Automotive Trim Market

Automotive Trim Market Size, Share & Trends Analysis Report By Material Type (Polypropylene (PP), Polyoxymethylene (POM)), By Interior Application (Dashboard, Door panel), By Exterior Application (Bumpers, Door & window seals), By Vehicle Type (Passenger Car, Light Commercial Vehicle, Electric Vehicles), Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

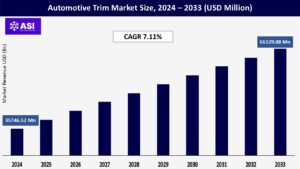

CAGR: 7.11%

Last Updated : February 5, 2026

The global automotive trim market size was valued at USD 35746.52 million in 2024 and is expected to grow from USD 38288.1 million in 2025 to reach USD 66329.08 million by 2033, growing at a CAGR of 7.11% during the forecast period (2025-2033).

Automotive trims are plastic parts fitted in cars to improve their looks and functionality. The unique features of a vehicle are described by the trims used on it. Many parts in a car, including the front and rear bumpers, the dashboards, and similar ones, describe various trims used more often in vehicles.

Numerous automotive component manufacturers have developed and introduced lightweight and robust car components comprised of multiple polymers. These parts are used more frequently in automobiles, which positively impacts the expansion of the worldwide automotive trims market.

The demand for more comfort and luxury in automobiles and a quieter interior has dramatically fueled the expansion of the worldwide automotive trims market. Manufacturers that produce efficient automotive trims and provide their goods to the automotive sector include Gronbach, Grupo Antolin, International Automotive Components, and Kasai Kogyo Co., Ltd.

In addition, it is predicted that the sale of luxury vehicles will double by 2020 due to improvements in vehicle technology and the expansion of the economies of developing nations.

Furthermore, a vehicle’s noise, vibration, and harshness (NVH) performance must fulfill traditional values to comfort and lessen vibrations inside the cabin. Thus, combining these variables helps the global market for automotive trims flourish.

Additionally, countries like China, the US, Japan, India, Germany, and the UK have experienced significant automotive industry expansion over the past ten years. Japan, the United States, and Germany were initially the industrialized nations on which the global automotive industry concentrated.

However, businesses have moved their manufacturing operations there because of the rise in demand for cars and automotive parts in these nations, such as China, Thailand, and India.

Low labor costs allow manufacturers to produce more products at lower prices, which helps them meet rising demand, which is expected to increase car sales over the projected period. Which will successively grow the market for automotive trim.

The primary driver behind the automotive interior trim parts market growth is the surging production and sales of vehicles. As the global demand for automobiles increases, there is a parallel increase in the demand for interior trim components to equip these vehicles.

Advancements in automotive technology contribute to the demand for sophisticated interior components. Features such as advanced connectivity, smart interfaces, and integrated electronics require corresponding innovations in interior trim parts.

Since many of the parts that make a car are more expensive, their constant replacement is impractical. As a result, vehicle makers fit more robust, durable, and reasonably priced components into cars and trucks that can operate in any climate.

Additionally, the high cost of component replacement contributes to an increase in car prices, which is predicted to restrain market expansion. Consumers would have to pay more for hardware, software, and other components if cars offered premium features, which would eventually restrain the market’s expansion.

Furthermore, their numerous components and sensors make such vehicles challenging to service and call for specialized personnel. Systems with complex architectures have shorter service lives. Therefore, it is anticipated that high replacement costs will hinder the expansion of the worldwide automotive trims market.

One of the key restraints in this market is the volatility in raw material prices. Automotive interior trim parts are often made from a variety of materials, such as plastics, leather, metals, and textiles. Sudden increases in the prices of these raw materials significantly raise production costs for manufacturers.

This, in turn, limits profit margins and makes it challenging for companies to stay competitive in the market. When raw material prices rise, manufacturers may face the difficult decision of either absorbing the increased costs, which can impact profitability or passing them on to consumers through higher prices.

Higher prices, however, may lead to reduced demand among consumers, affecting the overall market growth. The automotive industry heavily relies on materials such as plastics, leather, textiles, and various metals for interior trim components. Thus, fluctuations in the prices of these raw materials can significantly impact the manufacturing costs for interior trim parts.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Material Type |

Polypropylene Polyoxymethylene |

| By Interior Type |

Dashboard Door Panel |

| By Exterior Type |

Bumpers Window & Door Seals |

| By Vehicle Type |

Passenger Cars Light Commercial Vehicle Electric Vehicles |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The polypropylene (PP) section will presumably grow at a CAGR of 7.3% and hold the largest revenue share. Polypropylene (PP) may be changed for various applications and is considered a more robust plastic material.

Its ability to be widely employed in the production of various automotive components, its outstanding resistance to corrosion, and its ability to operate as an insulator, among many other characteristics, have contributed to the segment’s expansion.

The polyoxymethylene (POM) section will hold the second-largest share. Due to its good stiffness, rigidity, and yield strength, polyoxymethylene (POM) is a material that can be used in the automotive sector.

Its excellent chemical and fuel resistance and other properties make it a favored polymer for usage in the automotive industry to build various components, including multiple trims.

The dashboard section will presumably expand at a CAGR of 7.5% and hold the largest share. Vehicle dashboards are fitted to carry out various functions, including showing the vehicle’s meters. They are also used to equip dash cameras and other components, supporting the segment’s global market growth.

This growth is driven by the increasing popularity of SUVs and crossovers, which typically feature more exterior trim than sedans or coupes. The lighting segment is another important application of automotive trim.

The growing adoption of LED and OLED lighting systems is expected to drive the growth of this segment in the coming years. The door panel section will hold the second-largest share.

One of the most essential parts of a car is the door panels since they offer dependable side protection, ergonomic comfort, and convenience, as well as beautiful and soft-touch surfaces.

The bumpers section is presumed to hold the largest share, growing at a CAGR of 7.25%. The hood, trunk, grill, fuel, exhaust, and cooling systems of the car are all protected by bumpers.

They serve as shock absorbers because they are made of steel, aluminum, rubber, or plastic, protecting the vehicle from harm. These characteristics allow the producers to create robust bumpers, supporting the market’s expansion.

Bumpers are particularly important as they enhance safety while also influencing the vehicle’s design. Grilles, acting as both protective barriers and design features, contribute to the vehicle’s cooling systems and overall appearance.

The window & door seals section will hold the second-largest share. Window and door seals in automobiles guard against weather-related threats, including snow, rain, dust, and grime.

The window and door seals come in various lengths and sizes, which contributes to their adaptability. These elements support the development of window and door seals.

Passenger Cars dominated the segment and generated over 45% of the total revenue. The reasons for such a tendency include the increasing production and sales of passenger vehicles on the global market.

Moreover, the growing popularity of SUVs and Pickups will also drive the demand for the automotive trim market. These types of transport are favored for their convenience, breathing space, and off-road capacity.

The passenger vehicle section is presumed to have the highest shareholding and grow at a CAGR of 6.87%. The passenger car segment consists of cars with internal combustion engines that are used for people’s transportation, including compact cars, hatchbacks, sedans, luxury sedans, and others.

The development of electric vehicles by various automakers contributes to the expansion of the passenger automobile market. Ford, General Motors, and other companies have made several investments and improvements to support the segment’s growth.

Light commercial vehicles (LCVs) also represent a significant segment within the automotive trim part market. LCVs are commonly used for goods transportation and small-scale commercial activities.

The demand for LCVs is driven by the growth of e-commerce, urbanization, and the need for efficient logistics solutions. The use of durable and high-strength trim parts in LCVs is essential to withstand the rigorous usage conditions.

Additionally, the growing trend towards customization and branding in commercial vehicles is driving the demand for specialized trim parts that enhance the visual appeal and functionality of LCVs.

Electric vehicles (EVs) represent a rapidly growing segment in the automotive trim part market. The shift towards sustainable and eco-friendly transportation solutions is driving the adoption of EVs globally.

In the EV segment, the demand for lightweight and innovative trim parts is particularly high to enhance vehicle efficiency and range. The use of advanced materials, such as composites and lightweight metals, is gaining traction in EVs.

Additionally, the integration of advanced electronics and smart features in EVs necessitates the use of specialized interior trim components, further supporting the growth of this segment.

The OEM section will presumably expand at a CAGR of 7.6% and have the most significant shareholding. Due to the rising adoption of functional components in vehicles, OEMs are becoming more prominent in the automotive trims industry.

Additionally, the development of technology has made it possible for consumers to select efficient auto parts, which has fueled the global market expansion.

OEM trims are installed during the production and assembly of the vehicle; these beams are produced by major players in the market and supplied to Automotive manufacturers for direct installation. These trim materials and fabrication processes have the highest quality and strict quality control.

The aftermarket section will have the second-largest share. The aftermarket provider is used to upgrade the existing automobiles with new parts or to repair a damaged item in a vehicle.

As a result, the aftermarket is growing in popularity for the automotive trim service because customers want to add cutting-edge parts to their cars to increase driving safety.

The aftermarket, on the other hand, represents a significant distribution channel for automotive trim parts. The aftermarket includes independent suppliers, retailers, and service providers that offer replacement and upgrade parts for vehicles.

The Asia Pacific will likely hold the predominant share while advancing at a CAGR of 7.6%. It is anticipated that market participants in the Asia Pacific will generate considerable returns throughout the forecast period.

This is primarily due to the growing urban population, rising disposable incomes, and growing manufacturing operations in various Asian countries.

Additionally, the ever-increasing desire for automobile manufacturers to improve quality by reducing unpredictability and removing faults to enhance comfort while driving any vehicle and assistance is also supporting the growth of the Asia Pacific automotive trimmings business.

The expansion of the Asia-Pacific region is being fueled by both an increase in the population of vehicles and an increase in the criteria for cars. In addition, several technological breakthroughs about trims are currently taking place, followed by the launch of more robust components, which drives the expansion of the market.

Europe will have the second-largest shareholding of USD 14,217 million, growing at a CAGR of 7.95%. Companies like the Draxlmaier Group have operations throughout Europe to produce and introduce appropriate automotive trims.

This aids in the expansion of the global market in Europe. The expanded product range that businesses offer contributes to developing international automotive trims in Europe.

Since 2010, both demands for and sales of passenger automobiles have been on the rise thanks to an increase in the worldwide population and the amount of disposable income available in many emerging countries.

Customizing interior and exterior trim pieces according to a customer’s specific request is one way that manufacturers emphasize the provision of consumer-centric components

North America was the highest revenue contributor and is estimated to grow at a CAGR of 40.8%. The North American region includes countries such as the U.S., Canada, and Mexico.

The launch of a new range of self-driving buses on roads to offer transportation services to passengers and government initiatives for the development of driverless buses are anticipated to propel the growth of the self-driving bus market in North America.

Leading bus manufacturers are launching autonomous technology programs to develop and deploy self-driving buses. For instance, Flyer, a bus manufacturer, has launched an autonomous technology program to deploy driver-assist and self-driving technology for public transit agencies.

The automotive trim market is expected to grow CAGR of 7.11% from 2025 to 2033.

The current automotive trim market size is USD 35746.52 million in 2024.

Asia Pacific currently holds the largest automotive trim market shares.

Top industry players in the automotive trim market are Draexlmaier Group, Dura Automotive Systems Inc., Gemini Group, Inc., Hella, Grupo Antolin, Cooper, Kasai Kogyo Co., Ltd., Adient, etc.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Trim Market, By Material Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Trim Market, By Interior Type

5.3 Automotive Trim Market, By Exterior Type

5.4 Automotive Trim Market, By Vehicle Type

6.1 North America Automotive Trim Market, By Country

6.1.1 Automotive Trim Market, By Material Type

6.1.2 Automotive Trim Market, By Interior Type

6.1.3 Automotive Trim Market, By Exterior Type

6.1.4 Automotive Trim Market, By Vehicle Type

6.2 U.S.

6.2.1 Automotive Trim Market, By Material Type

6.2.2 Automotive Trim Market, By Interior Type

6.2.3 Automotive Trim Market, By Exterior Type

6.2.4 Automotive Trim Market, By Vehicle Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping