Automotive Part Die Casting Market

Automotive Part Die Casting Market Share & Trends Analysis Report, By Process Type (Pressure Die-Casting, Vacuum Die-Casting, Squeeze Die-Casting, Gravity Die-Casting) By Raw Material Type (Aluminum, Zinc, Magnesium,) By Application Type (Body Assemblies, Engine Parts, Transmission Parts,) Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

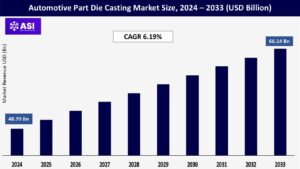

CAGR: 6.19%

Last Updated : March 13, 2026

The Automotive Parts Die Casting Market size is estimated at USD 48.99 billion in 2025, and is expected to reach USD 66.14 billion by 2033, at a CAGR of greater than 6.19% during the forecast period (2025-2030).

The automotive parts die casting market is experiencing a significant transformation driven by technological advancements and changing manufacturing paradigms. Global vehicle production reached approximately 85 million units in 2022, highlighting the robust demand for automotive metal components and die-cast parts.

The increasing emphasis on fuel efficiency and emissions reduction is propelling the demand for lightweight vehicles across the automotive industry. The Automotive Parts Die-Casting Market Industry plays a significant role in this trend by enabling manufacturers to produce lightweight components that contribute to overall vehicle weight reduction.

As automotive manufacturers are under pressure to comply with stringent environmental regulations, die casting technology becomes essential for producing high-performance parts without compromising on structural integrity.

Advancements in die casting technology are significantly improving production efficiency and part quality, which are crucial for the Automotive Parts Die-Casting Market Industry.

Enhanced techniques such as low-pressure die casting, high-pressure die casting, and the use of new materials are expanding the capabilities of manufacturers to produce complex and highly intricate automotive parts.

Automotive parts die casting market growth would be hampered by the increasing volatility in aluminum, magnesium, and zinc prices. The raw materials are essential in the die casting process, and the supply chain disruptions cause capital losses to the manufacturers in the automotive industry.

Such price volatility can also reduce the adoption of automotive parts die casting in the future, further hindering the market’s growth. On the other hand, the requirement of high initial cost and high cost associated with the raw materials for the process are expected to obstruct market growth.

Also, stringent regulations associated with the process are projected to challenge the automotive parts die casting market in the forecast period of 2025-2033.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Process Type |

Pressure Die-Casting, Vacuum Die-Casting Squeeze Die-Casting Gravity Die-Casting |

| By Raw Material Type |

Aluminum Zinc Magnesium |

| By Application Type |

Body Assemblies Engine Parts Transmission Parts |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The pressure die-casting segment dominated the market, with a market share of around 44.44% in 2024. Pressure Die Casting stands out as one of the prominent methods employed in the industry. This process involves injecting molten aluminum into a steel mold cavity at high pressure.

The molten metal is forced into the mold, resulting in precise and intricate shapes. In 2024, the Pressure Die Casting segment was valued at 12478.9 USD Million, underlining its significant contribution to the market.

Vacuum Die Casting is another notable production process in the automotive parts aluminum die casting market. In this method, a vacuum is applied to the mold cavity before the molten aluminum is injected.

This helps in reducing air and gas porosity in the final product, resulting in higher-quality parts. The Vacuum Die Casting segment was valued at 3390.4 USD Million in 2024, indicating its considerable market share.

Squeeze Die Casting is characterized by applying additional pressure to the mold after the initial injection of molten aluminum. This process helps in further compacting the metal and improving the mechanical properties of the final product.

The Squeeze Die Casting segment accounted for a value of 2690 USD Million in 2024, showcasing its significance in the market. Gravity Die Casting, while not as widely used as the aforementioned methods, still holds its place in certain applications.

Unlike other processes that rely on high pressure, Gravity Die Casting utilizes gravity to fill the mold cavity with molten aluminum. Although it may not offer the same level of intricacy as other methods, it remains a cost-effective solution for producing certain automotive parts.

The Global Automotive Parts Aluminium Die Casting market experiences growth due to several key factors. One significant driver is the increasing demand for lightweight automotive components. This demand stems from the desire to enhance fuel efficiency in vehicles.

Consumers and manufacturers alike seek solutions that can reduce the overall weight of vehicles, thereby improving their fuel economy. This emphasis on lightweighting has propelled the use of aluminium die casting in automotive parts production.

Magnesium is emerging as a preferred option owing to its exceptional strength-to-weight ratio, contributing to overall weight reduction in vehicles. Cast Iron remains a reliable choice for components requiring robustness and thermal resistance.

Copper serves a specific niche, particularly in applications demanding high electrical conductivity. As manufacturers seek to innovate and improve their product offerings, the diverse capabilities and properties of these materials create numerous opportunities across the Global Automotive Parts Die Casting Market.

Zinc die casting is used to manufacture the vehicle safety component, including seat belts and other parts such as brakes, sunroofs, and many others. In order to reduce automobile emissions and increase fuel efficiency, CAFÉ standards and EPA policies are driving automakers to reduce the weight of the automobile by employing lightweight non-ferrous metals.

Employing die-cast parts as a weight reduction strategy is a major driver for the automotive segment of the market. Although heavier than aluminum, the lower cost of these parts and higher intricacy allowance make them more suitable in certain applications.

The BFSI (Banking, Financial Services, and Insurance) sector has undergone a conversion impact from Autonomous AI and Autonomous Agents, a change in what ways financial institutions deliver services.

These advanced technologies offer unparalleled opportunities for automation, increasing decision-making, and improving customer experiences.

Autonomous AI systems in the BFSI sector employ machine learning procedures to analyze expansive amounts of financial data, detect patterns, and make autonomous decisions in areas such as fraud detections risk management, and investment strategies.

The transmission parts segment dominated the market, accounting for around 43.13% of global revenue. Transmission parts are involved in the primary function of a vehicle, i.e., movement.

The critical importance of transmission makes it the most dominant sub-segment. It is produced on a larger scale than other automotive parts for new vehicles and for repairing/replacing.

The Asia Pacific region emerged as the largest market for the global automotive parts die casting market, with a 45% share of the market revenue in 2024. The Asia Pacific currently dominates the automotive parts die casting market due to an increase in the disposable income of consumers, which has led to a rise in demand for vehicles.

Asia-Pacific is expected to rise in the forecast period due to the adoption of new policies by the government. The new policies encourage the adoption of automotive parts die casting.

The most important 20% markets for automotive part die casting in Europe during the anticipated period are expected to be Germany, Italy, and Russia. At the moment, die casters in Europe are concentrating on high-end vehicles like the new Jaguar I-Pace, BMW 8 Series, and Mercedes-Benz C-Class.

Rheinmetall AG, GF Automotive, Martinrea, Nemak, and Alucast are just some of the major players in Europe’s automotive part die casting market.

North America acquired the 25% market share of the global market. North America is expected to grow during the forecast period. Rising demand for cars and light trucks means a booming market for automotive die casting in North America.

As reported by the Mexican Automobile Manufacturers Association (AMIA), the demand for automotive die-cast part suppliers in Mexico is expected to grow to nearly 3.8 million in 2024. In the United States alone, over 30 die-casting companies employ over 400 die-casting plants to produce auto parts for engines and transmissions.

MEA acquired only 10% market share. Over the forecast period, the die-casting market for automotive components is expected to expand significantly in the Middle East and Africa. Die casting for automotive parts is expected to increase in the Middle East and Africa as automakers look for ways to cut vehicle weight.

State and local governments in countries like Argentina and Brazil are creating opportunities for foreign investors by providing the auto manufacturing industry with various incentives, which bodes well for the growth of the die-casting market in LAMEA.

The current automotive part die casting market size is USD 48.99 billion in 2025.

The global automotive part die casting market is growing at a CAGR of 9.8% during the forecasting period 2025-2033.

The Asia Pacific region held the highest share in 2024 of the automotive part die casting market.

The Global Market is studied from 2025 to 2033.

Georg Fischer Limited, Kspg Ag, Ryobi Aluminum Casting Ltd., Teksid, Trimet Aluminum Se, Martinrea Honsel, Montupet S.A., Ksm Castings, ALBERT HANDTMANN, METALLGUSSWERK Gmbh and CO. KG, Brabant Alucast, Saint Jean Industries, Officine Meccaniche Rezzatesi.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Automotive Part Die Casting Market, By Process Type

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Automotive Part Die Casting Market, By Raw Material Type

5.3 Automotive Part Die Casting Market, By Application Type

6.1 North America Automotive Part Die Casting Market , By Country

6.1.1 Automotive Part Die Casting Market, By Process Type

6.1.2 Automotive Part Die Casting Market, By Raw Material Type

6.1.3 Automotive Part Die Casting Market, By Application Type

6.2 U.S.

6.2.1 Automotive Part Die Casting Market, By Process Type

6.2.2 Automotive Part Die Casting Market, By Raw Material Type

6.2.3 Automotive Part Die Casting Market, By Application Type

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping