Autonomous Last Mile Delivery Market

Autonomous Last Mile Delivery Market Size, Share & Trends Analysis Report By Platform Type (Ground Delivery bots , Aerial Delivery Drones, Autonomous Vehicles), By Range (Short-Range, Long-Range), By Application (Retail, Food & Beverages, Healthcare, Logistics,) – Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

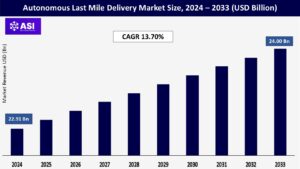

CAGR: 13.70%

Last Updated : February 5, 2026

The autonomous last mile delivery market size reached USD 21,940.1 million in 2025. Looking forward, IMARC Group expects the market to reach USD 6330.2 million by 2033, exhibiting a growth rate (CAGR) of 18.4% during 2025-2033.

The autonomous last-mile delivery market focuses on the use of self-driving vehicles, ground robots, and aerial drones to transport goods from distribution hubs to end users. This market has gained attention due to the growth of e-commerce, rising urban congestion, and increasing demand for faster and contactless delivery solutions. Retailers, logistics providers, and food delivery platforms are exploring autonomous delivery to reduce dependency on manual labor and manage operational costs.

Technological developments in artificial intelligence, sensors, computer vision, and navigation systems have supported the gradual adoption of autonomous delivery solutions. Urban areas are emerging as early adoption zones because of shorter delivery distances and higher order volumes. However, regulatory uncertainty, infrastructure limitations, and safety concerns continue to influence deployment timelines across regions.

The market includes a range of vehicle types such as delivery robots, autonomous vans, and drones, with pilot projects and limited commercial deployments currently underway. As regulations evolve and public acceptance improves, autonomous last mile delivery is expected to see wider integration into existing logistics networks.

New vehicles are changing the face of last mile delivery services. Major companies are experimenting & investing in R&D on new solutions to combat rising customer demand.

Moreover, rapid progress in delivery technologies such as artificial intelligence (AI) based autonomous delivery vehicles, drones, and others is directly helping by reducing dependency on worker availability, driving down the labor costs, and also enables around clock delivery.

Furthermore, many giant retailers are testing unmanned parcel delivery products. In January 2024, Baylor University launched Starship Technologies’ robot food delivery service, utilizing a fleet of 20 autonomous robots.

These robots currently deliver from seven campus eateries, including Panda Express, Steak ‘n Shake, two Starbucks locations, Which Wich, Moe’s, and Rising Roll. T

Through the Grubhub app on iOS and Android, the university’s over 20,000 students, faculty, and staff are able to order food and beverages from these eateries, with delivery to any campus building typically taking just minutes.

The growth of the autonomous last mile delivery market is limited by the payload capacity. When technologies like drones and small robotic vehicles offer advantages in speed and accessibility, their ability to carry heavier or larger payloads is restricted.

This limitation affects the effective delivery of certain products using autonomous systems, especially those that surpass weight or size limits. Industries handling bulkier or specialized cargo, such as furniture, appliances, or industrial equipment, might find it impractical to use these autonomous solutions.

Furthermore, businesses requiring multiple items to be transported in a single delivery may create many conflicts due to the limited payload capacity of autonomous vehicles; this can lead to increased operational complexity and costs through multiple trips or deliveries.

Therefore, while autonomous last mile delivery proves suitable for specific applications, its payload limitations present a significant obstacle to wider acceptance. This necessitates the development of innovative solutions that address these constraints and expand the market’s possibilities.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Application |

Retail Logistics Food and Beverage Healthcare and Pharmaceutical |

| By Range Type |

Long Range Short Range |

| By Vehicle Type |

Ground Delivery Bots Delivery Bots Self-driving Vans & Trucks |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

In 2024, the ground delivery bots’ sector had the highest market share on the basis of the vehicle type. Ground delivery bots, also known as sidewalk robots or ground drones, are compact and autonomous vehicles specifically designed to navigate sidewalks and pedestrian-friendly areas.

These innovative machines directly transport goods to customers’ doorsteps. Increasing popularity in both urban and suburban environments, these delivery bots offer a solution for suitable and contineous last mile deliveries.

They come out several advantages such as alleviating traffic congestion, reducing delivery costs, and providing contactless deliveries an aspect of utmost importance during the COVID-19 pandemic.

The aerial delivery segment will hold the second-largest share. Aerial delivery drones are more widely used in autonomous last-mile delivery services since they travel by air and avoid traffic jams and other problems that could interfere with product delivery.

During the projection period, this is anticipated to increase the use of aerial delivery drones in the last-mile autonomous delivery market. Aerial Delivery Drones are used in areas with limited road access or to overcome urban traffic.

Ideal for urgent or lightweight deliveries, drones can fly directly to homes, bypassing congested streets. Zipline, Wing, and Amazon Prime Air are pioneers in drone logistics.

The market for last-mile delivery is largely running by the autonomous vehicles segment, which includes delivery robots, pods, and self-driving vans. These vehicles are made to move cargo without the need for human assistance; they frequently combine LiDAR, GPS, cameras, and artificial intelligence (AI) to navigate safely in suburban and urban settings.

With their high efficiency and low cost per delivery, they are perfect for route-based or bulk neighborhood deliveries. At the forefront are businesses like Nuro, Boxbot, and Starship Technologies, which collaborate with significant grocers and retailers.

The short-range segment of the autonomous last mile delivery market is a fastly improving and dynamic sector. It focuses on providing beneficial and localized autonomous delivery solutions, primarily within urban or suburban environments.

These solutions encompass small autonomous vehicles, sidewalk robots, and drones optimized for quick and convenient deliveries. They cater to a wide array of goods including groceries, takeout food, medications, and packages from local businesses.

Long-range parcel delivery robots/products include ground delivery bots and self-driving trucks& vans, which deliver last mile services to customers’ doorsteps.

In addition, the companies have carried out numerous developments in the last mile delivery system/services, which is expected to foster the growth of the long-range (>20km) market in the forecast period.

According to the application, the retail sector has held the major revenue share in 2024. Retailers are increasingly using autonomous technologies to optimize their delivery operations. Self-driving vehicles, drones, and robots are among the innovative technologies that offer numerous advantages.

These improvements make delivery times quicker and more less delivery times, cost reduction, and increased customer satisfaction. By integrating these technological innovations into various industries, businesses can reap significant benefits while improving their overall performance.

The food & beverage section will acquire the second-largest market shares. The food & beverage industry utilizes last mile delivery services to complete orders on time and efficiently without much human effort or error.

The drone delivery service has undergone advancements from several businesses to deliver food goods to clients effectively. For instance, the Icelandic company AHA and the North Carolina company Flytrex debuted a drone delivery service in 2017 and were working to increase their food delivery services in Raleigh.

Autonomous delivery systems are being fastly assumed by the healthcare industry to improve the speed, accuracy, and safety of moving medical supplies. Vaccines, blood samples, drugs, and medical equipment are delivered by drones and self-driving ground vehicles, especially in isolated or disaster-affected areas.

In order to increase operational efficiency and reduce costs, logistics providers are major players in the deployment of autonomous last mile delivery technologies.

Companies like UPS, FedEx, and DHL are using autonomous bots, drones, and delivery vehicles to complete deliveries in cities and suburbs due to rising fuel prices and a shortage of drivers. Particularly in high-demand e-commerce settings, these technologies aid in streamlining routes, decreasing the need for labor, and increasing delivery frequency.

APAC is acquired the largest 26% market shares of the global markets. The APAC region is projected to be the fastest-growing region in the vehicle recycling market, with a compound annual growth rate (CAGR) of around 7% expected through 2034.

This rapid growth is being fueled by several interlinked factors, including soaring automotive sales, rapid urbanization, and a rising awareness of sustainability issues.

Countries such as China, India, and Japan are at different stages of developing national vehicle scrappage policies and investing in formal recycling infrastructure. In particular, China’s aggressive push towards circular economy practices and India’s new Vehicle Scrappage Policy are creating favorable conditions for market expansion.

Europe stands as the second-largest player in global market with 28% . Europe is envisaged to hold USD 27,286 million, growing at a CAGR of 25.1%.

To promote the autonomous last-mile delivery industry throughout the region, the major players in the European autonomous last mile delivery market share, including Airbus, Savioke, Starship Technologies, and others, are developing a variety of autonomous last-mile delivery vehicles, including drones, ground delivery bots, and self-driving trucks & vans.

North America region represents 35% market. North America will likely command the market while expanding at a CAGR of 26.6%. Numerous businesses have been able to innovate due to the region’s increased use of automation in last mile delivery services, which supports the expansion of the autonomous last mile delivery market share there.

Customers are increasingly attracted to shop online for everyday necessities like groceries and medicines as a precautionary strategy to avoid human-to-human connection or contact due to the pandemic’s adverse effects across North America.

MEA Acquired approximately 11% of the global market share. Although it is still in the early stages of implementing autonomous last-mile delivery technologies, the MEA region is making encouraging progress.

In nations like Saudi Arabia and the United Arab Emirates, where smart city initiatives promote automation and innovation, pilot programs are being tested. These initiatives frequently focus on healthcare logistics, such as the transportation of medications, immunizations, and laboratory samples, particularly in isolated or rural locations.

The market was valued at USD 22.91billion in 2024.

The market is projected to grow at a CAGR of 13.70% from 2025 to 2033.

The short-range segment is predicted to expand at a CAGR of 22.9% and hold the largest share.

North America region has highest growth rate.

Airbus SAS, Matternet, Flirtey, Drone Delivery Canada, Flytrex, Amazon.com, are the top players in the market.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Autonomous Last Mile Delivery Market, By Application

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Autonomous Last Mile Delivery Market, By Range Type

5.3 Autonomous Last Mile Delivery Market, By Vehicle Type

6.1 North America Autonomous Last Mile Delivery Market , By Country

6.1.1 Autonomous Last Mile Delivery Market, By Application

6.1.2 Autonomous Last Mile Delivery Market, By Range Type

6.1.3 Autonomous Last Mile Delivery Market, By Vehicle Type

6.2 U.S.

6.2.1 Autonomous Last Mile Delivery Market, By Application

6.2.2 Autonomous Last Mile Delivery Market, By Range Type

6.2.3 Autonomous Last Mile Delivery Market, By Vehicle Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping