Tin Catalyst Market

Tin Catalyst Market & Trends Analysis Report, By Grade (Leading Segment: Dibutyltin Dilaurate (DBTDL), Octoate Stannous), By Application (Polyurethane: The Most Common Use, Silicones), By End-Use Industry (Automotive, Construction), By Distribution Channel (One of the main channels is direct sales, Online Platforms)– Industry Analysis Report, Regional Outlook, Growth Potential, Price Trends, Competitive Market Share & Forecast, 2025–2033.

Historical Period: 2019-2024

Forecast Period: 2025-2033

Report Code :

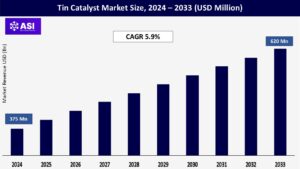

CAGR: 5.9%

Last Updated : March 7, 2026

The global tin catalyst market size was valued at approximately USD 375 million in 2024 and is projected to reach USD 620 million by 2033, growing at a CAGR of 5.9% during the forecast period. Tin catalysts, primarily organotin compounds, are widely used in accelerating chemical reactions across various industries, including plastics, adhesives, and coatings.

Growth is driven by the increasing demand for high-performance catalysts in polymer production, sustainability efforts in chemical processing, and rising consumption of polyurethane and silicone-based products in automotive and electronics sectors.

Technological advancements, particularly in eco-friendly and low-toxicity tin catalyst formulations, are also fostering market expansion.

Tin catalysts are necessary for the production of silicone-based elastomers and polyurethane foams. The need for tin catalysts is being driven by the expanding use of these materials in electronics, medical gadgets, building insulation, and automobile seating. One of the main drivers of growth is the rise of the automobile and construction industries, especially in Asia and North America.

Tin catalysts are being used more frequently in a variety of manufacturing industries due to the accelerated industrial expansion in areas like the Middle East, Latin America, and Asia-Pacific.

These include the paint and coating, adhesive, sealant, and plastic processing industries, where catalysts are essential for improving the quality of the final product and the efficiency of reactions.

Numerous organotin chemicals are hazardous and endanger the environment and human health. The use of dangerous tin-based compounds is restricted by strict laws, particularly in Europe, which could hinder industry expansion.

Industries looking for greener solutions are changing their choices as a result of the growing discovery of alternative catalysts (such as those based on zinc and bismuth) that are less harmful.

| Report Metric | Details |

|---|---|

| Segmentations | |

| By Grade |

Leading Segment: Dibutyltin Dilaurate (DBTDL) Octoate Stannous |

| By Application |

Polyurethane: The Most Common Use Silicones |

| By End-Use Industry |

Automotive Construction |

| By Distribution Channel |

One of the main channels is direct sales. Online Platforms: A New Development |

| Key Players |

|

| Geographies Covered | |

| North America |

U.S. |

| Europe |

U.K. |

| Asia Pacific |

China |

| Middle East & Africa |

Saudi Arabia |

| Latin America |

Brazil |

The Tin Catalyst Market is segmented by Function (Acidulant, Emulsifier, Diuretic), By End-Use (Food & Beverage, Pharmaceuticals, Personal Care, Industrial). Each factor plays a crucial role in enhancing patient safety, increasing the adoption of self-administered anticoagulant therapies, and supporting the development of more convenient, prefilled drug delivery systems that streamline treatment in the management of thromboembolic and cardiovascular conditions.

Leading Segment: Dibutyltin Dilaurate (DBTDL)

Due to its exceptional catalytic efficiency in the manufacture of silicone and polyurethane, dibutyltin dilaurate has the biggest market share. It is the most extensively used tin-based catalyst across sectors due to its wide compatibility with different formulations and lengthy history of commercial use.

Octoate Stannous

The main application for stannous octoate is in the manufacturing of polyurethane foams, especially flexible foams for furniture and car interiors. Because of its strong catalytic activity and affordability, it is still a popular option for high-volume foam production applications.

Polyurethane: The Most Common Use

Tin catalysts are most commonly used in the manufacturing of polyurethane. These catalysts are frequently used in the production of elastomers, adhesives, sealants, varnishes, and flexible and rigid polyurethane foams (CASE).

Tin catalysts improve the mechanical and thermal qualities of the end product, increase the rate of reaction, and regulate the structure of polymers, particularly dibutyltin dilaurate and stannous octoate.

The construction, automotive, furniture, and packaging sectors are the main drivers of the global spike in demand for polyurethane, which is fueling market expansion. Lightweight polyurethane foams are used for energy-efficient insulation in construction and to increase interior comfort and fuel efficiency in automobile manufacturing.

Tin catalysts continue to be essential for fulfilling changing material performance demands as lightweight car designs and sustainable building techniques gain popularity.

Silicones

One rapidly growing application area for tin catalysts is the silicone market. Numerous items, such as elastomers, lubricants, adhesives, sealants, and medical-grade materials, contain silicones.

For silicone goods to have the appropriate elasticity, toughness, and temperature tolerance, effective cross-linking and curing procedures are made possible by tin catalysts. The need for high-performance silicones is increasing due to the expansion of end-use industries like electronics, healthcare, and construction.

Tin catalysts are essential for maintaining product performance and consistency in specialty-grade silicone compounds, which are becoming more and more necessary due to the growth of wearable technology, medical implants, and electric cars. The use of tin-catalyzed silicones is further increased by the building industry’s need for weather-resistant sealants and adhesives.

Automotive

One of the biggest final consumers of silicone and tin-catalyzed polyurethane is the automotive sector. Lightweight parts, flexible foams, acoustic insulation, adhesives, gaskets, and coatings are all made with these materials.

Enhancing vehicle comfort, safety, and fuel efficiency requires effective curing and bonding processes, which are made possible by tin catalysts. Advanced polymeric materials are becoming more and more in demand as the industry moves toward electric vehicles (EVs) and lighter designs to fulfill emission and mileage objectives.

Silicones are crucial for sealing and thermal management applications, while polyurethane foams are utilized in automobile seats, headliners, and door panels. Both of these applications depend on tin-based catalysts for reliable performance and efficient production.

Construction

Because tin catalysts are used to make polyurethane foams, sealants, and elastomers, the construction industry is another important end-use market for them. In both residential and commercial constructions, these materials are essential for gap filling, insulation, waterproofing, and structural bonding.

Tin catalysts are crucial for large-scale, quick-paced building projects because they improve cure speed, adhesion, and durability. High-performance insulating materials, low-VOC sealants, and long-lasting adhesives—all of which benefit from tin-catalyzed chemistry—have become more widely used as a result of the growing emphasis on sustainable construction, energy efficiency, and green building certifications (such as LEED and BREEAM).

Infrastructure development is booming in emerging economies in Latin America, the Middle East, and Asia-Pacific, which is driving up demand in this market.

One of the main channels is direct sales.

Since these products need specific handling, storage, and regulatory compliance, direct sales account for the majority of the tin catalyst business. Manufacturers usually sell to industrial end users directly or through technical, authorized distributors.

When working with reactive or dangerous substances, this route guarantees that product specifications, safety precautions, and technical assistance are properly communicated.

In order to preserve supply chain dependability, quality control, and regulatory traceability, industrial buyers—including producers in the polyurethane, silicone, adhesives, and coatings sectors—prefer direct procurement. Technical service packages and long-term supply agreements are typical in this channel, especially for large-scale businesses.

Online Platforms: A New Development

Online platforms for chemical procurement are becoming more popular, despite being a niche market at the moment, especially among research institutes and small- to medium-sized customers.

Specialty catalysts in lower quantities are now more easily accessible because to the growth of online chemical markets and e-commerce websites, which also provide technical datasheets, safety data sheets, and certificates of analysis (COAs).

The growing desire for speedy delivery, price transparency, and convenience is driving online distribution. Its wider use for tin catalysts is nevertheless constrained by issues including regulatory limitations, the requirement for thorough expert consultation, and restricted logistics capabilities for hazardous materials.

Asia-Pacific holds the largest share of the global tin catalyst market and is expected to maintain the highest growth rate over the forecast period. Key economies such as China, India, Japan, and South Korea are driving demand due to robust industrialization, expanding automotive production, and a strong presence of polyurethane and silicone manufacturing facilities.

Supportive government policies, foreign direct investments, and a growing focus on construction and infrastructure development further fuel market growth. China, in particular, leads both in production and consumption, benefiting from a well-developed chemical manufacturing ecosystem and export-oriented industrial base.

North America, led by the United States, represents a mature but stable market for tin catalysts. A well-established automotive and construction industry, coupled with significant investments in R&D for advanced materials, sustains demand across end-use applications.

The growing push for sustainability and the shift toward green and bio-based catalysts are influencing product innovation in the region. Additionally, stringent safety and quality standards ensure steady reliance on proven catalyst technologies, including specialized tin compounds.

Despite facing strict environmental regulations surrounding organotin compounds, Europe remains a significant market—especially for eco-friendly and low-toxicity tin catalysts. Countries like Germany, France, and the UK are at the forefront of adopting greener chemical processes, particularly in electronics, building materials, and industrial coatings.

The region’s advanced manufacturing capabilities, high regulatory compliance, and focus on energy efficiency contribute to the steady use of tin catalysts, particularly in applications where performance consistency and environmental safety are both critical.

While still emerging markets, Latin America and the Middle East & Africa (MEA) are witnessing moderate but rising demand for tin catalysts. Brazil, Mexico, the UAE, and Saudi Arabia are key contributors, driven by infrastructure expansion, increasing industrial output, and growing automotive assembly activities.

Modernization of industrial processes, increased foreign investments, and the rising presence of international chemical players are expected to open new opportunities for tin catalyst adoption in these regions—particularly in construction, packaging, and adhesives.

The market size for tin catalysts is USD 375 million.

The projected CAGR of the tin catalysts is 5.9%.

The Polyurethane production application dominates the tin catalysts market.

The Asia-Pacific region dominates the market, driven by rapid industrialization and high polyurethane demand.

1.1 Summary

1.2 Research methodology

2.1 Research Objectives

2.2 Market Definition

2.3 Limitations & Assumptions

2.4 Market Scope & Segmentation

2.5 Currency & Pricing Considered

3.1 Drivers

3.2 Geopolitical Impact

3.3 Human Factors

3.4 Technology Factors

4.1 Porters Five Forces Analysis

4.2 Value Chain Analysis

4.3 Average Pricing Analysis

4.4 M & A, Agreements & Collaboration Analysis

5.1 Tin Catalyst Market, By Grade

5.1.1 Introduction

5.1.2 Market Size & Forecast

5.2 Tin Catalyst Market, By Application

5.3 Tin Catalyst Market, By End-Use Industry

5.4 Tin Catalyst Market, By Distribution Channel

6.1 North America Tin Catalyst Market, By Country

6.1.1 Tin Catalyst Market, By Grade

6.1.2 Tin Catalyst Market, By Application

6.1.3 Tin Catalyst Market, By End-Use Industry

6.1.4 Tin Catalyst Market, By Distribution Channel

6.2 U.S

6.2.1 Tin Catalyst Market, By Grade

6.2.2 Tin Catalyst Market, By Application

6.2.3 Tin Catalyst Market, By End-Use Industry

6.2.4 Tin Catalyst Market, By Distribution Channel

6.3 Canada

7.1 U.K.

7.2 Germany

7.3 France

7.4 Spain

7.5 Italy

7.6 Russia

7.7 Nordic

7.8 Benelux

7.9 The Rest of Europe

8.1 China

8.2 South Korea

8.3 Japan

8.4 India

8.5 Australia

8.6 Taiwan

8.7 South East Asia

8.8 The Rest of Asia-Pacific

9.1 UAE

9.2 Turkey

9.3 Saudi Arabia

9.4 South Africa

9.5 Egypt

9.6 Nigeria

9.7 Rest of MEA

10.1 Brazil

10.2 Mexico

10.3 Argentina

10.4 Chile

10.5 Colombia

10.6 Rest of Latin America

11.1 Global Market Share (%) By Players

11.2 Market Ranking By Revenue for Players

11.3 Competitive Dashboard

11.4 Product Mapping