electric vehicles. Furthermore, the demand for BEVs has increased significantly over the years to reduce the carbon emissions from fuel cars.

Moreover, enforcement of stringent government regulations to restrain environmental pollution and reduce the dependency on fuel cars is expected to boost the demand for battery electric vehicles, thereby augmenting the growth of the global market.

Most of the EVs in the market are equipped with an onboard charger. In addition, the manufacturer supplies a unit of the charger to customers. The EV owner can use this charger to charge the EV from the house power outlet, propelling the market growth. The surge in BEVs and PHEVs is expected to boost the demand for onboard chargers during the forecast period. Onboard chargers include AC level 1 and 2 modes of charging systems that convert AC to DC. Onboard chargers are available at most charging stations, which are more cost-effective than off-board chargers.

In 2024, Off-board Chargers held a dominant market position, capturing more than a 72.4% share in the electric vehicle charger market by charging type. These chargers are widely used in public and commercial spaces, offering higher power output and faster charging times compared to on-board systems.

Their popularity is especially strong among fleet operators, highway service stations, and urban public charging networks, where quick turnaround is essential. DC charging stations have a unique grid that can charge the vehicle in a few minutes, which reduces downtime. CHAdeMO, combo charging system (CCS), and supercharger are the recent developments in the market. The surge in demand for luxury and supercars is projected to fuel the demand for DC fast chargers, thereby driving the growth of the global market.

In 2024, Residential held a dominant market position, capturing more than a 62.8% share in the electric vehicle charger market by end user. This strong presence is primarily driven by the rising number of personal electric vehicle purchases, particularly in urban and suburban regions where users prefer the convenience of overnight home charging.

An electric vehicle commonly comes with a level 1 EVSE charger with three-pong household plugs on one end and a J1772 connector on the other, making it suitable for most home-based charging. As more homeowners install Level 1 and Level 2 chargers, often supported by local utility rebates and tax incentives, the adoption curve continues to rise. The residential segment is further supported by smart home integration features and user-friendly mobile apps, making charging management easier and more efficient.

Commercial charging is rapidly emerging as a critical application segment, driven by the electrification of corporate fleets, workplace charging initiatives, and the integration of charging infrastructure in retail, hospitality, and real estate developments. Businesses are recognizing the value of offering EV charging as a service to employees, customers, and tenants, enhancing their sustainability credentials and attracting environmentally conscious stakeholders.

The deployment of advanced charging solutions, including fast and ultra-fast DC chargers, is enabling commercial entities to cater to diverse user needs, from short-term visitors to long-term parkers. Partnerships between charging network operators, utility companies, and commercial property owners are accelerating the rollout of commercial charging infrastructure, positioning this segment for robust growth in the coming years.

The Asia Pacific region currently dominates the Electric Vehicle Charger (EVC) market, accounting for approximately USD 8.6 billion in revenue in 2024. China, as the world’s largest EV market, is the primary driver of regional growth, supported by aggressive government policies, massive investments in charging infrastructure, and a rapidly expanding consumer base.

Japan and South Korea are also making significant strides, leveraging advanced technologies and strong automotive industries to accelerate EVC deployment. The Asia Pacific market is expected to maintain its leadership position, with a projected CAGR of 25.1% from 2025 to 2033, driven by continued policy support, technological innovation, and rising EV adoption rates.

Europe is the second-largest market for Electric Vehicle Chargers, with a market size of USD 5.1 billion in 2024. The region’s growth is underpinned by ambitious decarbonization targets, stringent emissions regulations, and substantial investments in public charging networks.

Leading countries such as Germany, the United Kingdom, France, and the Netherlands are at the forefront of EVC deployment, supported by robust government incentives and a strong focus on interoperability and standardization. The European market is also benefiting from collaborations between automakers, energy companies, and technology providers, which are accelerating the rollout of fast and ultra-fast charging infrastructure across the continent.

North America, led by the United States and Canada, recorded a market size of USD 3.7 billion in 2024. The region is witnessing rapid growth, fueled by increasing EV adoption, supportive federal and state policies, and significant investments from both public and private sectors.

The expansion of fast-charging networks along major highways and urban centers is addressing range anxiety and supporting long-distance travel. The North American EVC market is projected to grow at a CAGR of 22.8% through 2033, supported by ongoing infrastructure development, technological advancements, and the entry of new market players.

Latin America and the Middle East & Africa are emerging markets for EVCs, with combined revenues of USD 1.8 billion in 2024. These regions are gradually embracing electric mobility, supported by urbanization trends, increasing environmental awareness, and pilot projects in major cities.

The market is expected to grow CAGR of 27 % from 2025 to 2033.

The current market size is USD 12.56 Billions in 2024.

Asia Pacific currently holds the largest market shares.

Top industry players are, ABB Ltd., Robert Bosch GmbH, Siemens AG, Delphi Automotive, Chroma ATE, Aerovironment Inc., Silicon Laboratories, Chargemaster PLC, Schaffner Holdings AG, POD Point., etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Electric Vehicle Charger (EVC) Market, By Vehicle Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Electric Vehicle Charger (EVC) Market, By Charging Type

5.3 Electric Vehicle Charger (EVC) Market, By End-Use Type

6.1 North America Electric Vehicle Charger (EVC) Market , By Country

6.1.1 Electric Vehicle Charger (EVC) Market, By Vehicle Type

6.1.2 Electric Vehicle Charger (EVC) Market, By Charging Type

6.1.3 Electric Vehicle Charger (EVC) Market, By End-Use Type

6.2 U.S.

6.2.1 Electric Vehicle Charger (EVC) Market, By Vehicle Type

6.2.2 Electric Vehicle Charger (EVC) Market, By Charging Type

6.2.3 Electric Vehicle Charger (EVC) Market, By End-Use Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping