Connected Car Market

Connected Car Market Share & Trends Analysis Report, By Connectivity Type (Integrated, Tethered), By Application (Navigation, Safety & Security), By Communication Type (V2V, V2I, V2C) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

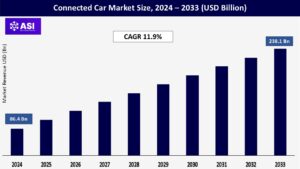

CAGR: 11.9%

Last Updated : January 12, 2026

The Connected Car market was valued at approximately USD 86.4 billion in 2024 and is projected to reach USD 238.1 billion by 2033, expanding at a compound annual growth rate (CAGR) of 11.9% during the forecast period 2025–2033.

Connected cars are vehicles purchase with internet access and wireless local area network (LAN), enabling the cars to share internet access and data with other devices inside and outside the vehicle. The market is continue by increasing demand for driver assistance, in-vehicle infotainment, telematics, and road safety improvements.

Demand for ADAS, remote diagnostics, and in vehicle digital experiences is surging, prompting automakers to deploy connectivity technologies across vehicle segment.

Fastest and low latency 5G networks are open more reliable vehicle to vehicle (V2V), vehicle to infrastructure (V2I) and vehicle to cloud (V2C) communications, supporting autonomous driving and real time updates.

Regulations mandating eCall systems and telematics, particularly in europe and North America, are fostering market growth..

The cost of integrating advanced sensors, processors, and communication modules can be a barrier for entry specially in mid range and budget vehicles.

Growing connectivity increase vulnerability to hacking and data display posing significant risks for manufacturers and users.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application Type |

Safety & Security Infotainment Telematics |

| By Technology Type |

4G/LTE 5G 3G |

| By Connectivity Type |

Embedded Connectivity Tethered Connectivity Integrated Connectivity |

| By Communication Type |

Vehicle to Vehicle (V2V) Vehicle to Infrastructure (V2I) Vehicle to Cloud (V2C) |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Driver Assistance segment continues to dominate the connected vehicle market, commanding approximately 61% of the total market share in 2024.

This significant market position is driven by the increasing integration of advanced driver assistance systems (ADAS) in modern vehicles, ranging from basic features like lane-keeping assistance and adaptive cruise control to more sophisticated functionalities.

The segment’s growth is further bolstered by stringent safety regulations worldwide and rising consumer demand for safer vehicles. The Telematics segment is emerging as the fastest-growing segment in the connected vehicle market, with a projected growth rate of approximately 18% during 2024-2029.

This remarkable growth is driven by the increasing demand for real-time vehicle monitoring, fleet management solutions, and predictive maintenance capabilities. The segment is witnessing significant technological advancements, particularly in areas of data analytics and cloud computing integration.

The Infotainment segment is characterized by the integration of advanced entertainment systems, smartphone connectivity solutions, and voice-controlled interfaces, enhancing the overall user experience in connected vehicles.

This segment continues to evolve with the integration of more sophisticated multimedia systems, navigation capabilities, and connectivity features. The Other Applications segment encompasses various emerging technologies and solutions, including cybersecurity systems and specialized connected vehicle applications, which contribute to the broader ecosystem of connected vehicle technologies.

The 4G/LTE segment maintains a strong presence due to its widespread availability and reliable performance in supporting various connected car features and services.

Meanwhile, the 2G segment, though declining, still serves basic connectivity needs in certain regions and specific applications, particularly in areas where newer network infrastructure is still developing.

The 5G technology segment is experiencing remarkable growth in the connected vehicle market, with an expected growth rate of approximately 70% during 2025-2033.

This explosive growth is driven by the technology’s superior capabilities in handling vast amounts of data generated by connected vehicles, including high-definition maps, traffic data, and vehicle telemetry.

The increased data handling capability is proving crucial for advanced driver assistance systems (ADAS) and autonomous driving technologies market.

The 4G/LTE and 2G segments continue to play important roles in the connected vehicle market, each serving distinct needs and use cases. The 4G/LTE segment maintains a strong presence due to its widespread availability and reliable performance in supporting various connected car features and services.

Meanwhile, the 2G segment, though declining, still serves basic connectivity needs in certain regions and specific applications, particularly in areas where newer network infrastructure is still developing.

The embedded segment continues to dominate the connected vehicle market, holding approximately 83% market share in 2024. Embedded connectivity solutions have established themselves as the cornerstone technology for developing firmware and hardware solutions in connected vehicles.

This segment’s prominence is driven by its ability to enable direct incorporation of internet connectivity within a vehicle’s system architecture, as opposed to relying on external devices.

The integrated segment is emerging as the fastest-growing segment in the connected vehicle market, with a projected growth rate of approximately 23% during 2025-2033.

This remarkable growth is driven by the increasing demand for seamless connectivity solutions and the evolution of vehicle architecture that supports integrated systems.

The tethered connectivity segment represents an important alternative in the connected vehicle market, offering flexibility and cost-effectiveness for certain applications. This segment primarily focuses on solutions that enable connectivity through external devices like smartphones and mobile hotspots.

The Vehicle to Vehicle (V2V) segment continues to dominate the connected vehicle market, holding approximately 65% market share in 2024. This significant market position is driven by the increasing integration of V2V communication technologies that enable vehicles to share critical data about speed, position, and direction with nearby vehicles in real-time.

The Vehicle to Infrastructure (V2I) segment is emerging as the fastest-growing segment in the connected vehicle market, with a projected growth rate of approximately 19% from 2025 to 2033. This remarkable growth is being driven by increasing investments in smart city infrastructure and the deployment of intelligent transportation systems worldwide.

The Vehicle to Pedestrian (V2P) segment represents an important component of the connected vehicle ecosystem, focusing on enhancing safety for vulnerable road users. This technology enables direct communication between vehicles and pedestrians through their mobile devices or smart infrastructure, helping prevent accidents and improve overall road safety.

The Asia-Pacific Connected Car Market is expected to grow at the fastest CAGR from 2025to 2033. This is due to the increasing manufacturing operations developments related to connected services and the adoption of the 5G network for connected cars.

Moreover, China’s Connected Car market held the largest market share, and the Indian Connected Car market was the rapid-growing market in the Asia-Pacific region.

Europe’s Connected Car market accounts for the second-largest market share owing to the increase in investment to enable the adoption of cybersecurity in connected cars and the introduction of new advanced technology by the manufacturers.

Further, the German Connected Car market held the largest market share, and the UK Connected Car market was the rapid-growing market in the European region.

The North America Connected Car Market would witness market growth of 29.9% CAGR during the forecast period (2025-2033). North America adopts new technologies relatively earlier than any other regions.

Factors such as technological advancements and increasing need for connectivity among the customers are the major drivers for the connected car market in the North American region. U.S was one of the first countries to adopt connected cars and M2M connectivity in the automotive sector.

The Middle East Africa Connected Car Market was reached at USD 18.91 billion in 2024. The market growth is continue by a combination of technological improvements, increased customer demand for safety and convenience, and supportive government initiatives.

The increasing accessibility of internet services, increase vehicle production, and a growing focus on smart transportation solutions.

The market is expected to grow USD 11.9 Billions from 2025 to 2033.

The current market size is USD 86.4 Billions in 2024.

North America currently holds the largest market shares.

Cybersecurity and high integration costs.

Key players include Continental AG, Audi, Tesla, Bosch, Ford.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Connected Car Market, By Application Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Connected Car Market, By Technology Type

5.3 Connected Car Market, By Connectivity Type

5.4 Connected Car Market, By Communication Type

6.1 North America Connected Car Market, By Country

6.1.1 Connected Car Market, By Application Type

6.1.2 Connected Car Market, By Technology Type

6.1.3 Connected Car Market, By Connectivity Type

6.1.4 Connected Car Market, By Communication Type

6.2 U.S

6.2.1 Connected Car Market, By Application Type

6.2.2 Connected Car Market, By Technology Type

6.2.3 Connected Car Market, By Connectivity Type

6.2.4 Connected Car Market, By Communication Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping