Electric Vehicle Charging Station Market

Electric Vehicle Charging Station Market Size, Share & Industry Analysis, By Charger Type (AC Charging Station, and DC Charging Station), By Application (Passenger Cars and Commercial vehicles), By Propulsion (BEV and PHEV) Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

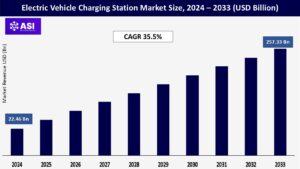

CAGR: 35.5%

Last Updated : June 17, 2026

The global Electric Vehicle Charging Station Market size was valued at USD 22.46 billion in 2024. The market is projected to grow from USD 30.63 billion in 2025 to USD 257.33 billion by 2033, exhibiting a CAGR of 35.5% during the forecast period.

Asia Pacific dominated the global market with a share of 62.64% in 2024. The Electric Vehicle (EV) Charging Stations Market in the U.S. is projected to grow significantly, reaching an estimated value of USD 2.04 billion by 2033.

An electric vehicle charging station, also referred to as an EV charging point, connects an electric vehicle to an electric source for charging. The station consists of Electric Vehicle Supply Equipment (EVSE) and the necessary infrastructure to deliver power.

The rising popularity of electric vehicles is the main driver behind market growth. The global automotive industry has experienced significant development, with electric car sales growing significantly in recent few years. This is due to increased demand for zero-emission vehicles, strict government regulations to control car emissions, incentives, and government tax credits for rapid electrification.

Therefore, the demand for EV chargers is anticipated to bolster market growth due to the rapid electrification of vehicles globally. Global electric vehicle sales in 2021 have doubled compared to 2020, according to the 2021 edition of the International Energy Agency. By 2022, electric vehicle sales exceeded 10 million units.

Factors such as rising fossil fuel prices, increasing public environmental concerns, and falling electric vehicle battery prices are also contributing to market growth. Moreover, from 2010 to 2021, the cost of battery packs dropped by almost 90% in real terms.

Various manufacturers are rapidly advancing their battery technologies in the EV sector. In line with this, they are working on technologies such as wireless charging and autonomous charging robots, which may make vehicle charging convenient. For instance, Siemens AG launched a new high-power charger, Sicharge D.

It features scalable, high charging power of up to 300 kW. The charging station also supports voltages between 150 and 1,000 volts and charging currents of up to 1,000. Moreover, the integration of higher-voltage Level 2 chargers and rapid DC fast chargers that provide quicker charge times and enhance the overall EV ownership experience is also contributing to market growth.

Apart from this, various power companies are increasingly investing in developing the public charging infrastructure to cater to the escalating need for faster and more affordable charging solutions.

For instance, in October 2022, Ather Energy announced the installation of the 580th public fast charging point, the Ather Grid, across 56 cities in India. As the company expands its national footprint, Ather Energy plans to install 820 more grids, bringing the total to 1400 by the end of FY23. Ather Grids are strategically installed across markets, with 60% of current installations in tier-II and tier-III cities.

The growth of the electric vehicle charging stations market is facing challenges due to the high upfront costs associated with the installation of fast-charging infrastructure, including equipment, grid upgrades, and site development

Limited power grid capacity, especially in rural and developing regions, and the need for extensive permitting and regulatory approvals create additional barriers to the rapid deployment of charging networks

Commercial site owners, governments, and charging service providers often face difficulties in securing suitable locations and managing the complex logistics of integrating chargers with existing urban infrastructure

As EV adoption accelerates, addressing cost barriers through public-private partnerships, streamlined permitting processes, and innovations in grid management will be crucial to scaling up the electric vehicle charging stations market globally

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Charger Type |

AC DC |

| By Vehicle Type |

Passenger Cars Commercial Vehicles |

| By Propulsion Type |

BEV PHEV |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

In 2024, AC Charging leads the world electric vehicle charging station market forecast with a strong share of 88.1%. This is due to extensive use of alternating current (AC) chargers in both residential and commercial areas. AC chargers are cheaper to install and operate compared to DC fast chargers, and hence they are the preferred solution for home installations, offices, and public charging stations.

These chargers are generally slower but sufficient for overnight charging or extended stops, providing a balance between cost and charging time. The growing use of electric vehicles, along with government incentives and encouragement of EV infrastructure, has helped fuel the ongoing expansion of AC charging stations.

As the demand for electric vehicles on the road increases, so will the need for AC charging stations, particularly in inner cities where the ability to charge conveniently and at a low cost is vital for EV owners.

DC charging station maintained 78.70% of the electric vehicle charging station market share in 2024, while it accelerated at 56.29% CAGR during the forecast period, driven by operator strategies to reduce charging session duration and increase throughput.

Oak Ridge National Laboratory achieved a breakthrough in wireless charging technology, demonstrating 100-kW power transfer to passenger vehicles with 96% efficiency across a five-inch air gap, potentially disrupting traditional connector-based charging.

AC charging below 22 kW serves primarily residential and workplace applications where longer dwell times accommodate slower charging speeds, while maintaining cost advantages for installations with lower utilization requirements.

The emergence of megawatt charging systems for commercial vehicles creates a distinct ultra-high-power category that requires specialized electrical infrastructure and cooling systems.

Passenger cars commanded 89.10% of the electric vehicle charging station market share in 2024, yet commercial vehicles exhibit the fastest growth at 55.47% CAGR through 2033, reflecting the infrastructure requirements for fleet electrification mandates.

Buses represent a critical commercial segment where electrification accelerates due to urban air quality mandates and predictable route patterns that enable optimized charging infrastructure deployment. Two-wheelers gain traction in emerging markets where battery swapping models prove economically viable, particularly in India.

Trucks require the most sophisticated charging infrastructure due to weight constraints and operational demands, driving innovation in high-power charging systems and depot-based solutions.

Commercial vehicle electrification creates anchor demand that justifies charging infrastructure investment, as fleet operators provide predictable utilization patterns and higher power requirements than passenger vehicles.

CharIN officially launched the Megawatt Charging System at EVS35 in Oslo, establishing standards for charging capacities up to 3.75 MW that enable commercial vehicles to achieve operational parity with diesel counterparts.

Passenger car infrastructure benefits from commercial vehicle deployment as shared charging corridors reduce per-unit infrastructure costs and improve network utilization rates across vehicle categories.

The BEV segment dominates the market due to customer preferences and the rising demand and growing manufacturing of BEV-based vehicles across the globe. This dominance is expected to continue in future. Ongoing advancements in battery technology have improved the performance and range of battery electric vehicles (BEV).

Lithium-ion batteries have become less expensive and efficient, addressing concerns about limited driving range. Major automotive manufacturers are heavily investing in electric vehicle technology and production leading to an increasing variety of electric models available that cater to different market segments and consumer preferences.

Additionally, stringent emission standards and government regulations in various regions are compelling automakers to prioritize electric vehicles in their product portfolios. This regulatory pressure contributes to the industry’s shift toward cleaner transportation solutions.

Plug-in hybrid vehicles (PHEV) combine an electric motor with a conventional engine, offering the advantage of extended range. This addresses range anxiety, making PHEVs more appealing to consumers concerned about charging infrastructure availability.

PHEVs can operate in electric-only mode for short distances and switch to the internal combustion engine when needed for longer distances. This dual capability provides flexibility and addresses concerns about limited electric range.

In 2024, the Asia-Pacific region has the largest market share of the EV charging station market, at 54.5%. This is mainly due to the speedy adoption of electric vehicles in the countries of China, Japan, and South Korea, which are leading the world in the EV movement.

Regional government policies are highly conducive to the adoption of EVs, with subsidies, tax breaks, and investment in charging infrastructure being primary growth drivers.

China, the world’s biggest EV market, has invested heavily in the development of its charging infrastructure, which further fuels the growth of electric vehicles.

Europe shows the fastest regional growth at 42.68% CAGR to 2033. The Spark Alliance integrates 11,000 high-power connectors across 25 countries, offering transparent pricing and 100% renewable electricity.

Germany’s plan for more than 1 million new charging points by 2030 aligns with EU regulations that tie infrastructure quotas to EV registrations. Norway retains the world’s highest per-capita charger count, while France uses low-interest loans to spur private deployments.

UK policy bans sales of most new petrol cars from 2035 and now mandates payment-card interoperability at public chargers, further strengthening consumer confidence.

In 2024, the North America electric vehicle (EV) charging station market maintains its steady growth, fueled by expanding EV adoption and consistent government support for clean transportation.

The region is seeing more investments in charging infrastructure in urban, suburban, and highway networks to make EV charging more convenient and accessible for consumers. Public and private sectors are working actively to increase the coverage of both Level 2 and DC fast-charging stations, with a specific focus on fixed installations in residential and commercial locations.

Level 2 chargers continue to be dominant because of their cost versus charging speed balance, catering to daily commuting requirements. Residential installations are also increasing at a fast pace as more EV owners find home charging convenient.

The market is expected to grow CAGR of 35.5% from 2025 to 2033.

The current market size is USD 22.46 B7illions in 2024.

Asia Pacific currently holds the largest market shares.

Some of the major players in the electric vehicle charging station market include ABB Ltd., Blink Charging Co., BP plc, ChargePoint Inc., Daimler AG, Eaton Corporation PLC, EFACEC Power Solutions SGPS S.A., Engie SA, EVgo Services LLC (LS Power Development LLC), Renault Group, Schneider Electric SE, SemaConnect, Siemens AG, Tata Power Company Limited, Tesla Inc., etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Electric Vehicle Charging Station Market, By Charger Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Electric Vehicle Charging Station Market, By Vehicle Type

5.3 Electric Vehicle Charging Station Market, By Propulsion Type

6.1 North America Electric Vehicle Charging Station Market , By Country

6.1.1 Electric Vehicle Charging Station Market, By Charger Type

6.1.2 Electric Vehicle Charging Station Market, By Vehicle Type

6.1.3 Electric Vehicle Charging Station Market, By Propulsion Type

6.2 U.S.

6.2.1 Electric Vehicle Charging Station Market, By Charger Type

6.2.2 Electric Vehicle Charging Station Market, By Vehicle Type

6.2.3 Electric Vehicle Charging Station Market, By Propulsion Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping