Automotive Engine Management System Market

Automotive Engine Management System Market Share & Trends Analysis Report By Engine Type (Diesel, Gasoline), By Component (Engine Control Unit (ECU), Sensors), By Vehicle Category (Passenger Cars, Commercial Vehicles).

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

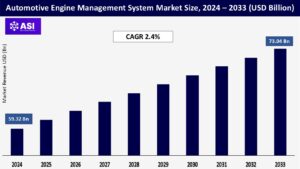

CAGR: 2.4%

Last Updated : June 17, 2026

The worldwide Automotive Engine Management System Market size is anticipated to see steady growth, with forecasts indicating the market size will reach USD 59.32 billion in 2024, increasing to USD 73.04 billion by 2033. This indicates a compound annual growth rate (CAGR) of 2.4%.

The engine management system in automobiles is essential for enhancing vehicle performance, ensuring compliance with emissions standards, and boosting fuel efficiency. With the rising need for cleaner and more efficient vehicles, engine control systems are evolving to be more intelligent and integrated.

Rising emission standards, fuel efficiency requirements, and consumer desire for enhanced driving experiences are significant drivers of the uptake of contemporary engine management systems. These systems employ sophisticated sensors, ECUs, and immediate data processing to enhance air-fuel mixture, ignition timing, and engine load parameters.

Technologies like cylinder deactivation, variable valve timing, and hybrid powertrains are heavily dependent on advanced engine management. Moreover, producers face pressure to comply with Euro 6, BS-VI, and EPA Tier 3 regulations, which promote the adoption of efficient and integrated control systems.

Although fully electric vehicles do away with conventional combustion engines, plug-in hybrids and range-extender electric vehicles still depend on intricate engine management systems.

Moreover, the need for engine management enhancement is increasing in mild hybrid and strong hybrid vehicles, which necessitate smooth integration between electric motors and internal combustion engines. This shift is transforming the EMS market environment, leading OEMs to invest in flexible and scalable control systems.

The main difficulties involve the elevated expenses associated with the development and execution of sophisticated ECUs and sensor systems. These advanced components require significant R&D expenditures, along with the miniaturization and software integration needed for contemporary engine management systems.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Engine Type |

Diesel Gasoline |

| By Component Type |

Engine Control Unit [ECU] Sensors |

| By Vehicle Type |

Passenger Cars Commercial Vehicles |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

Gasoline is held the most of the portion in global market is 65% in 2024. Gasoline Sector remains the leader owing to its extensive use in passenger cars. Gasoline engines can be controlled more easily through electronics, facilitating improved integration of EMS solutions.

Nonetheless, this segment is projected to expand gradually as the market progressively transitions to hybrid and electric powertrains.

For instance, automakers like Volkswagen and BMW have shifted their focus to gasoline-powered models to comply with emission limits, given the challenges of meeting stringent NOx standards with diesel engines.

Diesel is acquired the 35% market shares in the global market. Diesel Segment anticipated to experience a minor decrease in market share owing to stricter emission regulations and a drop in demand for passenger vehicles, particularly in Europe.

Nonetheless, diesel continues to be essential for commercial vehicles and off-road applications where engine performance and torque are key. A diesel engine is an internal combustion engine that relies on compression ignition to burn fuel, typically diesel, to power vehicles, machinery, and industrial equipment.

Unlike gasoline engines, diesel engines are known for their efficiency and durability, making them ideal for heavy-duty applications that require high-torque output, such as construction, transport, agriculture, and power generation.

The ECU segment commands the largest portion of the market 60% in 2024 and is expected to experience consistent growth. It functions as the engine’s brain, analyzing data from various sensors to manage the combustion process.

Engine Control Unit (ECU) sensors are important for keeping an eye on several engine-related characteristics, including pressure, temperature, airflow, and oxygen levels. Every sensor has a distinct purpose that enhances the engine’s efficiency and performance.

Moreover, a car usually has a single ECU that processes the information from the sensors and modifies the engine in real time to maximize performance. Even though the ECU is unique, it is essential to the coordination of the complex functions of the engine management system.

Sensors are acquired the 40% market shares of the global market. Sensors the demand for sensors is rising quickly because of heightened complexity in EMS.

Sensors like oxygen, knock, crankshaft, camshaft, and mass air flow (MAF) are essential for immediate modifications. The rise of turbocharged engines and emission management systems is enhancing sensor usage.

Passenger cars leading the market with 70% of the global market. Thanks to substantial worldwide production levels and quicker technological adoption. Focus on performance, emissions, and customer satisfaction is promoting innovation in this area.

This is primarily due to consumers’ higher demand for passenger cars worldwide. Passenger cars are often subject to more stringent emission regulations compared to commercial vehicles, necessitating the implementation of advanced engine management systems to ensure compliance.

The rise in demand for sports utility vehicles (SUVs) creates profitable opportunities for market players as the sale of sports utility vehicles accounts for more than 50% of passenger car sales in India.

Commercial vehicles are held the portion with 30% of the global market. Commercial Vehicles the need for EMS is increasing in this industry because of tighter emissions regulations and an enhanced emphasis on fuel economy. Collaboration with telematics and forecasting maintenance is becoming widespread.

Commercial vehicles, including light and heavy commercial vehicles (LCV and HCV), have unique needs in terms of engine performance, fuel efficiency, and emissions control, which impact the EMS market.

North America accounted for a strong 31.5% of the worldwide automotive EMS market in 2024. North America possesses a considerable portion of the worldwide automotive engine management system market, driven by a dense presence of automotive OEMs and robust technological implementation.

The U.S. is at the forefront of the region, propelled by regulatory requirements for fuel efficiency, emission criteria, and the swift adoption of electronic engine controls and sensor-based monitoring systems.

Moreover, the area’s prompt embrace of hybrid and electric powertrains is affecting the need for sophisticated engine management systems (EMS) in both passenger and commercial vehicles

Europe stands as the second-biggest market with 28.5% market shares, bolstered by strict EU emissions standards (such as Euro 6/7) and a robust presence of high-end and luxury vehicle manufacturers. Nations like Germany, France, and the UK fuel this advancement by investing heavily in R&D for cleaner, more efficient engines.

Management of diesel engines remains significant in commercial fleets, as gasoline and hybrid engine technologies enhance EMS integration. The implementation of mild-hybrid systems (48V) is increasing the need for ECUs and sensors.

APAC is acquired the 30% of the global EMS market. The APAC region is the quickest-growing area, driven by rising automotive manufacturing and growing vehicle ownership in China, India, and Southeast Asia.

China dominates the region because of its extensive automobile production foundation and emphasis on electric vehicles, which demand sophisticated EMS. India is undergoing swift growth, propelled by BS-VI regulations and encouragement from the Make in India program. Japan and South Korea are enhancing demand by emphasizing hybrid and plug-in hybrid technologies.

MEA is having only 5% share of the global EMS market. MEA demonstrates consistent growth, driven by rising demand for passenger vehicles and high-performance cars in Gulf Cooperation Council (GCC) nations such as the UAE and Saudi Arabia.

The growth of infrastructure and increasing consumer income are boosting automotive sales. Nonetheless, restricted domestic production and a strong dependence on imports somewhat hinder greater EMS adoption. Engine longevity and efficiency in extreme weather conditions are driving EMS enhancements.

Lati America is accounted onlyn5% shares of the EMS global markets. The growth of Latin America is steady yet moderate. Brazil and Mexico lead because of a solid OEM presence and governmental backing for domestic manufacturing.

The transition to more fuel-efficient engines and the implementation of emission standards are driving the demand for EMS. Mexico, serving as a manufacturing center for U.S. OEMs, is experiencing substantial EMS integration in vehicles that are exported. Growth is additionally bolstered by the rising interest in hybrid vehicles within city markets.

The market is expected to reach USD 73.04 billion by 2033.

Engine Control Units [ECUs] and Sensors are the major components of EMS.

Gasoline Engine is most dominate the EMS market.

Asia-Pacific is projected to grow at the highest CAGR, driven by vehicle production and emission reforms.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Engine Management System Market, By Engine Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Engine Management System Market, By Component Type

5.3 Automotive Engine Management System Market, By Vehicle Type

6.1 North America Automotive Engine Management System Market , By Country

6.1.1 Automotive Engine Management System Market, By Engine Type

6.1.2 Automotive Engine Management System Market, By Component Type

6.1.3 Automotive Engine Management System Market, By Vehicle Type

6.2 U.S.

6.2.1 Automotive Engine Management System Market, By Engine Type

6.2.2 Automotive Engine Management System Market, By Component Type

6.2.3 Automotive Engine Management System Market, By Vehicle Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping